Americans for a Balanced Budget released the findings of a national survey of 800 likely voters on November 18, 2025, conducted by pollster John McLaughlin of McLaughlin & Associates, across 16 GOP-held battleground districts rated Toss Up or Lean Republican by the Cook Political Report.

Wyoming has ~46,000 residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. They also have an unknown number of off-exchange enrollees (likely only a few thousand at most). Combined, that's around 8% of their total population.

(Note, however, that the official actuarial rate filings for the 3 carriers offering coverage in the Wyoming individual market only report a combined total of around 39,000 enrollees as of spring 2025, or 6.6% of the total population).

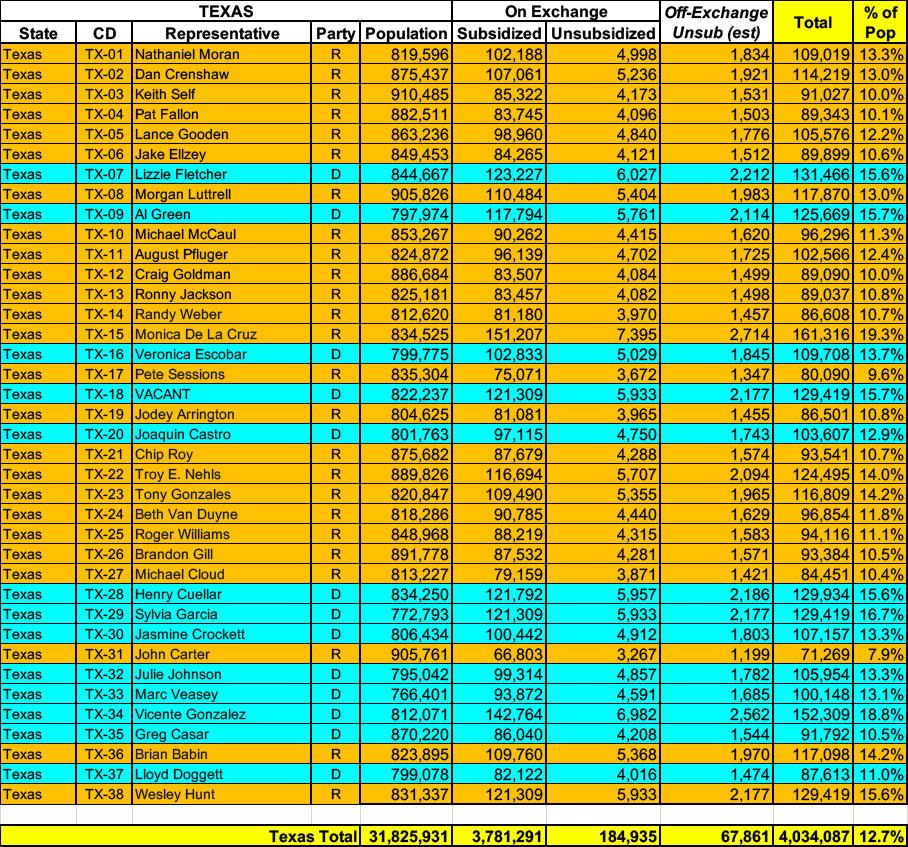

Texas has ~3.9 MILLION residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. I estimate they also have perhaps ~67,000 unsubsidized off-exchange enrollees.

Combined, that's over 4.0 MILLION Texans, although although assuming the national average 6.6% net enrollment attrition rate applies, current enrollment would be back down to more like ~3.8 million statewide.

Mississippi has around ~338,000 residents enrolled in ACA exchange plans, 98% of whom are currently subsidized. I estimate they also have another ~14,000 unsubsidized off-exchange enrollees.

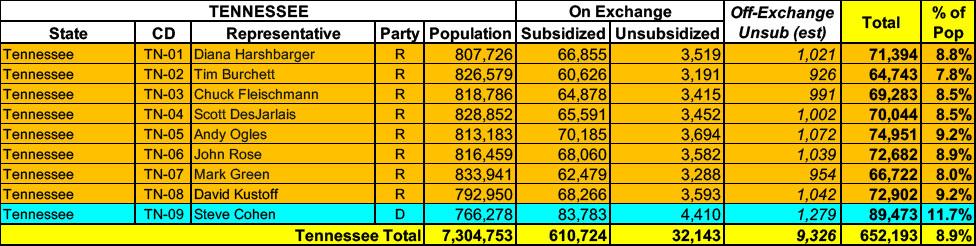

Tennessee has around ~642,000 residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. I estimate they also have another ~9,000 unsubsidized off-exchange enrollees.

Nebraska has around ~136,000 residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. I estimate they also have another ~2,000 unsubsidized off-exchange enrollees.

Alaska has around ~28,000 residents enrolled in ACA exchange plans, 88% of whom are currently subsidized. They also have an unknown number of off-exchange enrollees in ACA-compliant individual market policies. Overall, including net attrition, I estimate their total enrollment both on & off exchange to be perhaps ~27,000 or so.

Kansas has around 200,000 residents enrolled in ACA exchange plans, 94% of whom are currently subsidized. I estimate they also have another ~6,000 unsubsidized off-exchange enrollees.

New Hampshire has around ~70,000 residents enrolled in ACA exchange plans, 71% of whom are currently subsidized. I estimate they also have another ~14,000 unsubsidized off-exchange enrollees.

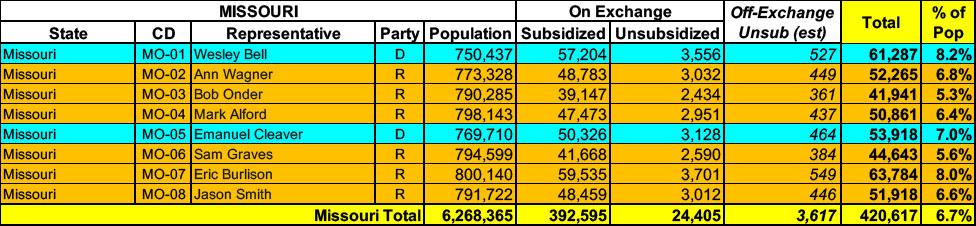

Missouri has around ~417,000 residents enrolled in ACA exchange plans, 94% of whom are currently subsidized. I estimate they also have another ~3,600 unsubsidized off-exchange enrollees.