Back in June 2016, the Obama Administration rightly clamped down on "Short-Term Plans", limiting them to, you know, a "short term"...no more than 3 months out of the year, while also making them non-renewable; that is, you couldn't get around the 3-month limit by simply renewing the policy every three months:

An analysis of potential premium changes in states across the nation shows increases of 16 to 30 percent likely in 2019 if federal steps are not taken.

While the Patient Protection and Affordable Care Act’s subsidies would largely insulate subsidized consumers from these costs, millions of unsubsidized consumers would pay the full price of these increases. Many would likely be priced out of coverage.

Continued policy and premium uncertainty risks further carrier withdrawals, leaving more consumers with only one health plan and even the prospect of “bare counties.”

The analysis reviews three federal policy options that could stabilize markets and mitigate the impact of premium increases in many states.

Covered California’s open-enrollment period is still underway and consumers have through Jan. 31 to sign up for coverage.

A week or so ago, there was some confusing news about how Donald Trump may or may not be planning on signing a new healthcare-related executive order. I didn't write about it earlier because at first it sounded like he was talking about a meaningless "sell across state lines" decree...meaningless because the ACA already allows carriers to sell ACA-compliant policies across state lines, as long as the states in question sign onto an interstate compact.

It's not over yet, since the House of Representatives still has to vote on the bill again (either as is, or after hashing out the differences between the House and Senate versions of the bill), but assuming the final version of the bill includes mandate repeal and is indeed signed into law, this is what the ACA's 3-legged stool would look like when the dust settles.

Obviously I'll have much more to say about what happened last night soon, but for the moment I'll leave it at this.

Things were looking pretty dicey for two of Montana's three insurance carriers participating on the individual market the past few days. One of the three, Blue Cross Blue Shield, saw the writing on the wall regarding Cost Sharing Reductions (CSR) likely being cut off and filed a hefty 23% rate hike request with the state insurance department. The other two, however (PacificSource and the Montana Health Co-Op, one of a handful of ACA-created cooperatives stll around), assumed that the CSR payments would still be around next year and only filed single-digit rate increases.

I'm not going to speculate as to the reasons why they both did so when it was patently obvious that having the CSRs cut off was a distinct possibility, although I seem to recall the CEO of the Montana Co-Op said something about their hands being tied since CSR reimbursement payments are legally required, after all. Basically, it sounds like he was genuinely trying to avoid passing on any more additional costs to their enrollees than they had to.

Hey there, I called again and I was able to talk to a more knowledgeable agent who found out what the issue was and was able to enroll me in a plan!

Apparently, the Marketplace renewed automatically my application based on my 2016 income, which was enough to receive a tax credit in 2017, but is no longer enough to receive one in 2018.

Luckily, my income has increased since then, so I reported the change and was able to get a credit applied to the premiums

Still need to send copy of my green card for verification, but I can use the tax credit immediately

So I'm not sure why the person I talked to earlier today told me the rules had changed

Sorry for the confusion

OOF. OK, this pretty much torpedoes the entire basis of this blog entry. I'm going to leave it up in the interest of letting documented immigrants know that they ARE eligible to enroll AND for tax credits, but it sounds like the original concern may be unwarranted after all.

With the 2018 Open Enrollment Period coming up just 5 days from now, it's time to put this to bed: After 6 months of painstaking research and analysis, I've compiled a comprehensive analysis of the weighted average rate changes for unsubsidized ACA-compliant individual market policies in 2018, including both the on- and off-exchange markets. It's already been confirmed by a different analysis by healthcare consulting firm Avalere Health, which used a completely different methodology to arrive at the exact same conclusion: The national average increase isbetween 29-30%, ranging from as low as a 22% average premium drop in Alaska(thanks to their successful reinsurance program) to as high as a painful 58% increase in Virginia.

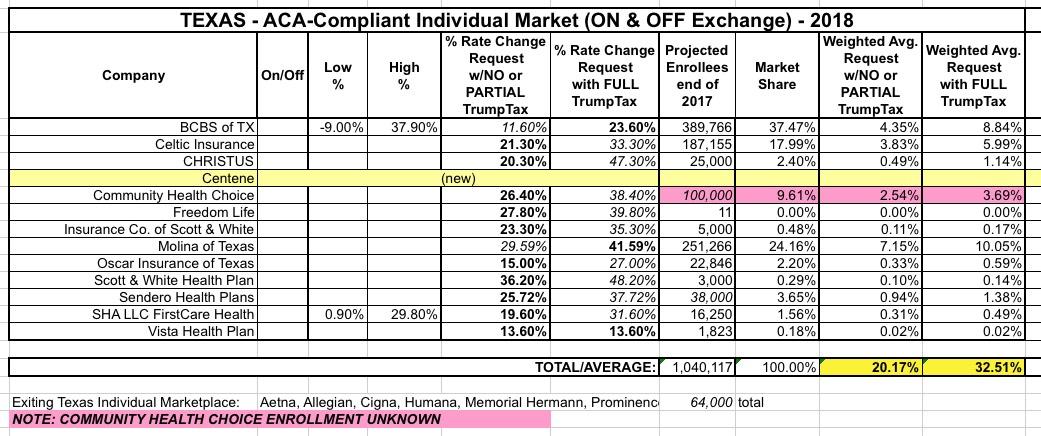

I've saved Texas for last because, frankly, I haven't been able to make heads or tails out of their actual average rate increases for next year (and unlike smaller states which might not move the needle on the national average anyway, Texas has one of the largest populations in the country, so a substantial error here can also impact the national numbers significantly).

Back in early August, I pieced together a rough average of the requested rate increases for the Lone Star State of around 20% if CSR payments are made or 32.5% if they aren't:

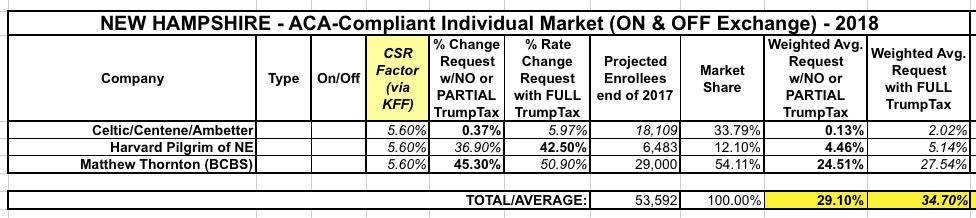

As noted earlier today, I've now managed to plug 48 states (plus DC) into my 2018 Rate Hike Project spreadsheet. This leaves just two states missing: New Hampshire and Texas. I'm still waiting to clarify some things for each, so this analysis could still change, but I really want to wrap this up, so here's what I have for New Hampshire right now:

When I first ran the numbers for New Hampshire'srequested 2018 rate increases, it seemed pretty straightforward: 3 carriers on the individual market. 2 listed rate changes assuming CSRs would be paid; one assumed they wouldn't. This gave the following: