OK, I actually have 3 different sources for these Massachusetts numbers, and the dates and classifications overlap a bit so bear with me.

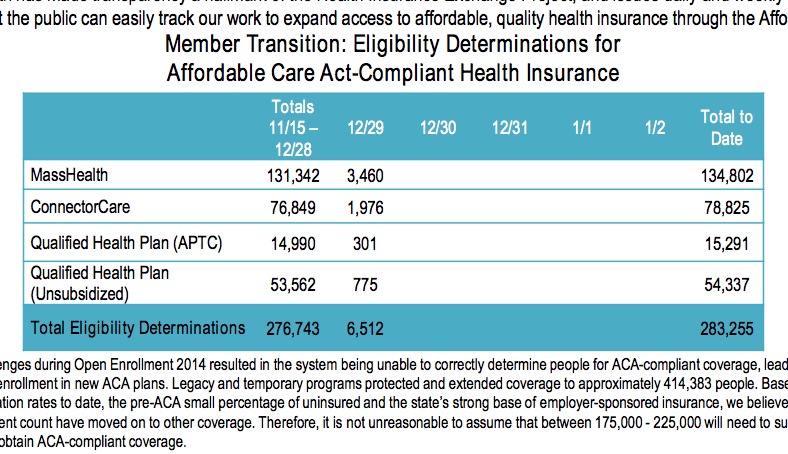

First, we have today's daily MA Health Connector Dashboard report, which states that there have been 148,453 QHP determinations thorugh yesterday (12/29). Assuming 50% of these have selected plans, that's around 74,200 QHP selections to date. In addition, the 134,803 Medicaid (MassHealth) enrollments are already locked in.

However, there's also this story from Felice J. Freyer of the Boston Globe from 12/28 (about a jaw-droppingly poor bit of timing by private, for-profit corporation Dell to install some sort of major software update which caused the payment system to be unavailable for 12 hours on the payment deadline), which pins down the numbers a bit further:

As of Dec. 28, a total of 146,529 Marylanders have enrolled in quality, affordable health coverage for calendar year 2015 since the 90-day open enrollment period began Nov. 15. That includes 83,735 individuals enrolled in private Qualified Health Plans (QHP) and 62,794 individuals enrolled in Medicaid.

At 83,735 enrollments so far, MD has now enrolled 24% more people than they did during all of the 2014 open enrollment period (67,757 thru April 19th).

Put another way, they've enrolled 375 people per day since their January deadline, which is still 11% faster than the 338/day they averaged during the first open enrollment period (including the December and March surges).

Add another 62,794 to Medicaid and MD's turnaround for 2015 is quite impressive indeed.

These numbers are pretty good for DC...except that there's an important caveat: They're all cumulative numbers since October 1st, 2013, making it trickier to parse out:

More Than 71,000 People Enrolled in Health Coverage Through DC Health Link

Wednesday, December 24, 2014

Enrollment

From October 1, 2013 to December 21, 2014, over 71,500 people have enrolled in health insurance coverage through DC Health Link in private health plans or Medicaid:

18,773 people, including new customers from the 2nd Open Enrollment Period , have enrolled in private health plans through the DC Health Link individual and family marketplace; 37,457 people were determined eligible for Medicaid coverage through DC Health Link; and 15,284 people enrolled through the DC Health Link small business marketplace and members and staff from US Congress.

Fortunately, I have most of the 2014 data as well so we can break this out:

OK, YES, I know that the HHS's monthly ASPE report on ACA enrollment was finally released today. And yes, I know there's been a ton of other state-level data and other news over the past couple of days. However, as I noted on Saturday, I had to go out of town right in the middle of all of this and just got back, so I have a busy afternoon ahead of me bringing everything up to date...

So, let's start out with one of the less-obvious updates: Medicaid expansion in Michigan.

To recap: Estimates of Michigan's ACA Medicaid expansion-eligible population have ranged from 477K - 500K, thus making the enrollment data from the official state website rather eyebrow-raising:

Healthy Michigan Plan Enrollment Statistics

Beneficiaries with Healthy Michigan Plan Coverage: 507,618

(Includes beneficiaries enrolled in health plans and beneficiaries not required to enroll in a health plan.)

*Statistics as of December 29, 2014

*Updated every Monday at 3 p.m.

...it's almost certainly a scam unless you're expecting the call and have verified their identity otherwise.

