(sigh) Regular readers know two things about me when it comes to Sen. Elizabeth Warren:

I'm generally supporting Elizabeth Warren in the Democratic Primary (not a full endorsement, but I've been strongly leaning her way for awhile now)...

...but I'm also not happy with her seeming 180 degree shift on how to best achieve universal healthcare coverage from her brilliant CNN Town Hall response in March to her cut 'n dried "I'm with Bernie" stance since June.

HOWEVER, for the time being at least, that seems to be where she's decided to lay her marker, so it is what it is.

The single biggest headache she's been dealing with all summer and fall, however, has been the "Will You Raise Taxes On The Middle Class" question which keeps popping up in interviews and the Democratic debates. Bernie Sanders has, to his credit or detriment, stated it plainly: Yes, his plan would indeed raise taxes on households earning more than $29,000/year.

I'm not sure how this slipped by me, but in addition to Covered California already having launched their 2020 Open Enrollment Period yesterday, five other state-based ACA exchanges are already partly open as well. That is, you can shop around, compare prices on next year's health insurance policies and check and see what sort of financial assistance you may be eligible for:

I'm not sure when the other 7 state-based exchanges will launch their 2020 window shopping tools, nor do I know when HealthCare.Gov's window shopping will be open for the other 38 states, although I believe they usually do so about a week ahead of the official November 1st Open Enrollment Period launch date.

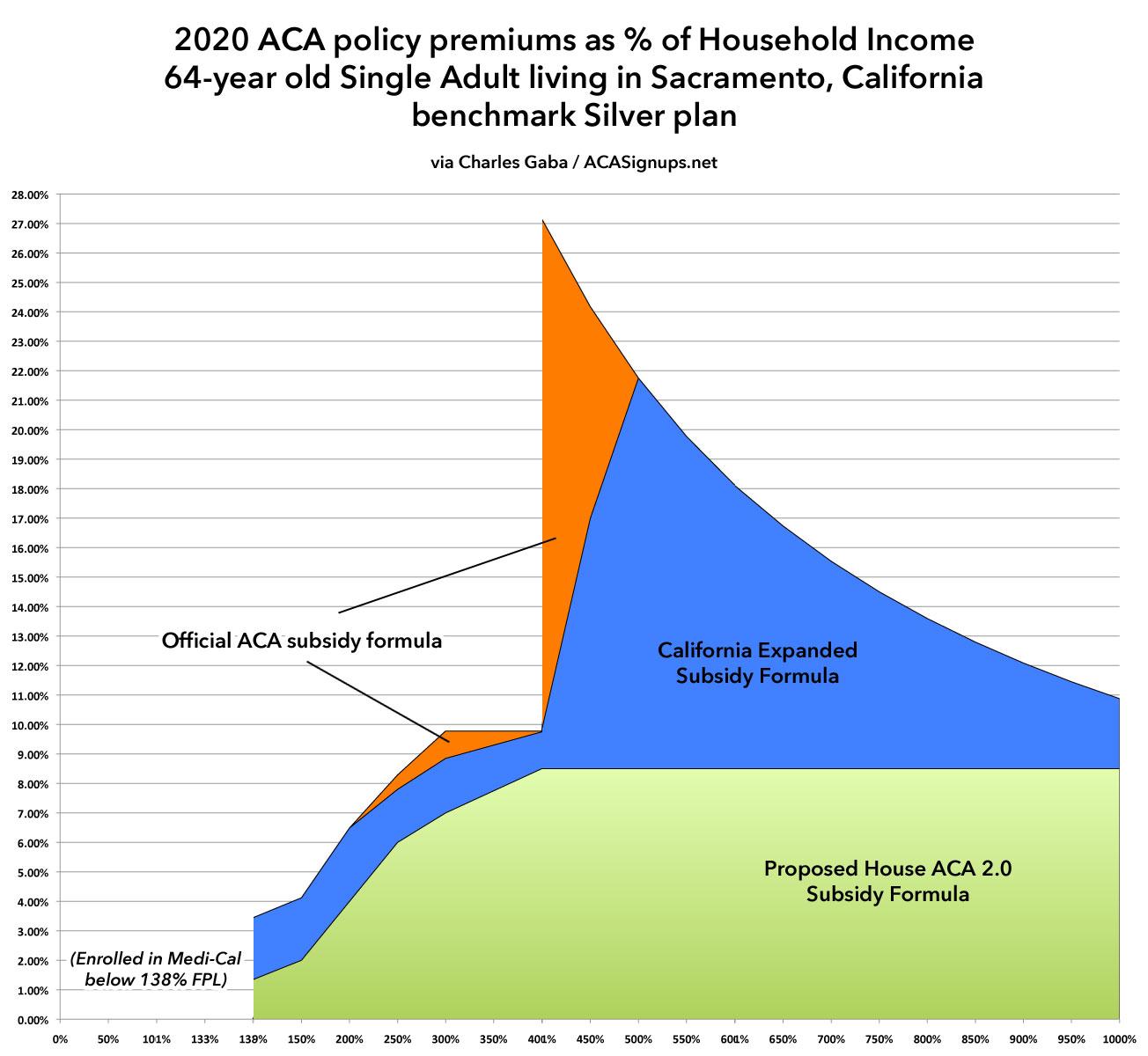

I also noted that there's two important points for CA residents to keep in mind starting this Open Enrollment Period:

First: The individual mandate penalty has been reinstated for CA residents. If you don't have qualifying coverage or receive an exemption, you'll have to pay a financial penalty when you file your taxes in 2021, and...

