Louise Norris has done the heavy lifting for me regarding Rhode Island's 2016 rate change requests. Then again, there's only 3 companies operating on the exchange anyway (and I don't see any other companies operating off-exchange only, so I assume that's it for the state's individual market):

Of the three carriers that offer individual plans in HealthSource RI, only one –UnitedHealthcare of New England – shows up on the rate review tool that HHS is using to publish proposed rate hikes of ten percent or higher. United is requesting an average rate increase of about 11 percent for their Compass individual plans.

Blue Cross Blue Shield had also initially proposed weighted average rate hikes of 11 percent for their individual market plans in RI, but in early July, the carrier revised their projection to a weighted average rate increase of just 7 percent. The lower rate is partially due to the fact that in the FY 2016 budget (see below), the HealthSource RI premium fee is lower than initially proposed.

Alaska Governor Sidesteps GOP-Controlled Legislature, Expands Medicaid On His Own

Alaska will become the 30th state to accept Obamacare’s optional Medicaid expansion, after Gov. Bill Walker (I)announced on Thursday that he will use his executive power to bypass the GOP-controlled legislature and implement the policy on his own.

Walker — a former Republican who has since become an Independent — has been advocating for Medicaid expansion for over a year. Implementing this particular Obamacare provision, which was ruled optional by the Supreme Court in 2012, would extend health coverage to an estimated 40,000 low-income residents in his state. Polling has found that the majority of Alaska residents agree with Walker’s position.

