Fifteen health insurers want an average 17.7 percent increase in premiums for Affordable Care Act individual plans, Florida officials said Thursday — higher than last year’s approved average of less than 10 percent.

...In Florida, 15 companies also asked for an average 9.6 percent increase for small group plans, said Amy Bogner, spokeswoman for the state’s Office of Insurance Regulation.

The companies were not identified individually because they claimed trade secrecy, she said.

This may seem like common knowledge now, but in 2014, it felt like I was one of the only people who recognized that there were millions of people enrolling in ACA-compliant policies off of the ACA exchanges, directly via the insurance carriers themselves. My best estimate for 2014 was that in addition to the 7 million or so exchange-based individual market enrollees, there were another roughly 8 million people who enrolled off-exchange (although several million of those were in non-ACA compliant policies).

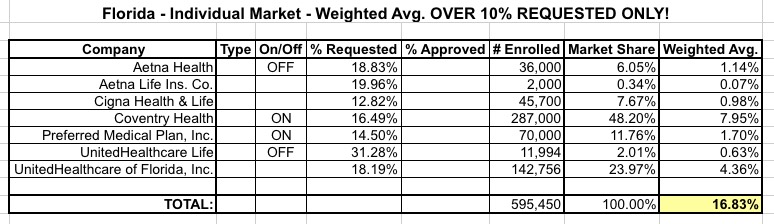

Last week I took the known 2016 Florida rate increase requests (around 14.7% weighted average for 10 companies with around 713,000 enrollees) and took my best shot at trying to estimate what the rest of Florida's ACA-compliant individual market might look like.

In order to do this properly, I'd need 2 pieces of data: First, the weighted average increase request for the 6 additionalcompanies which I didn't already have rate requests for; and second, the total ACA-compliant enrollment number for those 6 companies.

The Rate Review database at Healthcare.Gov is a very useful tool for any insurance company requesting rate increases above 10%, but it's completely useless for requests below 10%. As such, I have hard data on the requested increases for about 600,000 Florida residents:

If Florida's entire ACA-compliant individual market was only 600K people, that would be the end of the story.

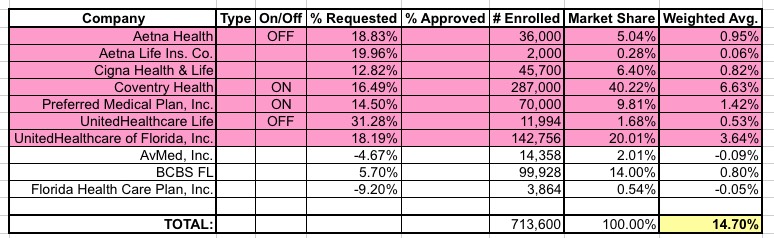

However, Florida actually has 16 different insurance companies selling individual policies...and the other 9 are all asking for lower than 10% hikes. After poking around the Florida Office of Insurance Regulation website as well as contacting the department directly, I've been able to pull together covered lives data for all 16, and requested rate change data for 3 more of them...2 of which are actually requesting rate decreases. When I add those 3 companies into the mix, the picture changes like so:

Of the 6.5 million people who would lose their federal tax credits, and almost certainly their healthcare coverage (completely apart from the additional 6.5 million who would have an economic boulder dropped on them indirectly) in the event of a King v. Burwell plaintiff win, over 1/3 live in just two states: Florida and Texas. 1.34 million Floridians and 846,000 Texans would be be among the direct casualties...close to 2.2 million between the two of them.

Given that both are completely run by off-the-rails batcrap-insane Republicans in the House, Senate and Governor's office, it's safe to say that you can expect a LOT of stories like the following from the Sunshine and Lone Star states.

Gov. Scott: We Will Begin Working Immediately on a Budget to Continue Critical Programs & Start Conversation on Healthcare Access and Cost

On April 30, 2015, in News Releases, by Currie Dickerson

TALLAHASSEE, Fla. – Governor Rick Scott released the following statement today upon the adjournment of the Florida Senate upon the call of the President, and after the Tuesday adjournment of the Florida House:

“Now that the Florida Senate and House have adjourned, we must immediately turn our focus to how we can work together to craft a state budget before July 1st that continues funding for critical state services. There were no discussions about Medicaid expansion under Obamacare before the legislative session began. Today, it is clear that a thorough analysis of how healthcare can be reformed to improve cost, quality and access is needed, apart from the budget process.

Florida Gov. Rick Scott announced Thursday that his administration will file a lawsuit against the federal government for threatening to withhold more than $1 billion in funding for hospitals if the state fails to expand Medicaid.

“It is appalling that President Obama would cut off federal health care dollars to Florida in an effort to force our state further into Obamacare,” Scott said, citing a 2012 Supreme Court ruling that said the federal government couldn’t put a “gun to the head” of states to force them to expand Medicaid under the health care law.

The Obama administration quickly accused Scott of misconstruing that court decision because the state is not being forced to do anything. And White House spokesman Josh Earnest blasted the governor for putting politics above people.

I have a ton of ACA-related stories cluttering up my in-box again; here's some of the more interesting ones, all regarding ACA Medicaid Expansion:

MICHIGAN:

For months now, I've been a bit obsessed with figuring out how my home state's Medicaid expansion enrollment has managed to reach as high as 21% more people than were supposedly even eligible for the program. Estimates last year ranged from 477,000 - 500,000, yet enrollment in Healthy Michigan (Gov. Snyder's name for Obamacare Medicaid Expansion) currently sits at a whopping 579K, less than 1 year into the program.

Remember "Florida Health Choices", the brainchild of Republican Senator Marco Rubio which was supposed to be the Florida GOP's response to the Affordable Care Act health insurance exchanges?

The Florida Republican Party flushed $900,000 in startup funds into a website/"exchange" which signed up a whopping 30 paying customers in 6 months, at a cost of $30,000 apiece...or between 46x - 81x as much per enrollee as the "wasteful" HealthCare.Gov.