For months now I've been warning that the initial data published about the 2026 ACA enrollment would likely massively underestimate just how ugly things were in terms of both effectuated enrollment as well as how comprehensive the coverage would be for those who did enroll.

Back in December, when Open Enrollment was still going on, I noted that regardless of what the official number of Americans who selected an exchange plan during Open Enrollment was, the actual number of those who would have effectuated coverage over the course of the year would likely be far lower:

So, what will this graph look like for 2026?

...IF that's what ends up happening, it would look something like the following:

Sen. Bernie Moreno, R-Ohio, made his final pitch to Senate Democrats on a plan to revive expired health care subsidies on Wednesday, according to a copy of the legislation obtained by Semafor.

The Ohio Republican is pitching a one-year extension of the enhanced premium tax credits that expired at the end of last year with an option to use Health Savings Accounts after 2026. it would also bar “individuals not lawfully present” in the US from receiving benefits under the bill.

...The proposal also includes a minimum $5 monthly payment on subsidized plans; extends open enrollment until March 31; imposes penalties on fraud; requires audits of states’ compliance with the Hyde amendment barring taxpayer funding on abortions; includes cost-sharing reduction payments; and caps the subsidies at 700% of the federal poverty level.

[GOP Sen. Bernie Moreno of Ohio] said his goal is to get roughly 35 of the Senate’s 53 GOP senators to support an eventual deal — not just a handful joining Democrats on a “defection vote” — and that he’s keeping the White House and Senate leaders closely apprised of the discussions.

...His involvement is also a sign that a new generation of bipartisan dealmakers might be starting to emerge after some of the Senate’s old hands headed for the exits in recent cycles. Moreno is now in close touch with not only Collins and Shaheen but other Senate pragmatists such as Tim Kaine (D-Va.), Lisa Murkowski (R-Alaska) and Angus King (I-Maine).

...The Senate group’s proposed extension would include new restrictions including a $5 a month minimum premium payment and an income cap set at 700 percent of the federal poverty level. In the second year, the proposal would also give enrollees to take their subsidy as cash in pre-funded health savings accounts — an arrangement favored by Trump.

As expected, just moments ago the House of Representatives voted to extend the enhanced ACA tax credits for another 3 years, through the end of 2028, with no strings attached...with a whopping 17 House Republicans crossing over to vote for it.

This is actually slightly higher than my prediction yesterday that up to 16 total House Republicans would vote for it, I should note!

I'm going to assume it will end up narrowly passing the House; it would be pretty stupid for those four to sign the discharge petition without actually voting for the bill, and Republicans are currently down 2 members anyway with Marjorie Taylor Greene (GA) having resigned and Doug LaMalfa (CA) dying yesterday morning.

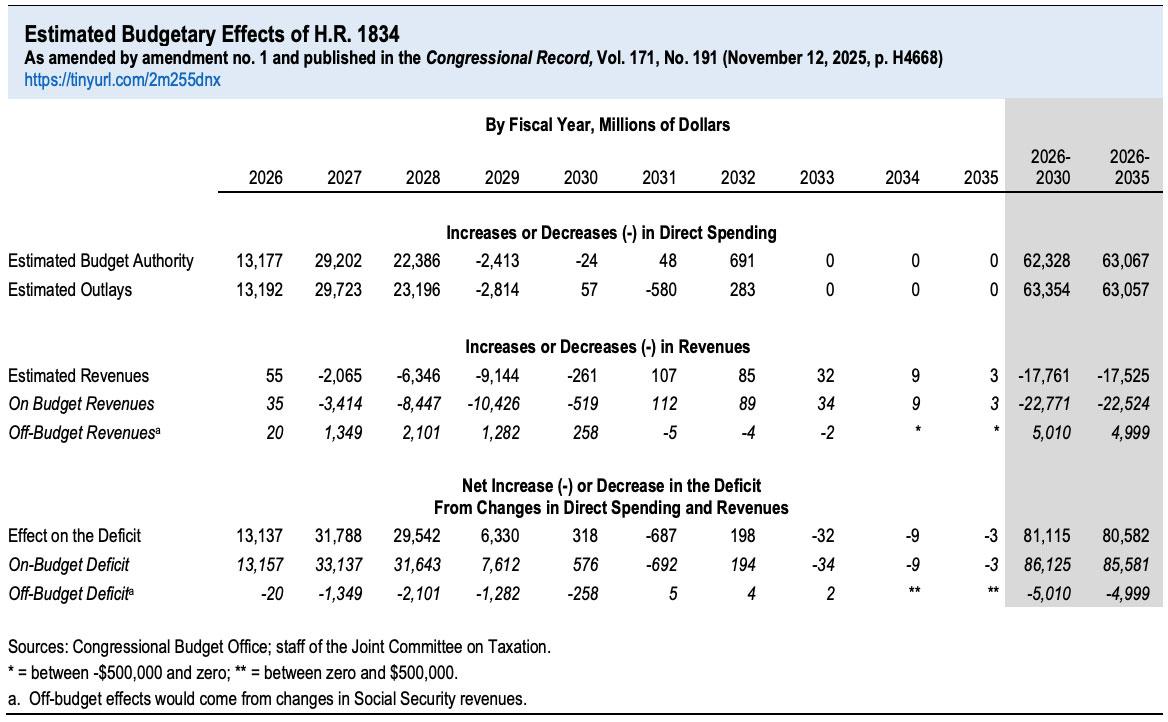

H.R. 1834 would authorize an extension through 2028 of the premium tax credit structure provided in the American Rescue Plan Act of 2021 and later extended through calendar year 2025 by the 2022 reconciliation act. The advanceable and refundable premium tax credit reduces out−of-pocket costs for the premiums enrollees pay for health insurance obtained through the marketplaces established by the Affordable Care Act.

Budget-wise, the CBO is pegging a 3-yr extension at costing around $80.6 billion net (they had previously pegged a 10-yr extension at ~$350B, but that assumes 10 years of inflation/etc as well).

Yesterday morning on CNN's "State of the Union," host Kasie Hunt talked to Oklahoma GOP Sen. James Lankford about the enhanced ACA tax credits which are currently scheduled to expire exactly 10 days from now.

This gets into the weeds a bit, so I'm breaking it into two separate posts; I'll be publishing the second part tomorrow.

The crux of the CNN appearance was Langford claiming that "Obamacare" (the Affordable Care Act...guys, he's been out of office for nearly 9 years now, let it go willya?) "caused prices to skyrocket in the marketplace" and that the expiration of the enhanced tax credits put into place in 2021 during the COVID pandemic is simply "exposing the real issues" within the ACA.

First of all, let's clear up this "they were only put in place due to the COVID pandemic" talking point which Republicans keep tossing around (the implication being that since the COVID pandemic is over, the subsidy upgrade should end as well).

Get it straight: Eliminating the 400% FPL subsidy cliff and beefing up the tax credit formula is something which Democrats always intended to do when they had the ability to do so.

Welp. In a development which should surprise absolutely no one, GOP House Speaker Mike Johnson has announced that the bipartisan "Fitzpatrick Bill" which would include a 2-year extension of the enhanced ACA tax credits (albeit with significant caveats) won't be included in their healthcare bill vote this week after all.

Speaker Mike Johnson confirmed Tuesday he will not allow a House vote this week to extend expiring Obamacare subsidies — a reversal from last week when a GOP leadership aide said the process “would allow” for an amendment vote.

“In the end, there was not an agreement,” Johnson told reporters, noting the divides in his conference over the subsidies.