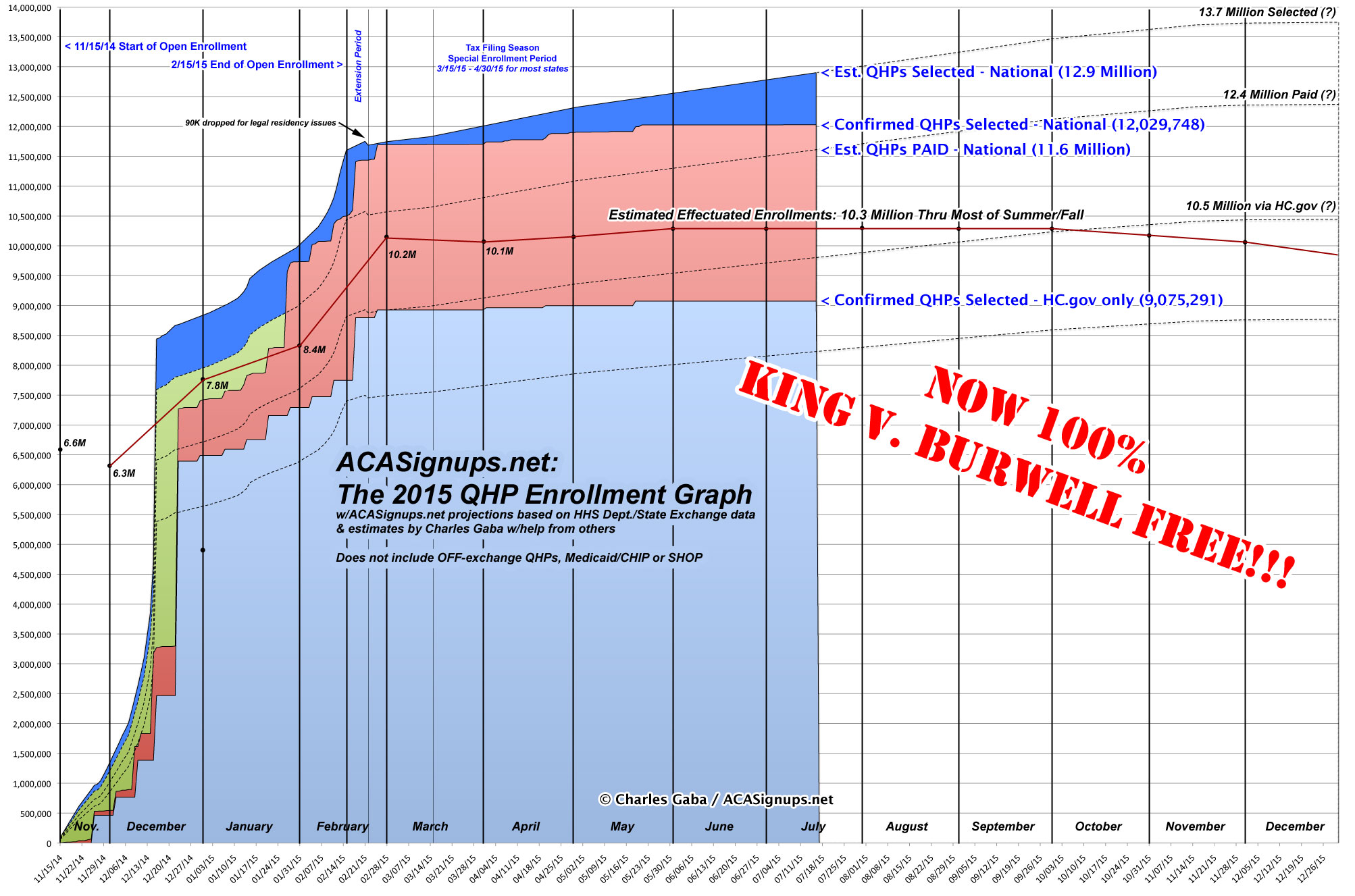

This may not seem like a Big Deal to anyone but myself, but I've decided to bump up my estimate of the currently effectuated ACA exchange QHP tally from 10.3 million (which is what I've been estimating ever since the March HHS report came out) to 10.4 million, where I expect it to hover until right around the point that the 2016 Open Enrollment period kicks off in November.

I'm basing this modest increase on the latest enrollment data out of 4 states: Washington, Colorado, Maryland and Massachusetts, each of which is showing stronger retention numbers (or, in some cases, net increases) since March:

Whoa, Nelly! Ask and ye shall receive...I was just sent a copy of the June report from the Massachusetts Health Connector, and there's some fasinating healthcare data nerd stuff included.

I've pasted screen shots of every page of the report below (and there's a link to the PDF version at the bottom), but here's the main takeaways:

Effectuated QHPs have reached nearly 166,000...a whopping 40,520 higher than at the end of Open Enrollment!

While the national effectuation number is likely only 2% or so higher today than it was in March (likely 10.3 - 10.4 million vs. 10.2 million), in Massachusetts it's 32% higher. There's two main reasons for this, both connected to "ConnectorCare", which is unique to Massachusetts. ConnectorCare consists of the same low-end Qualified Health Plans that anyone can purchase (ie, they're still counted as QHPs in the national tally), except that in addition to the federal Advanced Premium Tax Credits (APTC), enrollees in ConnectorCare also receive additional state-based financial assistance, making them even more attractive to enrollees. In addition, however, unlike "normal" APTC or Full Price QHPs, which are limited to the official open enrollment period for most people, ConnectorCare enrollment, like Medicaid/CHIP, is open year round. That makes a dramatic difference, as you can see below; over 85% of the net QHP enrollment increase since March is thanks to ConnectorCare additions.

In addition, MA is the only state I know of which actively reports their attrition numbers--that is, so far this year they've had 13,635 people drop their QHP policies, meaning a total of 179,557 people have selected a plan and paid at least their first monthly premium.

Assuming a 90% payment rate (confirmed for Massachusetts back in April), this also suggests that the cumulative QHP selection total should be roughly 200,000 people to date, which is only significant to me and The Graph.

When you add the MA factor to the other state-level numbers I've received from Washington State, Colorado and Maryland, this is very strong evidence that the current effectuated number as of July nationally is more like 10.4 million vs. the 10.3 million I've been assuming.

But wait, there's more! Look below and you'll see a whole mess of pie charts, bar charts and line charts, breaking out everything from Metal Level selections and Market Share by Provider to SHOP enrollments (5,247 lives covered as of July 1st) and even Dental Plans!

Not sure how this one got by me, but the Maryland Health Benefit Exchange actually released some updated enrollment numbers over a week ago:

Nearly a half-million Marylanders — 493,346 — have enrolled in quality, affordable health coverage through Maryland Health Connection for 2015.

That includes 126,346 people enrolled in private Qualified Health Plans and 367,000 enrolled in Medicaid from Nov. 15, 2014 through July 5, 2015. About 92 percent of enrollees through the state’s health insurance marketplace are receiving some form of financial assistance.

