Hmmmm...I'm still waiting for the Michigan Dept. of Insurance to publicly post the 2017 requested rate hikes (they aren't due until June 20th, apparently), but in the meantime, Blue Cross Blue Shield of Michigan (the largest insurer in the state) decided to issue a press release patting themselves on the back for keeping their small business average rate hike down to 2.9%:

DETROIT, June 8, 2016 /PRNewswire-USNewswire/ -- In contrast to national trends, Blue Cross Blue Shield of Michigan today announced a comparatively small statewide average rate increase of 2.9 percent for small group employers in 2017, pending state regulatory approval. This follows rate reductions that Blue Cross delivered to small employer group customers that renewed during the second half of 2015.

Interesting. When I last checked in on the Maryland exchange, their effectuated QHP enrollment was down about 14% since the end of open enrollment (from 162,177 QHP selections to 139,379 effectuated enrllees as of the end of April).

However, they just posted the following market share breakdown, which shows that they currently have 148,403 Marylanders enrolled in exchange policies, a net drop of just 8.5%. Apparently they've added more people during the off season via SEPs than they've lost due to attrition since April.

Back in April, I attempted to figure out just how many people are still enrolled in Grandathered and/or Transitional (or "Grandmothered") policies on the individual market. My conclusion, based on some very rough estimates, was that the figure is likely somewhere between 800K - 1.4 million Grandfathered enrollees and somewhere between 1.1 - 1.5 million Transitional enrollees.

Today, I decided to try tackling the Transitional side of this problem by taking the direct approach: I visited RateReview.Healthcare.Gov.

Most of my time spent here over the past few weeks has been spent on the "Search ACA-Compliant Products" side, trying to lock down the requested 2017 rate hikes for every carrier offering individual policies in every state. However, there's a second big button available as well: "Search Transitional Products":

I receive most of the HHS/CMS press releases, but this one seems to have slipped by me (furiously checking spam filter...). Fortunately, Bob Herman of Modern Healthcare spilled the beans via Twitter this morning (emphasis mine):

Today, the Department of Labor, Department of Treasury, and Department of Health and Human Services (HHS) issued a proposed rule to revise the definition of short-term, limited duration coverage. Under the new rules, short-term policies may be offered only for less than three months, and coverage cannot be renewed at the end of the three month period. The proposed rule also improves transparency for consumers by requiring issuers to provide notice to consumers that the coverage is not minimum essential coverage, does not satisfy the health coverage requirement of the ACA, and will not prevent the consumer from owing a tax penalty. The proposed changes will help strengthen the risk pool by ensuring that short term limited duration plans are used only as intended, to fill truly temporary gaps in coverage.

First, let's hear it for the Oxford Comma, everyone!!

Ever since my infamous clash with Avik Roy over the "how many exchange enrollees are newly insured?" brouhaha over two years ago, one issue which has always been kind of fuzzy has been the question of exactly how many OFF-exchange individual healthcare policy enrollees there are. Since most carriers don't like to break out their enrollment numbers in too much detail for competitive/trade secret reasons, and many states don't require them to do so, this makes tracking the off-exchange numbers pretty difficult.

Just yesterday I posted the Washington Healthplanfinder's latest monthly report, which showed either 177,613, 170,267 or 167,827 people currently enrolled in exchange QHPs statewide, depending on whether you go by the number who have "selected plans", the number that the carriers have reported as being paid up or the number who the exchange has recorded as having paid.

The first number has been pretty confusing to me over the past few months, because the actual number of people who selected QHPs during the 2016 open enrollment period was reported as just over 200,000 by both the exchange itself as well as in the official national ASPE report, so I wasn't quite sure whether to report the net effectuated enrollment drop since then as being almost none at all or around 15%. I finally went with the 15% figure because dividing into the 177K number just didn't make sense by any other measure.

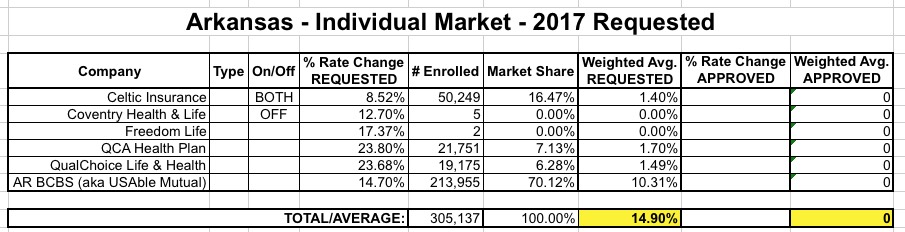

So just last Friday I posted the weighted average requested rate hikes for the Arkansas individual market; it came in at 14.9% overall, which is actually one of the lower statewide averages this year. As a reminder, here's what how the breakout looks:

OK, so 3 major carriers asking to jack up rates 15-24%, plus one at 8.5% and two others with just 7 enrollees between them (one of which is, once again, Freedom Life Insurance). So what?

As regular readers know, I'm currently in the thick of my state-by-state analysis of the requested, weighted average rate changes for 2017 by insurance carriers for the entire ACA-compliant individual market. As of this writing, the overall average looks like it's just a hair over 20% across 28 states + DC.

Does the first sentence above include a lot of clarifiers? Yes, yes it does...and with good reason. I try to be very specific when I discuss this stuff, because it's very easy to get confused about what a given number is actually referring to.

For instance, a few days ago, Avalere Health released their own analysis which concludes that the average requested/proposed premium rates are around 12%. If I left it at that, you might think that either my average is 8 percentage points too high...or that Avalere's is 8 points too low.

Thanks to commenter "Junaed S" who directed me towards this simple, cut 'n dry PDF from the Connecticut Dept. of Insurance detailing the requested rate hikes for the CT individual and small group markets for 2017:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}