Implications Of CMS Mandating A Broad Load Of CSR Costs

In October 2017, the Trump administration eliminated federal funding to reimburse insurers for cost-sharing reduction (CSR) subsidies, which they are obligated to provide to qualifying enrollees in the Affordable Care Act (ACA) Marketplace. President Donald Trump had threatened to eliminate CSR funding throughout 2017, so insurers and insurance regulators in many states had anticipated the move by adding the cost of CSRs to premiums for 2018.

Insurers selling Obamacare plans in Maryland are again seeking huge rate increases for 2019, but they could be knocked down significantly by a reinsurance program the state hopes to implement for next year.

CareFirst BlueCross BlueShield wants to increase rates on average by 18.5 percent on its HMO plans, which account for more than half of the individual market this year.Kaiser Permanente, the only other insurer selling on the exchange, is seeking a 37.4 percent average increase on its HMO plans, which cover just over a third of Obamacare customers.

A couple of days ago, I posted that Virginia has become the first state out of the gate with their preliminary 2019 premium rate requests for ACA individual policies. However, I made sure to emphasize that these are preliminary requests only; carriers often resubmit their rate change requests more than once over the course of the summer/fall, and even that may not match whatever the final, approved rate changes are by the state insurance commissioner.

In addition, I generally try to make it understood that there's alotof room for error here--the weighted averages are based on the number of current enrollees, but of course that number can change from month to month as people drop policies or sign up during the off-season (via Special Enrollment Periods). Even then, the rate filing paperwork is often vague or confusing about just how many enrollees they actually have in these plans. Sometimes wonks are reduced to taking the number of "member months" and dividing by 12 to get a rough idea of how many people are enrolled in any given month. Sometimes the only number of enrollees available are from last year, which could bear zero resemblence to how many are currently enrolled. Sometimes the only number available is how many people the carrier expects to enroll in their policies next year. And so on.

IMORTANT UPDATE: As I suspected, it turns out that the stray rate filing posted to the California Insurance Dept. website a few days ago was posted prematurely, doesn't reflect the carrier's final* rate filing, and has since been pulled from the California Insurance Dept. website.

I've been asked to remove the filing data, and seeing how there's nothing nefarious about it (I wasn't "whistleblowing" evidence of anything criminal/unethical), I'm complying with that request. Since everything in the post related to that data, there wasn't much point in keeping the rest of it either.

*(Yes, I'm aware that none of these early filings are "final" since they tend to be revised/resubmitted throughout the summer/fall, but you know what I mean.)

...and to absolutely no one's surprise, GOP sabotage of the ACA will be directly responsible for a significant chunk of the individual market premium increases.

Every year for 3 years running, I've spent the entire spring/summer/early fall painstakingly tracking every insurance carrier rate filing for the following year to determine just how much average insurance policy premiums on the individual market are going to increase (or, in a few rare instances, actually decrease).

The actual work is difficult due to the ever-changing landscape as carriers jump in and out of the market, their tendency repeatedly revise their requests, and the confusing blizzard of actual filing forms which sometimes make it easy to find the specific data I need and sometimes make it next to impossible.

NOTE: Just to clarify, here's where the headline comes from:

...Sponsoring Sen. Mike Shirkey, R-Clarklake, created exemptions in the Michigan legislation that would waive the work requirement for parents with young children, pregnant women or caretakers for disabled family members. But asked about people like Maitre who could still lose health care, he told reporters the social safety net “by definition, has a lot of holes in it.”

“The best safety net ever invented by God is family,” Shirkey said, “but I’m not sure that government is supposed to supplement that process.”

Well, here we go:

#BREAKINGtomorrow morning the House Appropriations Committee is taking up SB 897. Another Republican attempt to take away healthcare from Michigan familieshttps://t.co/WsUhyntINj

Time and opportunity still exist to replace Obamacare.

...I reported in January that a number of conservative groups, under the leadership of former Sen. Rick Santorum, was working hard to craft a new Obamacare replacement...Behind the scenes, those groups...have continued to meet and tweak their plan, and they seem just a few weeks away from being able to unveil it.

...I listened in on a March 21 conference call among numerous interested parties, and received further updates within the past week from Santorum.

Enrollment in the federally facilitated marketplace has dropped 9 percent over the past two years, with a nearly 40 percent drop in new enrollment, while enrollment in state-based marketplaces remained steady during the same period.

Nothing new under the sun here; this is the core of what I do at ACASignups.net. In fact, this press release underplays the point slightly: The official enrollment tallies are down 10% on the federal exchange since 2016 and up 1.5%, although the discrepancy might be partly due to Kentucky shifting from state-based status to federal status in 2017.

Former Acting CMS Administrator Andy Slavitt and Huffington Post healthcare reporter Jeff Young have each written up a fairly comprehensive list of the various types of ACA/healthcare sabotage which the Trump Administration and/or other Republicans in Congress or at the state level have attempted (or are in the process of attempting today).

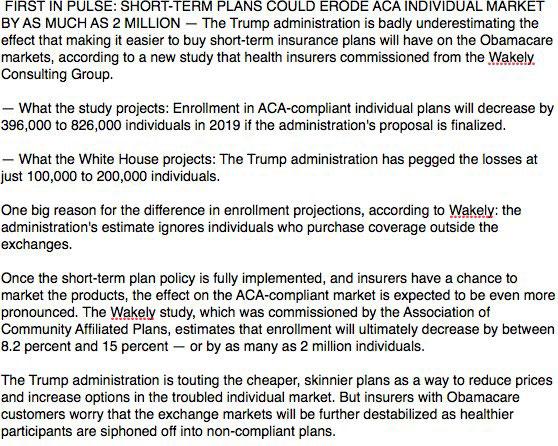

WAIT, I MISSED THIS: The Trump Administration DIDN’T INCLUDE OFF-EXCHANGE ACA POLICIES in their 100K - 200K projection?? I heard something about it but assumed they were just pulling numbers out of their asses. This is actually worse in some ways. https://t.co/S2qJetjdTS