Medicaid enrollments are year-round. And while open enrollment for private health insurance for 2015 coverage ended in February, people may still enroll if they have a qualified “life event.”

The "92% receiving financial assistance" bit is slightly misleading; that's true, but only because the Medicaid enrollees are lumped in. If you're talking about QHPs only, it's more like 69% (87.2K out of 126.3K). Whether that's a good or bad thing obviously depends on your POV.

The official tally of QHP selections nationally during the 2015 Open Enrollment Period (from 11/15/14 - 2/22/15) was 11,688,074 people.

The actual number of people still enrolled in effectuated plans (i.e., active) as of March 31, 2015, according to the HHS Dept., was 10,187,197 people. That's a net reduction of exactly 1,500,877.

On the surface, that may look bad, but bear in mind that with a 90% payment rate (which I suspect is actually pretty close to the non-ACA industry standard, and which is about 2 points better than last year), that means only about 10.5 million of the original enrollees would have been expected to actually be enrolled in March anyway. That leaves another 332,000 people who presumably paid up for January, February and/or March, but had dropped their policies by the end of March.

When you have diarrhea of the mouth and a "TEN BILLION DOLLAR" megaphone as Donald Trump does, sooner or later you're going to shoot your mouth off about every conceivable topic under the sun. I knew it was just a matter of time before he got to the Affordable Care Act, and while I didn't know exactly what he'd say, I knew that whatever it was, it'd be easily debunked.

Donald Trump, the celebrity businessman who has shaken up the Republican presidential race, has been attacking both Republicans and Democrats in his speeches and interviews. At one point in a July 11, 2015, speech in Phoenix, he took aim at the Affordable Care Act, President Barack Obama’s signature health care law.

He singled out the healthcare.gov website, which was unveiled in the fall of 2013 with a panoply of bugs and glitches, calling it "the $5 billion website for Obamacare, which never worked. Still doesn't work."

PolitiFact does a pretty good job of debunking both claims.

The obligatory update. Assuming around 7,500 off-season QHP selections per day nationally, the grand total should cross the 12.9 million milestone sometime this week if it hasn't already, and should pass the 13 million mark at the end of July.

This won't likely have any impact on the currently effectuated number of course, which is likely still hovering around the 10.3 million mark due to non-payments and normal attrition, although some limited evidence from Washington State and Colorado suggests that this might be a bit higher--perhaps 10.4 million or so.

Last week I noted that of the 33 million people still uninsured in the United States, around 6.5 million of them can't be covered via Affordable Care Act provisions because they're undocumented immigrants, who aren't legally allowed to #GetCovered via either the ACA exchanges (private coverage) or Medicaid expansion (public coverage). Another 3.7 million legal residents/citizens, of course, are caught in the Medicaid Gap. I also brought up the undocumented immigrant factor in a piece yesterday trying to break out the other portions of that 33 million total.

Anyway, in the comments, "dawgitall" asked a reasonable question: If there's around 11 million undocumented immigrants in the U.S. total (everyone seems to agree on that estimate), and 6.5 million of them aren't insured at all, what's the deal with the remaining 4.5 million?

Last week, after the latest quarterly Gallup survey came out stating that the uninsured rate among U.S. adults had dropped to just 11.4%, I did some number-crunching and pointed out that:

About 6.5 million of those 33 million are undocumented immigrants who are therefore not eligible for coverage via the ACA anyway

Another 3.7 million are folks caught in the "Medicaid Gap" in 21 Republican-controlled states...these are people who a) make less than 100% of the federal poverty line (making them ineligible for federal tax credits to purchase private policies) but b) aren't eligible for traditional Medicaid either, meaning they're basically screwed.

When you subtract those two populations, it leaves roughly 22.8 million people who are still uninsured. So, who are they?

Well, according to the Kaiser Family Foundation, as of 2014, there were roughly 13.8 million uninsured eligible for Medicaid (either traditional or via ACA expansion). Since then, thanks to several more states going through with expanding the program (Pennsylvania, Indiana and, any day now, Montana), this number has increased to around 14.3 million. According to the March Medicaid report released by CMS in June, there's been a net increase of 12.2 million Medicaid/CHIP enrollees since 2013 (I'm not including the 950K "bulk transferees" brought onto the program prior to October 2013, since most of those were already covered by some other state-run program).