Arkansas has around 166,000 residents enrolled in ACA exchange plans, 92% of whom are currently subsidized. I estimate they also have perhaps another ~11,000 unsubsidized off-exchange enrollees.

New Mexico has around ~70,000 residents enrolled in ACA exchange plans, 85% of whom are currently subsidized. I estimate they also have another ~8,000 unsubsidized off-exchange enrollees.

Iowa has around 136,000 residents enrolled in ACA exchange plans, 88% of whom are currently subsidized. I estimate they also have another ~9,600 unsubsidized off-exchange enrollees.

The District of Columbia has around ~15,000 residents enrolled in ACA exchange plans. Unlike most states where nearly all ACA exchange enrollees are subsidized, in DC only around 28% are due to the District having an unusually high income eligibility threshold for Medicaid (210%).

DC also has a unique requirement that ACA individual market plans can only be sold on their ACA exchange; I'm assuming perhaps 1,000 off-exchange enrollees regardless but officially I believe this should be pretty much zilch. With net attrition since January, however, it looks like the grand total is actually a bit below 14,000 District-wide.

Rhode Island has around ~42,000 residents enrolled in ACA exchange plans, 88% of whom are currently subsidized. I estimate they also have another ~3,000 unsubsidized off-exchange enrollees.

State Highlights Rising 2026 Health Insurance Rate Proposals

SAINT PAUL, MN: Minnesotans are facing unnecessarily higher health insurance rate hikes, and the blame lies with new Republican-led federal policy changes passed in Washington, says Minnesota Commerce Commissioner Grace Arnold.

“While HR1 has been dubbed the “One Big Beautiful Bill” by Republicans, many in our state will find nothing beautiful in health insurance premium increases they’ll experience for 2026,” Arnold said. “These will be the highest rate hikes since 2017 for individual and group markets.”

Maine has around 64,000 residents enrolled in ACA exchange plans, 85% of whom are currently subsidized. I estimate they also have another ~4,500 unsubsidized off-exchange enrollees.

Combined, that's around 70,000 people, although it could be somewhat lower due to net enrollment attrition since January.

Nevada has around ~110,000 residents enrolled in ACA exchange plans, 87% of whom are currently subsidized. I estimate they also have another ~23,000 unsubsidized off-exchange enrollees.

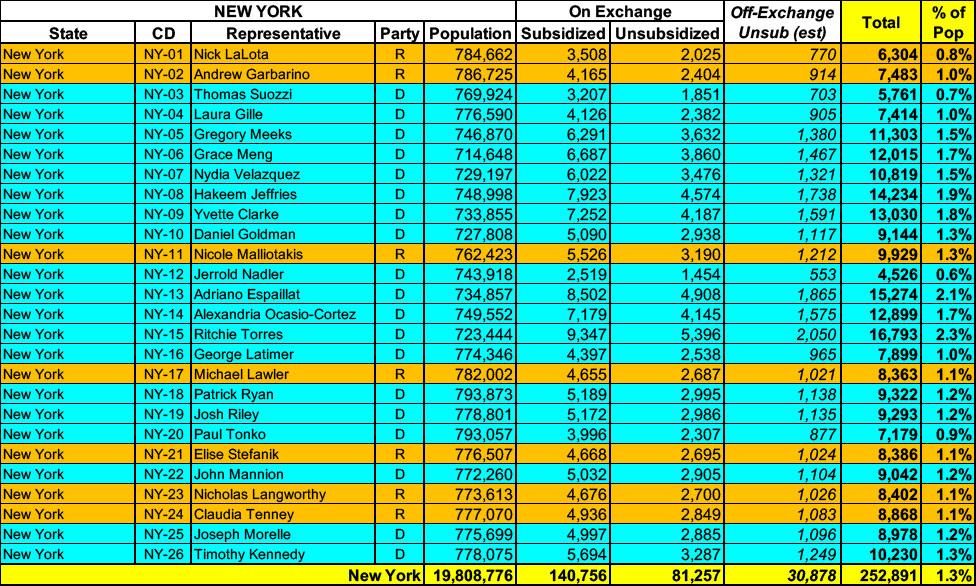

New York has around ~222,000 residents enrolled in ACA exchange plans, 63% of whom are currently subsidized. I estimate they also have another ~31,000 unsubsidized off-exchange enrollees.

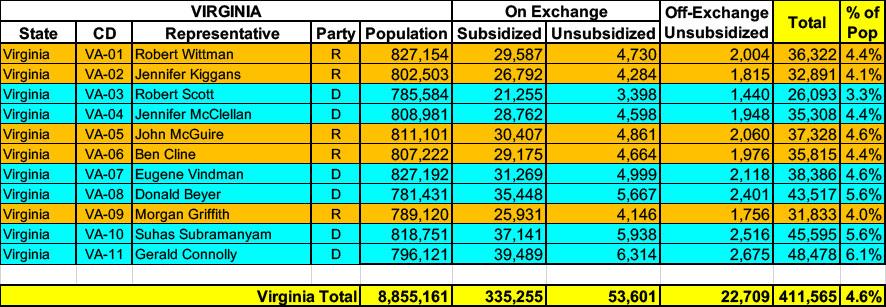

Virginia has ~388,000 residents enrolled in ACA exchange plans, 86% of whom are currently subsidized. They also have over 22,000 off-exchange enrollees. Combined, that's 411,000 people with ACA market coverage, or 4.6% of the total population.