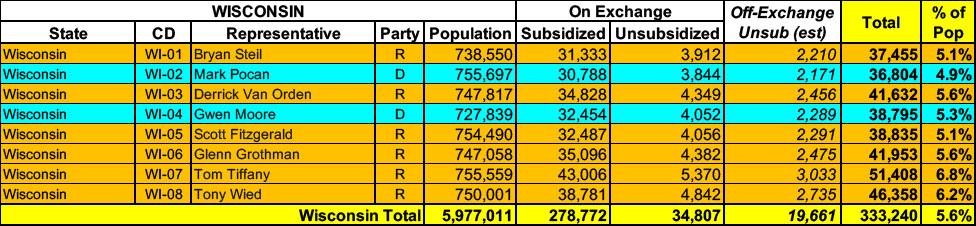

Wisconsin has around ~293,000 residents enrolled in ACA exchange plans, 98% of whom are currently subsidized. I estimate they also have another ~19,000 unsubsidized off-exchange enrollees.

West Virginia has ~67,000 residents enrolled in ACA exchange plans, 97% of whom are currently subsidized. They also have an unknown number of off-exchange enrollees (likely only a few thousand at most).

Colorado has around ~282,000 residents enrolled in ACA exchange plans, 80% of whom are currently subsidized. I estimate they also have another ~39,000 unsubsidized off-exchange enrollees.

Merged Market Summary for Proposed Rates Effective for 2026

The following tables depict the proposed overall weighted average premium increase and the key assumptions behind premium development for the merged (individual and small employer) market filed by insurance carriers as part of the Massachusetts Division of Insurance rate review process (for rates effective in 2026). This information is subject to change as the rate review process continues.

The Health Care Access Bureau within the Massachusetts Division of Insurance is currently reviewing these assumptions. This review process will culminate in a final decision in August 2025.

There are 711,563 consumers enrolled in merged (individual/small group) market plans (data as of December 2024).

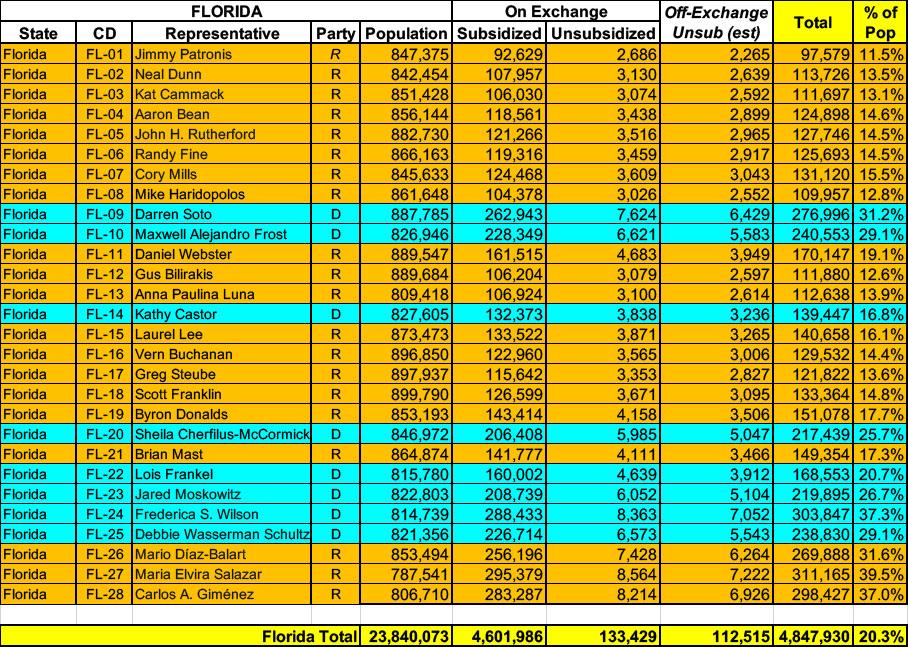

Florida has over ~4.7 MILLION residents enrolled in ACA exchange plans, 97% of whom are currently subsidized. I also estimate they have perhaps ~112,000 unsubsidized off-exchange enrollees.

Combined, that's over 4.8 million people, or a stunning 20.3% of their total population. 1 in 5 Floridians are enrolled in ACA exchange healthcare coverage (assuming CMS's 6.6% net national attrition rate applies to Florida specifically, the actual number of current enrollees is more like 4.5 million, or 19% of the state population).