Second: California has expanded and enhanced financial subsidies for ACA exchange enrollees:

Until now, only CoveredCA enrollees earning 138-400% of the Federal Poverty Line were eligible for ACA financial assistance. Starting in 2020, however, enrollees earning 400-600% FPL may be eligible as well (around $50K - $75K/year if you're single, or $100K - $150K for a family of four). In addition, those earning 200-400% FPL will see their ACA subsidies enhanced a bit.

While the 2020 Open Enrollment Period doesn't officially start until November 1st across the rest of the country, in California it begins two weeks earlier, for whatever reason:

In most states, open enrollment for 2020 coverage will run from November 1, 2019 to December 15, 2019. But California enacted legislation (A.B.156) in late 2017 that codifies a three-month open enrollment period going forward — California will not be switching to the November 1 – December 15 open enrollment window that other states are using.

Instead, California’s open enrollment period (both on- and off-exchange) will begin each year on October 15, and will continue until January 15. Under the terms of the legislation, coverage purchased between October 15 and December 15 will be effective January 1 of the coming year, while coverage purchased between December 16 and January 15 will be effective February 1.

I posted Wisconsin's preliminary 2020 rate filings in early August. Yesterday the state insurance department posted this press release, which includes the final, approved rate changes. As far as I can tell, nothing has changed (the final statewide weighted average is a 3.2% average premium reduction over last year, thanks primarily to them implementing a fairly robust ACA Section 1332 reinsurance waiver:

Gov. Evers Announces More Health Insurance Options for Wisconsinites in 2020 Ahead of Open Enrollment

Back in July, the Colorado Insurance Dept. announced the preliminary 2020 avg. premium rate changes for the individual and small group markets, including making the important point that their then-pending Section 1332 Reinsurance Waiver program, if approved, would cut down on unsubsidized premiums by over 18% on average (18.2%, to be precise, according to the CO DOI, although my own analysis based on the preliminary rate filings brought it in at a 17.5% reduction).

As you may recall, I managed to acquire all 2,700 MLR template filing spreadsheets from the CMS website a solid month before the data was made available to the public. After spending countless hours digging through them and compiling the data on a state-by-state basis, I concluded that the final breakout was as follows:

Individual Market: $769 million in rebates being paid back to 3.34 million ACA enrollees

Small Group Market: $312 million in rebates being paid back to 2.96 million enrollees

Large Group Market: $290 million in rebates being paid back to 2.31 million enrollees

TOTAL: $1.37 billion in rebates being paid back to 8.61 million enrollees nationally

With the 2020 Open Enrollment Period rapidly approaching (it actually kicks off on October 15th in California, and on November 1st in every other state + DC), it's important to keep in mind that many people who didn't qualify for financial assistance in 2019 may qualify in 2020...and in some cases that could mean a difference of thousands of dollars due to how the ACA subsidy formula works and other factors.

First, a refresher on how the ACA formula works for Individual Market enrollees (that is, people who are looking to buy health insurance for themselves and/or their family who don't receive it through their employer, Medicare, Medicaid, CHIP or some other source).

Getting ready for MNsure's open enrollment period: what to know and how to prepare

Open enrollment runs November 1 through December 23, 2019

ST. PAUL, Minn. — The MNsure open enrollment period begins in less than one month. To ensure Minnesotans are prepared to shop and enroll in coverage starting November 1, MNsure is highlighting some important information:

Open enrollment is shorter this year — don't miss out on coverage

MNsure's open enrollment period for 2020 health and dental coverage will be seven weeks long — beginning November 1, 2019, and ending December 23, 2019. Minnesotans should note that open enrollment is shorter than previous years and all those who enroll during open enrollment will have a start date of January 1, 2020.

MNsure assisters are ready to help — schedule an appointment today

MNsure has a statewide network of expert assisters who can help Minnesotans apply and enroll, free of charge. The assister can be a navigator or a broker.

The South Carolina Insurance Dept. released their final/approved 2020 Individual and Small Group Market premium rate changes a few days ago.

Previously, I only had the unweighted averages, which were a 1.9% decrease on the Indy market and an 11% increase for small group enrollees...but SCDOI has included the weighted averages for each in their approved numbers: A 3.9% drop and 7.6% increase respectively.

It's also worth noting that the Individual market is growing from three carriers to five next year--both Bright Health Co. and Molina Healthcare are joining the South Carolina market for the first time.

{kind=link}