Covered California’s Iconic Bus Tour Rolls into San Francisco to Promote Health Insurance Enrollment Ahead of Final Deadline

Covered California’s bus tour promotes enrollment and encourages consumers to see if they are eligible for financial help in obtaining quality health insurance.

The San Francisco visit coincides with the release of Governor Gavin Newsom’s budget which focuses on making health care more affordable through increased financial help and a state individual shared responsibility provision.

Consumers have through Jan. 15 to sign up and select a plan, through Covered California or directly with health plans, for Feb. 1 coverage.

An estimated 1.1 million uninsured Californians are eligible to enroll in Covered California and research shows that 82 percent of uninsured consumers surveyed, who are eligible for financial assistance, do not know that they qualify.

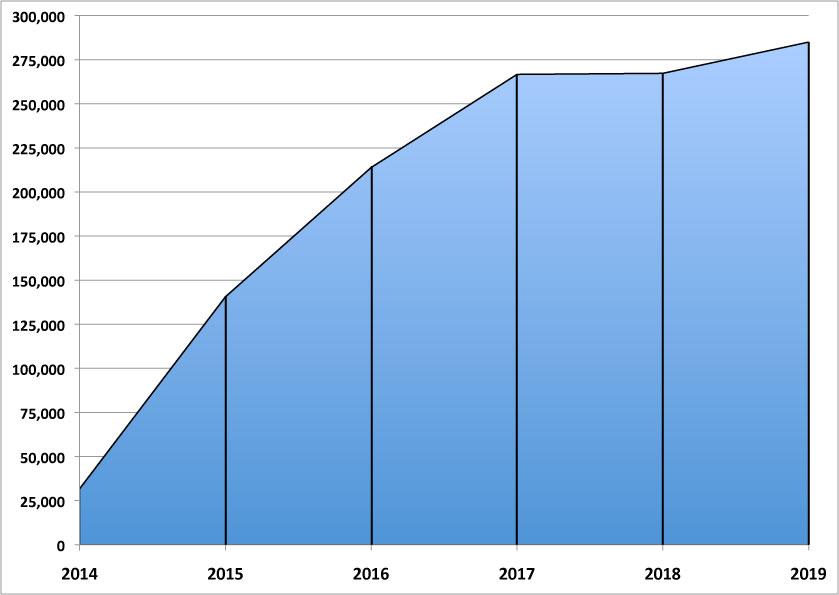

Once again: Massachusetts has managed to outperform their ACA enrollment numbers every year for five years running:

2014: 31,695 (major technical problems)

2015: 140,540 (complete platform overhaul)

2016: 213,883

2017: 266,664

2018: 267,260

2019: 284,969 and counting...

Just as impressive, if not more so: 97.2% of Massachusetts ACA enrollees have already paid their first monthly premium, which is well above the ~90% national average.

BLOCK GRANTS FOR MEDICAID — A Trump plan is in the works. Scoop today, behind the firewall right now. https://t.co/2PdVQKPoLH

The Trump administration is plotting a path for Medicaid block grants for states, a longstanding GOP goal to rein in spending on the entitlement program. News from me and @ddiamondhttps://t.co/EPkeqlPiSV

Per admin sources, CMS has guidance to states in the works on the topic. Officials also very aware of the political sensitivities surrounding such a plan.

Yesterday I wrote about the current status of several federal lawsuits against the Trump Administration over the decision to stiff contractors (i.e., health insurance carriers) out of nearly $2 billion in Cost Sharing Reduction reimbursement payments.

This morning I wrote about the current status of the infamous #TexasFoldEm lawsuit brought by 20 Republican Attorneys General and Governors against the ACA, and the impending appeal of Judge O'Connor's ruling in their favor.

I haven't written anything about the developments in the #TexasFoldEm anti-ACA lawsuit in awhile, partly because I was out of the country for a couple of weeks and got backlogged. Then again, things are kind of at a standstill at the moment anyway, so perhaps that omission on my part isn't quite as big of a deal as I had feared.

Last chance: MNsure Open Enrollment Period Ends this Sunday, January 13

January 10, 2019

ST. PAUL, Minn.—Minnesotans have until midnight on Sunday, January 13, to secure health insurance coverage through MNsure for 2019. Those who enroll by the deadline will have coverage that begins February 1.

"MNsure is the only place to get financial help to save money on your monthly premium," said MNsure CEO Nate Clark. "More than half of all MNsure enrollees are receiving tax credits."

Minnesotans can see if they qualify for financial help, while also comparing medical plans side by side, by using MNsure's plan comparison tool.

MNsure has extended Contact Center hours in the days leading up to the final deadline:

Reinstating the individual mandate penalty at the state level, as New Jersey, the District of Columbia, Vermont and Massachusetts have (VT's doesn't kick in until next year, and MA simply reverted back to their own pre-ACA mandate penalty), and

Enhancing ACA subsidies and expanding them to those earning 400-600% of the Federal Poverty Level

Newsom didn't include any details on either proposal, but I assumed that the mandate would simply reinstate what it was under the ACA before being repealed by Congressional Republicans in December 2017 ($695 per person or 2.5% of household income), and that the expanded subsidies would simply take the existing ACA formula (which limits the cost of benchmark Silver plans to no more than 9.86% of household income and provides subsidies to cover the difference after that), and raise the cut-off point from 400% FPL to 600% FPL.

That should mean that the average HC.gov premium is around $600 or so per month in 2018. The 3.5% surcharge hasn't changed for 2018, which means the federal exchange should take in something like $252/year per enrollee. Total enrollment in HC.gov plans was down 5% this year, so I'll assume average effectuated enrollment will be as well...somewhere around7.13 million per month. That means ~$1.8 billion in HC.gov revenue directly from the premium surcharge.

In the midst of the ongoing #TrumpShutdown, where hundreds of thousands of federal employees are either off the job altogether or having to work without being paid and hundreds of federal contractors are being stiffed for the work they've done in good faith, I just wanted to remind folks that Donald Trump also screwed over several hundred insurance carriers in October 2017 when he cut off contractually-owed Cost Sharing Reduction reimbursement payments to insurance carriers nationwide.

Monday: Newly sworn-in California Governor Gavin Newsom announces he's pushing for further Medicaid expansion to undocumented young adults; reinstating the mandate penalty; raising the subsidy cap; going All-Payer on prescription medications; and creating a state-level Surgeon General position

Gov. Jay Inslee and Democratic lawmakers Tuesday announced proposed legislation for a new “public option” health-care plan under Washington’s health-insurance exchange.

The proposal, which Inslee said is the first step toward universal health care, is geared in part to help stabilize the exchange, which has wrestled with double-digit premium increases and attempts by Republicans in Congress and President Donald Trump to dismantle the Affordable Care Act.

“We are proposing to the state Legislature that we have a public option that is available throughout the state of Washington so that we can increase the ability to move forward on the road to universal health care in the state of Washington,” said the governor, who is considering a run for president in 2020.