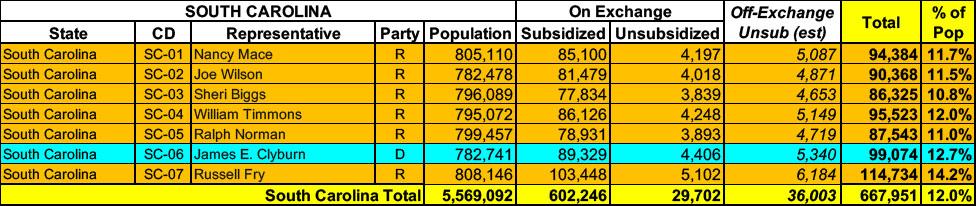

South Carolina has around ~632,000 residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. I estimate they also have another ~36,000 unsubsidized off-exchange enrollees.

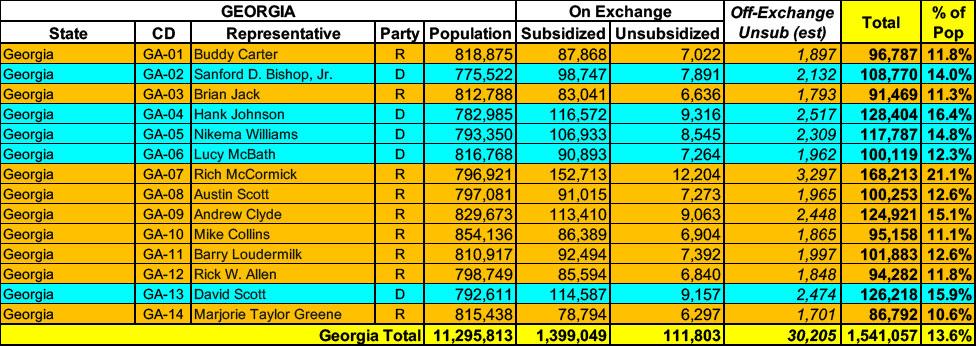

Georgia has around ~1.5 MILLION residents enrolled in ACA exchange plans, 93% of whom are currently subsidized. I estimate they also have another ~30,000 unsubsidized off-exchange enrollees.

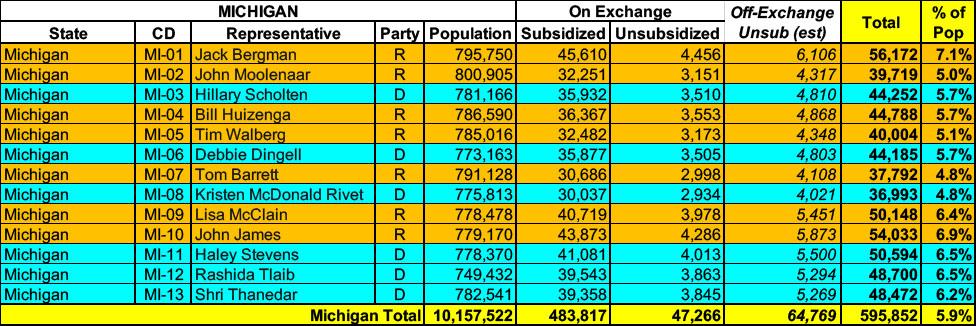

Michigan has around 531,000 residents enrolled in ACA exchange plans, 91% of whom are currently subsidized. I estimate they also have another ~64,000 unsubsidized off-exchange enrollees.

