However, the DC exchange board was also working quickly in an attempt to counter the Trump Administration's #ACASabotage factors, by voting to restrict short-term plans, to lock in DC's Open Enrollment Period at a full 3 months as in years past, and to reinstate the ACA's individual mandate penalty at the local level.

WASHINGTON (Reuters) - Republicans could try again to repeal Obamacare if they win enough seats in U.S. elections next month, Senate Republican Leader Mitch McConnell said on Wednesday, calling a failed 2017 push to repeal the healthcare law a “disappointment.”

...except that the headline understates what McConnell actually said:

...On Nov. 6, Americans will vote for candidates for the Senate and the House of Representatives.

McConnell’s Republicans now hold majority control of both chambers. Democrats will try to wrest control in races for all 435 House seats and one-third of the 100 Senate seats.

Despite their dominance of Congress and the White House, Republicans dramatically failed last year to overturn former President Barack Obama’s signature healthcare law, known as Obamacare. McConnell called it “the one disappointment of this Congress from a Republican point of view.”

(note: this is a work in progress...check back soon for more additions.)

As I noted yesterday, as the 2018 midterm election rapidly approaches, there's been a sudden and complete change in strategy when it comes to healthcare policy campaiging by practically every Republican running for office this year. After nearly a decade of doing everything in their power to attack, undermine, sabotage, hack away at, trash and especially repeal the Patient Protection and Affordable Care Act (that's the full title of the law, after all), GOP candidates have suddenly decided that "protecting coverage of pre-existing conditions" is a swell idea after all.

Premium Rates for Individual and Small Group Markets Individual plan premium rates may vary by age, rating area, family composition and tobacco usage. For example, a person living in Manhattan, KS (rating area 3) may pay a different rate than someone living in Pittsburg, KS (rating area 7) based on the claims data by rating area. A map of the counties included in each rating area is provided on the next page. Kansas is an effective rate review state, which means the actuarial review is conducted by the Kansas Insurance Department. KHIIS (Kansas Health Insurance Information System) claims data is utilized during the rate review process to verify the claims experience submitted by the companies. The following table provides details regarding the average requested rate revisions for companies writing individual policies in Kansas. Rate increases will be partially offset for individuals receiving a premium tax credit.