Yes, I know I'm violating my own earlier notice that I'm off the grid for a couple of days, but this development seems to warrant a quick post.

Earlier this evening I received the following email. I'm not including the sender's identifying information for obvious reasons:

Someone from this website contacted me to help with enrolling in health insurance. They created an account on healthcare.gov with an id of XXXXXXXX@acasignup.net instead of my email address and did not give me the password. I am trying to make some changes to my healthcare coverage and update my information.

I am very concerned with the safety of my information. I thought they were from the health insurance marketplace.

If you could change my id to my email and give me the password I would very much appreciate it.

If not I will assume you are an identity thief and contact the FBI.

I'm expecting a few major ACA-related announcements between now and Tuesday, including:

The first official Monthly HHS ASPE Report on ACA exchange enrollment (that is, the big, fat, 40-page detailed report with enrollments broken out by state, metal level, including both QHPs and Medicaid/CHIP and so on).

This is the same type of report which HHS released once a month last year, and it's the official record for purposes of tracking enrollment. It should include all 50 states plus DC. However, I have no idea whether it will run:

November 15th through November 30th (ie, a partial calendar month, which wouldn't be particularly useful); if so, I'd expect around 930K QHPs via HC.gov and 1.24M total.

November 15th through December 15th (everything up through the enrollment deadline for January coverage in most states; this would be useful, but wouldn't include any autorenewals); if so, I'd expect around 3.52M QHPs via HC.gov and 4.70M QHPs total.

November 15th through December 19th (actually 5 full calendar weeks, which is what I'm guessing it'll include and which would be the most useful, since autorenewals for most states would be included). If so, HHS has already given the total as roughly 6.39M via HC.gov, and I'm estimating roughly 8.52M total (remember, my 8.65M estimate includes 4 extra days, through 12/23).

I'm also expecting press releases from Minnesota, Washington State and of course Massachusetts. Washington's should include their "deadline surge" day enrollments, and Massachusetts should be revealing how many of the 34,138 people who enrolled by their deadline but hadn't actually paid by then made their payment under the wire.

Otherwise, I'm hoping that both New York and California will provide their respective renewal numbers, which should be roughly 1.1 million (CA) and 310K (NY), give or take. CoveredCA said that they won't be giving out their renewal data until January, but I'm not sure how that will work since HHS is supposedly releasing a comprehensive monthly report next week. If there's a big blank spot under CA, then the report will have a huge hole of over a million people, making my estimates kind of pointless.

However, I won't be able to post about any of this, as I'll be unavailable for a few days due to a family commitment. I should be back sometime Tuesday evening, and of course I'll be posting about any developments which took place while I was gone.

About 2.3 million Pennsylvanians are currently enrolled in Medicaid, Gillis said, and as of Dec. 22, about 88,000 households had applied for Healthy PA, with approximately 30,000 additional applications sent to the state from healthcare.gov. The number of applications from each county is not yet available, Gillis said.

The department is still processing applications but, she said, most of the new sign-ups are going into the Private Coverage Option, which is for people who are newly eligible because Healthy Pa.’s income limits — 133 percent of the federal poverty level, with a 5-percent income disregard — will be broader than Medicaid’s are.

PA has around 600K residents eligible for the expansion program, so that's about 20% who have already signed up so far.

Nearly 15,000 people signed up for coverage through D.C. Health Link to begin by Jan. 1, officials announced this week.

The D.C. Health Benefit Exchange Authority reported 1,886 new enrollees and 13,100 people who have re-enrolled in private health insurance plans so far in this second open enrollment period under the Affordable Care Act. Earlier this month,officials said there could be up to 500 applications that weren't completed by the first deadline to obtain health coverage by Jan. 1 because of a glitch in the system's new features. Officials said all of those impacted enrollees would have coverage by Jan. 1.

Between Nov. 15 and Dec. 21, the D.C. Health Link website had 56,318 visitors with 109,058 visits. It fielded 25,667 calls to its customer service center.

OK, that's 14,986 total for DC, and this gets another chunk of renewals off the books.

Maryland's previous update, which included their 12/18 deadline for January coverage was just shy of 80K QHPs, or an average of 2,353 enrollments per day since 11/15.

This weekly dashboard report is really just an official breakdown of the numbers I reported a couple of days ago, as it only runs through 12/23, but it's still good to have an official confirmation of everything: