NOTE: I originally posted this at 3:00pm October 1st. Shortly after that, I heard the news about the Oregon massacre. I seriously debated changing the headline, but decided that it was completely appropriate under the circumstances. If you disagree...well, we just have to disagree.

In 1991, conservative writer/humorist P.J. O'Rourke wrote a book called, fittingly enough, "Parliment of Whores". It was, as the title explains, "A Lone Humorist Attempts to Explain the Entire U.S. Government". The 9th chapter is entitled "Would you kill your mother to pave I-95?" The main point of this chapter, as you can probably imagine, is that there's a limited amount of money in any budget which can be set aside for various programs and departments, which in turn means that Tough Choices have to be made all the time:

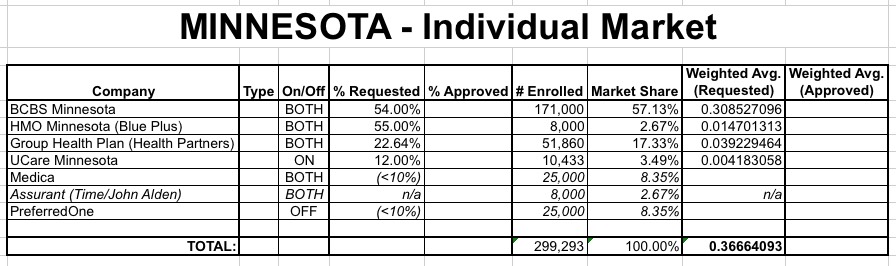

When I crunched the numbers for Minnesota's requested rate hikes, the results were pretty scary-looking; based on partial data, I estimated that the weighted average was something like a 37% overall requested increase:

Note that there were several crucial missing numbers: I didn't know the actual market share for several companies (I made a rough guess based on an estimate of the total missing enrollments), nor did I know what the requested increases were for Medica or PreferredOne, other than thinking that both were under 10%.

With the 2016 Open Enrollment Period quickly approaching (it launches on November 1st), the Maryland Health Connection has already officially launched 2016 Window Shopping!

They even whipped up a simple video stepping you through the process (oddly, the background music seems to have been lifted from "There's Something About Mary", which is either a good or bad omen depending on your POV):

Over the weekend I finally started plugging every state which have 2016 premium hike data for into a chart to see if any patterns were showing up, but I was still missing 6 states. I concluded that Medicaid expansion does not appear to be a major factor (or, at least, not an obvious one), but that there are two other clear trends:

First, states which are allowing "transitional" plans through next year are definitely seeing higher percentage rate hikes than those which stuck to their guns and discontinued non-ACA compliant policies.

Second, states which have only published requested rate changes are currently noticeably higher on average than those which have been put through the regulatory approval process.

Today I'm posting updated versions of all three charts, with some slight updates:

For most of the states I'm analyzing, I have hard enrollment numbers for the insurance carriers requesting rate hikes over 10%; it's the remaining companies (the ones seeking hikes of less than 10%) which are generally the big unknowns.

In Mississippi's case, this is flipped around: There appear to only be 4 companies offering individual policies in the entire state, and while I'm missing the enrollment number for the biggest one (BCBSMS), I can calculate a pretty close estimate due to a unique factor: Neither of the two asking for >10% hikes are offering exchange-based policies:

Assuming subsidies remain in place, none of the individual plans available in Mississippi’s exchange have requested double digit rate increases for 2016. The only exchange plan requesting a rate increase of ten percent or more is a small group plan from United HealthCare. Rate increases of at least ten percent are published on Healthcare.gov’s rate review tool, and the only individual market Mississippi plans on the list are off-exchange.