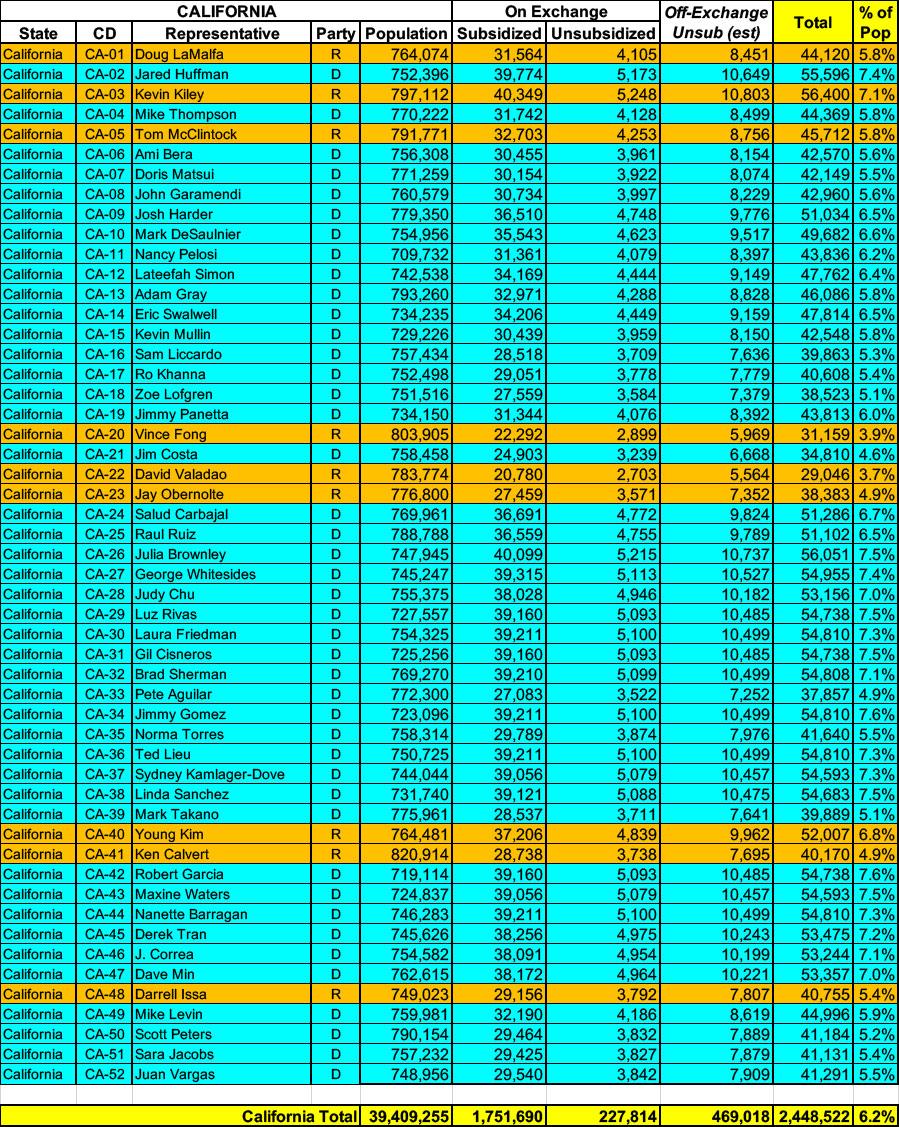

California has ~1.98 MILLION residents enrolled in ACA exchange plans, over 88% of whom are currently subsidized. They also have an estimated ~470,000 off-exchange enrollees. Combined, that's over 2.4 million people, or 6.2% of their total population.

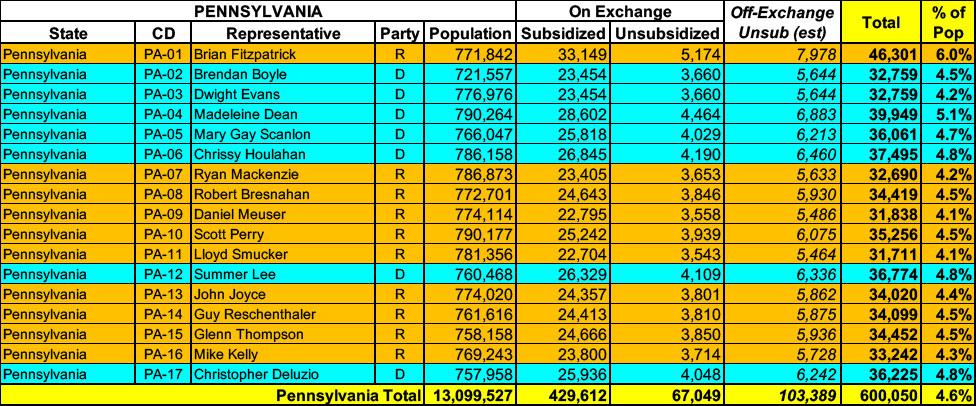

Pennsylvania has around ~496,000 residents enrolled in ACA exchange plans, 87% of whom are currently subsidized. I estimate they also have another ~103,000 unsubsidized off-exchange enrollees.

{kind=link}