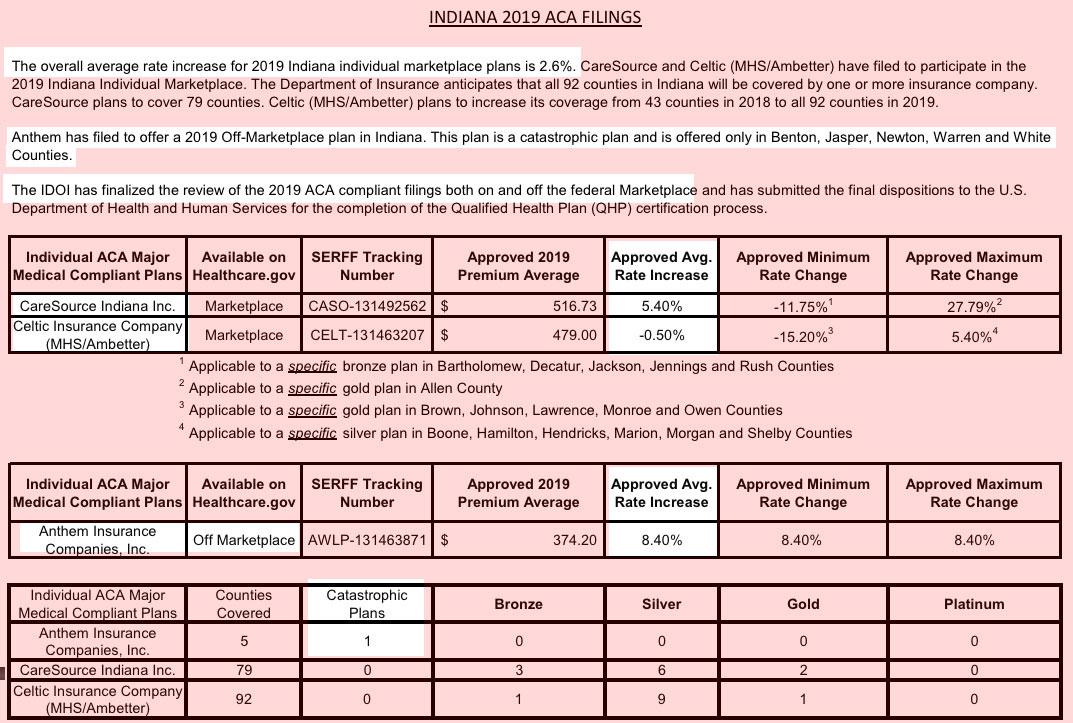

Back in June, Indiana's 3 individual market carriers submitted their requested 2019 ACA rate changes, which averaged around 5.1%. At the time I also pegged the impact of #ACASabotage on 2019 rates (mandate repeal + #ShortAssPlans) at around 13 percentage points.

The Department of Insurance received preliminary 2019 health plan information from insurance carriers on June 1 and began reviewing the proposed plan documents and rates for compliance with Idaho and federal regulations. The Department of Insurance does not have the authority to set or establish insurance rates, but it does have the authority to deem rate increases submitted by insurance companies as reasonable or unreasonable. After the review and negotiation process, the carriers submit their final rate 2019 increase information. The public is invited to provide comments on the rate changes. Please send any comments to Idaho Department of Insurance.

A few days ago, Jonathan Cohn of the Huffington Post wrote about a new phenomenon sweeping the nation: Republican candidates, all of whom have repeatedly either voted to repeal the Patient Protection & Affordable Care Act or who have repeatedly called for it to be repealed, are suddenly falling all over themselves to try and claim that they support patient protections for those with pre-existing conditions...usually by invoking family members who suffer from various ailments.

Cohn's examples include GOP Congressman Mike Bishop (MI-08), who claims his wife has rheumatoid arthritis; Dana Rohrabacher (CA-48), who says his daughter survived childhood leukemia; John Faso (NY-19) and Mario Diaz-Balart (FL-25), both of whose wives survived cancer; and Josh Hawley (MO-AG, running for MO-Sen), whose son has a rare chronic disease.

Yes, that's right...while the 2019 Open Enrollment Period doesn't start for the rest of the country until November 1st, the Golden State has decided to kick things off two weeks early (16 days early, technically): Covered California, the largest state-based ACA exchange, is officially open for business for 2019 enrollment as of today!

In addition, while you can't actually enroll for 2019 coverage in any other state until November 1st, in several states you can window shop to find out what your 2019 policy options and pricing will be, along with estimates about what sort of financial assistance you'll qualify for once you actually do go through the enrollment process.

The states which are already open for window shopping already include:

UPDATE 10/30/18: Thanks to some additional reviews/checking by Dave Anderson, Louise Norris, Andrew Sprung and myself, I've been able to update the spreadsheet further; the blog post has also been updated correspondingly.

Last year, while Congressional Republicans were doing everything possible to officially repeal the Affordable Care Act via legislative means, Donald Trump spent months repeatedly threatening to cause the ACA individual market exchanges to either "explode" or "implode" (depending on the day) by, among other things, cutting off Cost Sharing Reduction reimbursement payments to insurance carriers.

For as much as I write about healthcare policy, I actually don't write about Medicare itself all that often...at least not Medicare as it's defined today.

CMS announces 2019 Medicare Parts A & B premiums and deductibles

Today, the Centers for Medicare & Medicaid Services (CMS) announced the 2019 premiums, deductibles, and coinsurance amounts for Medicare Parts A and B.

{kind=link}