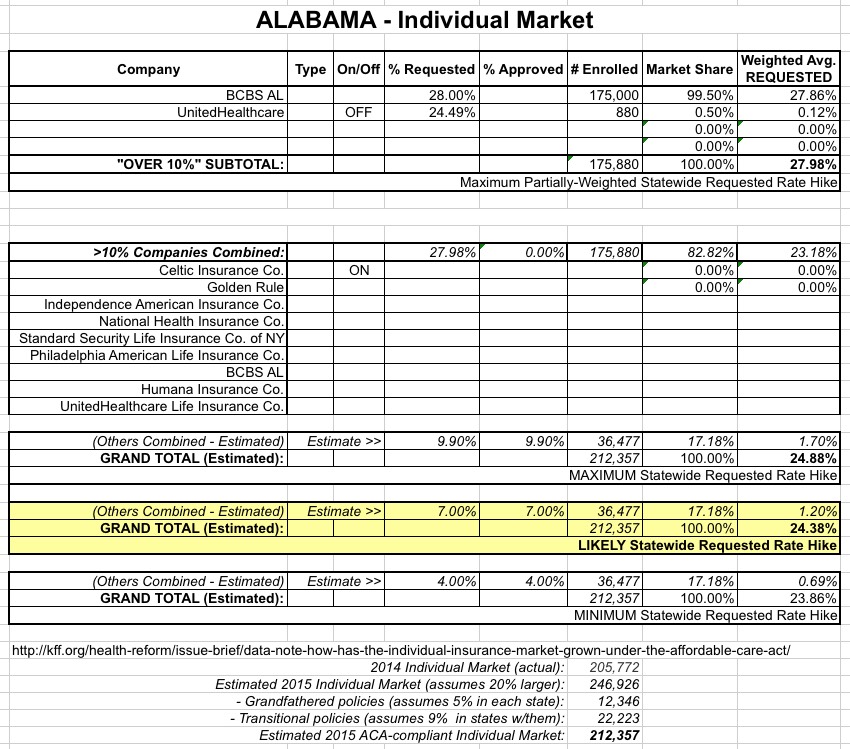

As with many other states, I'm working with limited enrollment and rate change data here, so plenty of caveats abound. However, Alabama's 2014 individual market was only around 206,000 people, and the ACA-compliant market should be roughly the same this year. I can account for 176,000 of that, so the remaining 30K or so are unknown other than being split among a half-dozen companies which requested rate changes of below 10% increases.

Assuming around 7% on average for the balance, Alabama residents are likely looking at roughly a 24.4% rate hike...assuming they stick with their current plans.

In other words: Shop around, shop around, shop around!

There's an old saying: Figures lie and liars figure. Statistics and percentages are a funny thing; as politicians of every stripe know, you can often twist them to mean whatever you like, especially when you don't provide proper (or sometimes any) context whatsoever. Case in point: Yesterday's embarrassingly dishonest "chart" presented by Representative Jason Chaffetz at the Planned Parenthood witchhunt committee hearing.

For a less inflamatory example of this, consider the headline of this entry:

Delaware: *Approved* 2016 rate hikes reduced by 11.4%!!

At first glance, of course, it looks like I'm saying that after going through the regulatory approval process, the individual health insurance premium rates in Delaware are being reduced by 11.4% next year! Hooray!

As part of a renewed attack on the Affordable Care Act, House Republicans grilled Access Health CEO James Wadleigh and the heads of other state health insurance marketplaces Tuesday, saying they had wasted billions of taxpayer dollars on an effort that has raised health insurance deductibles and premiums.

“In many states, physicians aren’t taking any new Medicaid patients. Focusing on uninsured rates is not the only parameter,” Rep. Greg Walden, R-Ore., said.

Last week I made a valiant effort to convert my 2016 individual market percentage rate ncrease project into actual dollar figures--that is, I tried to figure out how much premiums are likely to increase, on average, in each state, in actual dollars. After all, saying that a policy premium "went up 50%" while another "only" went up 5% for the same person doesn't tell you much if the first one started out at $200/month and the second one was already $300/month. Unfortunately, I failed at doing this; way too many variables and too much missing data.

However, I am able to provide a sneak peak at average rates on the New Mexico individual and small group markets next year, for individual enrollees at 5 different ages, in all 5 different coverage regions:

This issue brief reflects lessons learned from how consumers handled the new intersections between health coverage and the tax filing process in 2015. Drawing on public data as well as Enroll America’s private survey research and outreach efforts, this issue brief examines the policy framework underpinning the linkages between taxes and health coverage, messaging considerations and opportunities, and effective partnerships to maximize enrollment. Based on this analysis, the report concludes with recommendations for policymakers and other enrollment stakeholders about how to improve the consumer experience.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}