Connecticut has around ~151,000 residents enrolled in ACA exchange plans, 88% of whom are currently subsidized. I estimate they also have another ~7,000 unsubsidized off-exchange enrollees.

NJ Department of Banking and Insurance Warns of Congressional Reconciliation Bill Package’s Impact on Health Insurance Access

TRENTON — New Jersey Department of Banking and Insurance Commissioner Justin Zimmerman has sent a letter to New Jersey’s Congressional delegation warning them of the devastating impacts of the reconciliation package on access to quality, affordable health coverage for millions of Americans who need it, including over 513,000 New Jerseyans. The letter follows the U.S. House passage of the reconciliation package on May 22. A version of the bill is currently pending before the U.S. Senate.

The bill package would repeal key provisions of the Affordable Care Act, making it more difficult and expensive to enroll in coverage through Get Covered New Jersey, the State’s Official Health Insurance Marketplace. This legislation would:

Congress Urged to Renew Expiring Enhanced Premium Tax Credits and Prevent Unnecessary Increases in Health Care Costs for New Jersey Residents

Over 450,000 Get Covered New Jersey enrollees would be impacted by loss of expanded financial help

New Jerseyans could lose more than half a billion dollars in federal support and face higher health insurance costs

TRENTON — Warning about significant health insurance premium increases for over 450,000 New Jerseyans, New Jersey Department of Banking and Insurance Commissioner Justin Zimmerman sent a letter to New Jersey’s Congressional delegation strongly urging them to extend the expiring federal enhanced premium tax credits that have enabled hundreds of thousands of New Jersey residents to enroll in quality, affordable health insurance through Get Covered New Jersey, the State’s Official Health Insurance Marketplace.

9/29/25: Welcome Paul Krugman subscribers! I greatly appreciate the shoutout by him but should add the following clarification:

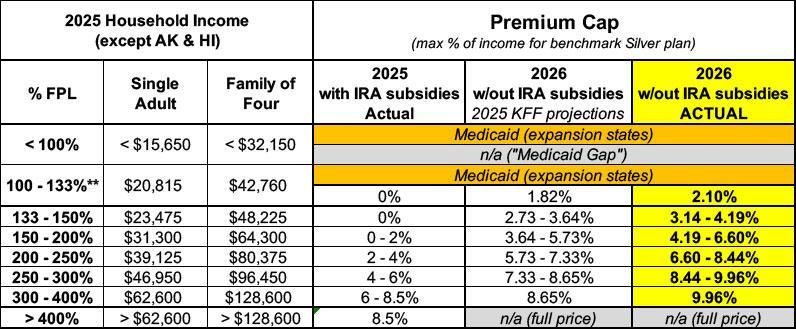

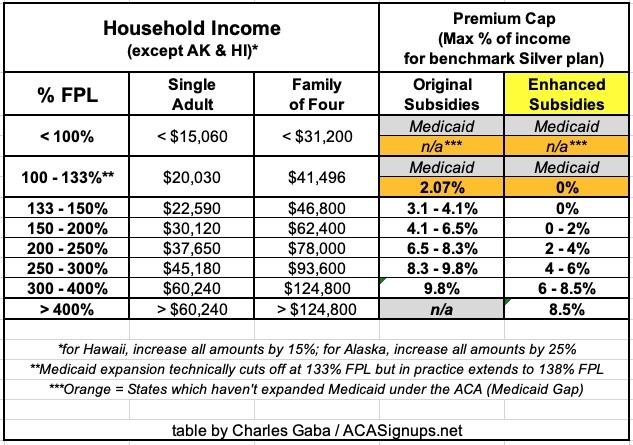

Regarding the chart below which he reposted comparing the original ACA subsidy scale to the current version: You probably think that if the enhanced subsidies expire it will revert back to the original version, which would be bad enough. In fact, however, the Trump Regime has also made THAT version even worse, like so:

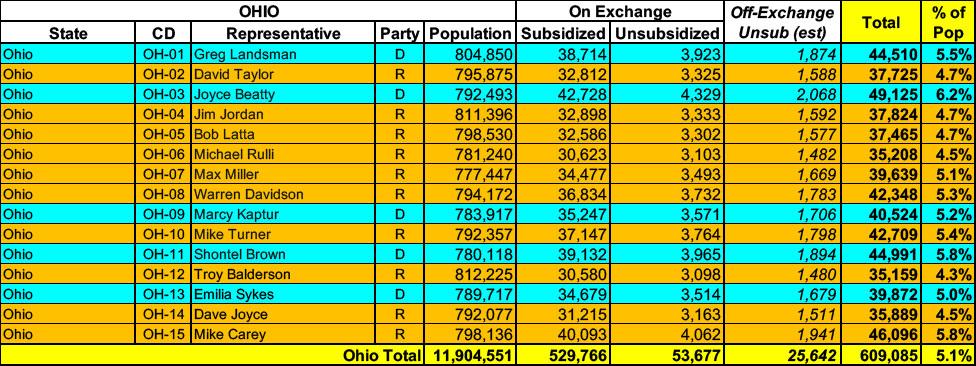

Ohio has around ~583,000 residents enrolled in ACA exchange plans, 91% of whom are currently subsidized. I estimate they also have another ~25,000 unsubsidized off-exchange enrollees.

Re: The Effects of Not Extending the Expanded Premium Tax Credits for the Number of Uninsured People and the Growth in Premiums

Dear Chairman Wyden, Ranking Member Neal, Senator Shaheen, and Congresswoman Underwood:

You have asked the Congressional Budget Office to discuss the effects on health insurance coverage and premiums that will result from not extending—either for one year or permanently—the expanded premium tax credit structure provided in the American Rescue Plan Act of 2021 (ARPA, Public Law 117-2).

ARPA reduced the maximum amount eligible enrollees must contribute toward premiums for health insurance purchased through the marketplaces established by the Affordable Care Act, and it extended eligibility to people whose income is above 400 percent of the federal poverty level (FPL). Those provisions were extended through calendar year 2025 in the 2022 reconciliation act (P.L. 117-169).

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

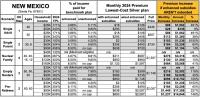

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula: