Connect for Health Colorado Extends Enrollment Deadline for January Coverage to Dec. 18, 2019

DENVER – To help as many people as possible get Jan. 1, 2020 coverage, Connect for Health Colorado is pleased to announce that the deadline to get coverage on Jan. 1 has been extended. Coloradans have until 11:59 p.m. on Wednesday Dec. 18, 2019 to sign up for a health insurance plan that starts on Jan. 1, 2020.

To sign up for coverage that begins Jan. 1, 2020, Coloradans must take the following steps:

1. Complete an application and select a health insurance plan online at ConnectforHealthCO.com, over the phone at 855-752-6749, or by working with a certified enrollment expert by 11:59 p.m. on Wednesday, Dec. 18.

OK, this isn't much of an extension, since the DCHealthLink.com exchange already lets people enroll as late as January 31st...but it's still important:

DC Health Link didn’t have any website issues on Sunday 12/15, but we know that news for other states may have caused confusion.

You now have until December 18 to sign up for a plan that starts January 1.

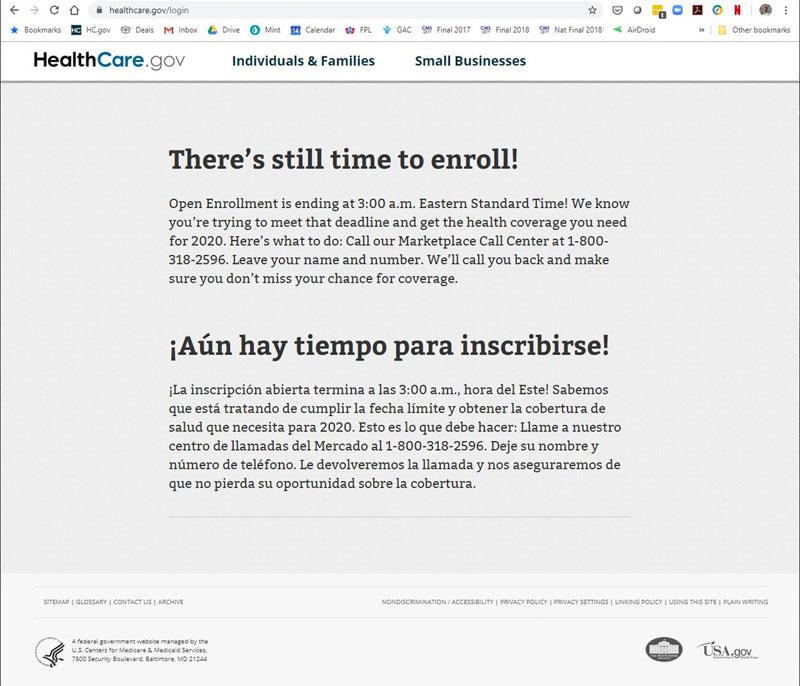

In response to tremendous pressure after yesterday's major technical issues at HealthCare.Gov, CMS Administrator Seema Verma just announced that the deadline for people to #GetCovered in the 38 states which host their ACA enrollment platform with HealthCare.Gov will indeed be extended by 2 days:

We at @CMSGov want to ensure a seamless shopping experience for everyone seeking coverage, so starting at 3 pm ET today, we are extending the marketplace #OpenEnrollment deadline until 3 am ET December 18! https://t.co/HmVdpJlX2C

OK, this is about as obscure of an "announcement" as I can imagine: Per a heads up from Louise Norris, if you visit the Washington HealthPlan Finder website this morning, there's a simple message at the top reading:

There's still time to get covered. Sign up by Dec. 30 to get coverage that starts Feb 1st.

That's it. There's no link to a press release, there's nothing in their "news announcements" archive, and as of this writing there's no tweet from their Twitter account announcing it...just that simple text message.

I'll update if/when there's a formal announcement, but until then...it appears that Washington State residents do indeed have another 16 days to #GetCovered after all, even if they'll face a one-month gap in coverage.

UPDATE: Confirmed:

Still need to sign up in a health plan? You're in luck!

Enroll in a plan from now through Dec. 30 at 8pm to receive coverage starting Feb. 1, 2020. #GetCoveredWA

As of today, their press release page states the following:

Stats as of December 13, 2019:

Qualified Health Plans (QHP):

Net Total QHP Enrollment: 102,589

2020 OE Acquisition Summary: 15,067

Overall Volume

Unique Website Visitors: 157,591

Calls Handled: 152,733

Medicaid: Completed applications/redeterminations processed through the integrated eligibility system: 35,231

This was as of 12/13, so it's missing the last 2 days of Open Enrollment signups. They would have to have added another 8,500 people in the final two days in order to beat last year's total of 111,066.

If you still missed the deadline, you won't be eligible to enroll for ACA-compliant major medical coverage for the rest of the year unless you qualify for a Special Enrollment Period (SEP) due to a qualify life event lke getting married/divorced, moving, giving birth/adopting a child, turning 26, becoming ineligible for Medicaid or losing your employer-sponsored health insurance coverage.

Dammit, I took a couple of hours off to rewatch The Force Awakens with my kid (in anticipation of The Rise of Skywalker coming out this week), and look what happens...

HealthCare.Gov is not letting people login to enroll. This is the second outage, the first lasted 15 minutes. We're 8 minutes into the second. Last time this happened, 100k people could not enroll. @CMSGov must extend the deadline.

Due to high call volume and enrollment demand, @CoveredCA will extend the deadline for Jan. 1 coverage through midnight next Friday, Dec. 20. That means consumers have an extra 5 days to sign up for #ACA#healthcare coverage for all of 2020. Check rates.

Moments ago, Covered California, the nation's largest state-based ACA exchange, released data via a media teleconference regarding the 2020 Open Enrollment Period.

In addition to being the largest ACA exchange after HealthCare.Gov, this info from Covered California is especially significant for the 2020 OEP due to their newly expanded/enhanced premium subsidies.

To recap: Under the ACA, financial subsidies are available to exchange enrollees earning between 100-400% of the Federal Poverty Level (FPL). That's between around $12,500 - $50,000/yr if you're a single adult, or between $25,000 - $100,000/yr for a family of four. Under the standard ACA formula, enrollees in that income range have their premiums capped at no more than around 2.0 - 9.8% of their income, on a sliding scale.

Unfortunately, this means that people earning more than 400% FPL are eligible for no financial assistance at all, a sudden drop-off known as the Subsidy Cliff.

More Than 200,000 New Yorkers Enroll in a Qualified Health Plan During First Forty-One Days of the 2020 Open Enrollment Period

December 15 is the Deadline to Enroll for January 1 Coverage

(ALBANY, N.Y.) December 12, 2019 - NY State of Health, the state’s official health plan Marketplace today announced that as of December 11, more than 200,000 consumers have enrolled in a 2020 Qualified Health Plan (QHP) through NY State of Health, the official health plan Marketplace, outpacing enrollment in a QHP at the same period last year by approximately 7,000 enrollees. Consumers must enroll or renew by December 15 for coverage beginning January 1, 2020.