As I noted last week, Minnesota had around 41,000 people enrolled in 2014 exchange QHPs as of October, and due to PreferredOne dropping off the exchange (with around 60% of the market), along with a state law which requires insurance companies to continue providing the same policy as long as a current enrollee wants to keep it (and keeps paying premiums), that meant that MN's renewal/re-enrollment situation was especially unusual compared to most states.

MNsure will release 2015 enrollment metrics weekly, and will present a more robust metrics summary to the MNsure Board of Directors at each regularly-scheduled board meeting. During weeks that MNsure is closed on Friday, the enrollment metrics update will be released earlier in the week.

Health Coverage Type Cumulative Enrollments

Medical Assistance 26,540

MinnesotaCare 11,152 Qualified Health Plan (QHP) 31,159

TOTAL 68,851

Vermont: I don't have a 12/15 report from the VT state exchange, but they did release one from 4 days earlier. It claimed 25,867 total QHP selections for 2015. The HHS report says it was 21,709...as of 4 days later. Again, a 4,100 difference.

Today I received my answer: It turns out that until now, the official state exchange enrollment reports were including both QHPs and Medicaid in both the "renewed" and "new" enrollment numbers. Medicaid/CHIP enrollments make up around 7,000 of the total (around 2,800 renewals and 4,300 new).

The broken-out numbers for Vermont, as of last night, directly from my contact at Vermont Health Connect, are as follows:

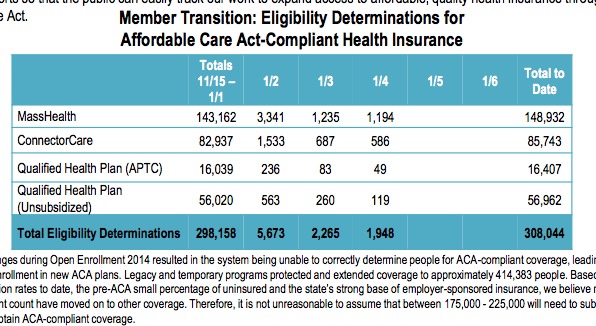

Chalk up another (likely) 2,000 QHPs for Massachusetts over the weekend: There were 4,116 QHP determinations from the 2nd - 4th (plus just a handful on New Year's Eve and Day for obvious reasons). Assuming at least 50% of them followed through and selected a plan (which has been pretty reliable so far), that should bring the grand total of QHP selections up to around 83.4K to date.

Meanwhile, Medicaid enrollments are closing in on 150K.

Earlier this evening I received the following email. I'm not including the sender's identifying information for obvious reasons:

Someone from this website contacted me to help with enrolling in health insurance. They created an account on healthcare.gov with an id of XXXXXXXX@acasignup.net instead of my email address and did not give me the password. I am trying to make some changes to my healthcare coverage and update my information.

I am very concerned with the safety of my information. I thought they were from the health insurance marketplace.

If you could change my id to my email and give me the password I would very much appreciate it.

If not I will assume you are an identity thief and contact the FBI.

New York state regulators say more than 225,000 people have newly enrolled in Affordable Care Act health insurance coverage heading into 2015.

That is important because more people with health insurance equals jobs,according to some investment advisers, who say hospitals and health care companies spend more money on construction and other related growth as the uninsured rate drops.

With the Affordable Care Act seemingly off to a good start in its first year, increasing access to insurance coverage for adults, attention is likely to turn to an older program for children that will come to an end in 2015 if it is not reauthorized: the Children’s Health Insurance Program, or CHIP.

OK, this is kind of strange...the WA exchange has not posted any press releases since the 23rd, and specifically told me that they don't have any updated numbers since then, but this brief story at KLEW TV is pretty clear about it...and the numbers are about right, since they only include 1 more day of data (the press release went through the 22nd, and the 23rd was the deadline for January coverage in WA):

LEWISTON, ID - We start off with news about healthcare. 101,000 people in Washington State have bought health insurance through the Washington Exchange so far during this open enrollment period.

About 76,000 renewed their policies by the Tuesday deadline for January first coverage. About 25,000 are new to the exchange and will have insurance on the first day of the new year.

The article also gives a solid number for how many current enrollees didn't make the deadline and what their options are:

Lost in the shuffle of the first monthly HHS report (which only ran through 12/15 and was missing gobs of data) was their weekly snapshot report, which was released the same day. It runs through 12/26, but isn't broken out by state, of course, and most importantly only includes QHP selections for the 37 states run through HC.gov.

I was expecting the number to drop substantially last week, of course, since the January coverage deadine has passed and the vast bulk of renewals (active + automatic) were already baked into the prior week's report. I figured that we'd be looking at roughly 30K/day on HC.gov until around January 10th, when it should start to spike again...or around 210K for the week.

Instead, I was surprised at how much it dropped last week--only 96,000 more QHPs added.

The Massachusetts exchange has released their weekly dashboard report, which includes actual QHP selections and payments, although that data only runs through 12/29.

Add them up and you get 79,842 total QHP selections, of which 55,260 have paid their first premium and are fully enrolled. This may sound like only a 69% payment rate, but remember that many of the remaining 24,582 aren't scheduled to have their current coverage dropped until the end of January and thus aren't even expecting their new policy to kick in until February 1st anyway. As always, the payments are a rolling average, and will ebb & flow until around mid-March (after which they should stabilize at around 88% at any given time).

For example, on Wednesday the 31st, the MA exchange issued a press release which stated that the total number who have paid in time for January 1st coverage is "over 50,000":

There hasn't been a lot of news about the upcoming King v. Burwell case lately, other than the fact that it's been scheduled to be heard by the Supreme Court on March 4th (with a final ruling likely to come out sometime in June).

One thing to watch as we approach the SCOTUS hearings on King v. Burwell this spring is how many people are newly qualifying for subsidies in those states as this year’s enrollment period continues.

The Department of Health and Human Services has released a new reporton enrollment data that suggests that number could be very large — which could (theoretically, at least) make it harder for SCOTUS to gut the law.

Remember, Rhode Island bumped out their January coverage deadline all the way through New Year's Eve, so even this data is still presumably missing a small surge on the final day:

HEALTHSOURCE RI RELEASES ENROLLMENT, DEMOGRAPHIC AND VOLUME DATA THROUGH DECEMBER 27, 2014

Posted on January 2, 2015 | By HealthSource RI

PROVIDENCE – HealthSource RI (HSRI) has released enrollment data, certain demographic data and certain volume metrics through Saturday, December 27, 2014, for Open Enrollment.

Enrollment data (November 7, 2014 through December 27, 2014)

As of December 27, 2014, 71% of Year One customers have renewed plans for 2015.*

Total New Customers: 4,969

Total Renewed Customers: 17,941

Total HealthSource RI enrollments for 2015 coverage

(including those who have not yet paid): 22,910

*As of December 30, 74% of Year One customers have renewed plans for 2015.

SHOP (cumulative as of December 27, 2014)

Small employer applications completed: 532

Small employer accounts created: 1,904 Small employer enrollment: 437 (representing 3,157 covered lives, based on their submitted census)

Small employers enrolling in Full Choice Model: 76%