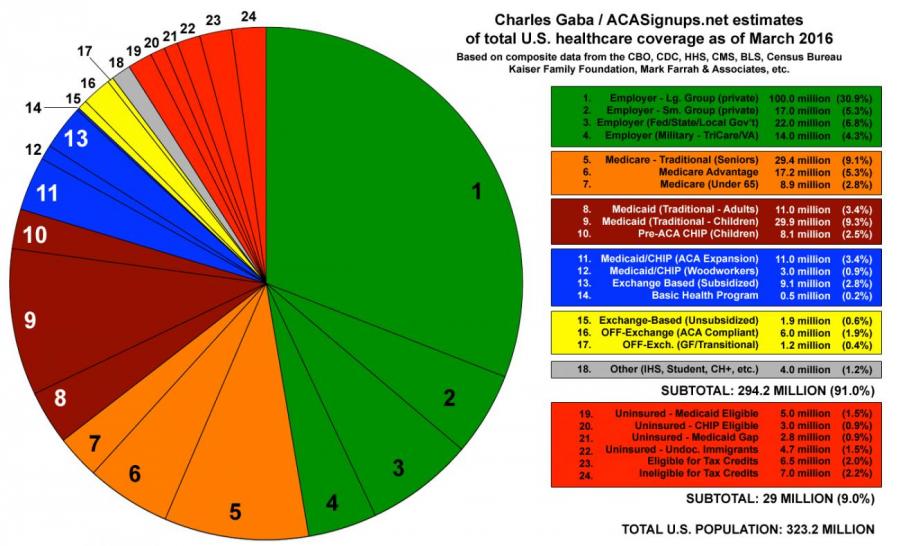

Given the massive backlash/debate going on over the impending (supposed) repeal of the Affordable Care Act, there seems to be one particular fact which a huge number of Obamacare opponents (and even many supporters of the law) don't seem to be aware of.

One of the big talking points among ACA opponents is "Why should my hard-earned tax dollars go to subsidize someone else's lazy ass?"

Now, aside from the fact that a) "being self-employed" or b) "happening to have a job which doesn't offer health benefits" or c) "being married to/a child of either a) or b)" hardly makes one "lazy", there's something which these folks should know:

nearly everyone's healthcare coverage is heavily taxpayer subsidized.

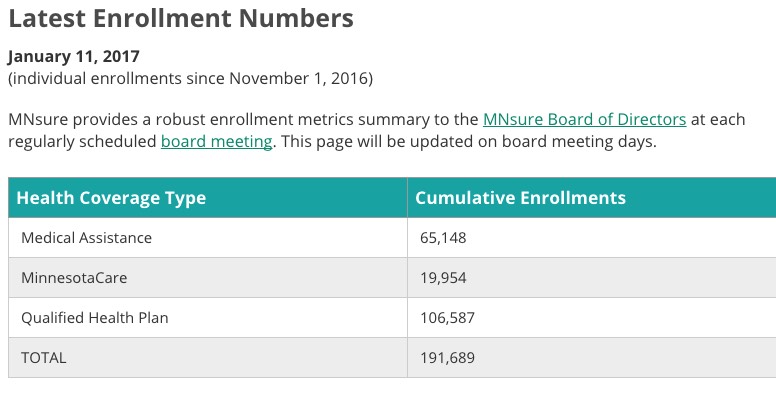

A few days ago I noted that MNsure, Minnesota's ACA exchange, has skyrocketed from last place to first in terms of achieving my personal OE4 enrollment targets, having enrolled 103,578 people in Qualified Health Plans (QHPs), plus another 19,960 in MinnesotaCare (MN's BHP program) and 65,164 in Medicaid.

Yestrerday they updated their numbers once again:

That's a further increase of 3,009 Minnesotans in QHPs in the past week or so. MN has already blown past my original projection (86K) and has reached 92% of my revised target (116K).

A few days ago I had the honor of joining healthcare reporter Jonathan Cohn and healthcare patient advocate Amy Lynn Smith as a guest on The Sit & Spin Room, a podcast presented by Michigan's best political website, Eclectablog, featuring hosts Chris Savage and the mysterious @LOLGOP.

Cohn is the guest for the first half-hour, while Smith and I join in for the remaining hour of the show.

This isn't a particularly dramatic update given that CMS released their "mid-season" report yesterday, which already updated Washington's tally from 180K thru 12/20 to 194K as of 12/24...but an update's an update:

The Washington Health Benefit Exchange today announced that more than 200,000 customers have selected 2017 health and dental coverage through Washington Healthplanfinder since the open enrollment period began on Nov. 1 – an increase of almost 14 percent over the same point last year.

Hmmmm...the numbers look good, but that "...and dental" caveat is a bit troubling. I've asked for clarification; it's possible that the "dental" reference simply refers to the fact that some Qualified Health Plans also include dental coverage, as opposed to referring to standalone dental plans, which shouldn't be counted as QHPs.

OK, with this morning's CMS/ASPE "mid-season report" being released, I figured this would be a good time to take a look at where things stand on both a state-by-state and national level. All of the state enrollment numbers should be accurate with the possible exception of California; there's a potential discrepancy of around 93,000 enrollees which I'm still trying to clarify. The tables/graph below all assume that those disputed 93K are supposed to be included.

Here's my original projections for each state, sorted in order based on what percent of my personal target each state has reached. As you can see, Minnesota, Hawaii, Massachusetts and South Dakota have already broken 100%, with Utah, Vermont, Oklahoma, Wyoming, Colorado, Oregon and (possibly) California all over the 90% mark. Any state over 90% at this point should hit my targets by the end of January.

For the past couple of weeks I've been compiling the county-level data across various states for just how many people are at risk of losing healthcare coverage if the Republican Party actually does follow through with repealing the Affordable Care Act. The main numbers are the subsidized QHP enrollees and the Medicaid Expansion enrollees.

What people really want, though, given the politics of the situation, are these numbers by Congressional District. Unfortunately, I can't provide that, which is why I'm going with County level data for now.

As I've noted before, until today, there was one state which I had no OE4 data for whatsoever: Vermont (which is ironic given their historic support of healthcare reform, including Sen. Bernie Sanders). This blank has been filled in by today's supplemental CMS/ASPE report: 29,021 QHP selections as of 12/24, which is actually quite a bit higher than I expected for the state (my target for VT is only 30,000 total through 1/31).

As regular readers know, I've always made sure to report the number of people who enroll in the ACA's Basic Health Plan (BHP) programs in Minnesota (since 2014) and New York (since 2016). The HHS Dept. didn't really highlight BHP numbers in 2014 or 2015 because they weren't even a rounding error nationally (they had 43,000 enrolled in BHPs via MNsure in April 2014, for instance). In addition, the BHP program in Minnesota was really just a retooling/expansion of an existing program anyway. As a result, it was treated as more of a footnote in the national reports. Interestingly, the number of MN residents enrolling in BHPs through MNsure this year is quite a bit lower (20,000), although state-wide the number is much higher (around 62,000 as of this week). Basically, 1/3 of MinnesotaCare enrollees are doing so via the ACA exchange, the rest via traditional state agencies/processes.

Don't get excited yet. This isn't remotely settled yet, and even if the GOP backs off now, there's no reason to think they won't be back in full force a few months down the road.

GOP Senators Propose Delay On O'Care Repeal To Work Out Replacement

After publicly airing some of their grievances with the GOP's current strategy of repealing Obamacare without a replacement plan, a handful of Republican senators put their concerns in legislative writing. Five senators on Monday evening introduced a measure that would delay the next steps on repealing the Affordable Care Act by more than a month. The senators, in their statements accompanying the provision, said the delay would buy Congress more time to work out of the the details of a replacement.

Minnesota is a different story. They started out Open Enrollment with a bang, racking up enrollees at up to 12x last year's pace...but that was mainly due to their unique "enrollment cap" policy this year. Once the caps were filled and current enrollees were all squared away, new enrollments appear to have dropped off dramatically. They're now dead last percent-of-target wise (again, I can't include NY or VT here since neither has enough data available).