The number of Americans struggling to pay medical bills fell last year for the first time in nearly a decade -- the latest sign that Obamacare is making health care more affordable.

Sixty-four million people, or approximately 35 percent of the U.S. population, said they had trouble paying bills or were stuck paying off medical debt in the past year, according to a new survey by the Commonwealth Fund released on Thursday. That was down from 75 million people, or 41 percent of the population, in 2012. This marks the first time that figure has fallen since 2005, when Commonwealth started keeping track.

Sean Parnell has posted a fairly negative story on the Rhode Island exchange, HealthSource RI. This is fairly unusual, because Rhode Island's exchange is actually one of the better ones...it operated fairly smoothly both last year and this year, and they're the only state which willingly followed the "no autorenewal" advice which I was giving to all of the exchanges way back in June (a few other states didn't allow autorenewals either, but that wasn't their choice...the new software platform wasn't compatible with the old software).

The problem in Rhode Island is that no matter how smooth and drama-free the exchange's operations have been, the actual numbers just haven't been up to snuff:

During the first eight weeks of open enrollment, 121,650 people enrolled in private coverage through Connect for Health Colorado and 47,724 in Medicaid and 2,272 in CHP+. Connect for Health Colorado also enrolled 20,580 individuals in dental plans.

“The enrollments in Medicaid and Connect for Health Colorado show that Coloradans are attuned to the importance of having health insurance coverage,” said Susan Birch, Executive Director of the Colorado Department of Health Care Policy and Financing. “Whether Coloradans have health insurance coverage through private insurance or through Medicaid, health coverage is the first step to better health.”

Colorado's last update ran through New Year's Eve, totalling 113,864 QHP enrollees, or 362 per day since the 12/15 deadline. That gives a nice apples-to-apples comparison to the new number (7,786 higher), which averages 519 per day...up over 40% per day since the holiday period.

As we’ve said many times before, it really pays for returning customers to the Obamacare insurance marketplaces to shop around for a 2015 health plan. Recent data from the federal government shows that a surprising number of people are doing just that.

More than 30 percent of federal marketplace customers who re-enrolled for 2015 did so by actively returning to Healthcare.gov and picking a plan, according to Health and Human Services Secretary Sylvia Mathews Burwell. That’s still less than half of all customers, but it far exceeds what you might expect based on consumer behavior in other public health insurancemarketplaces.

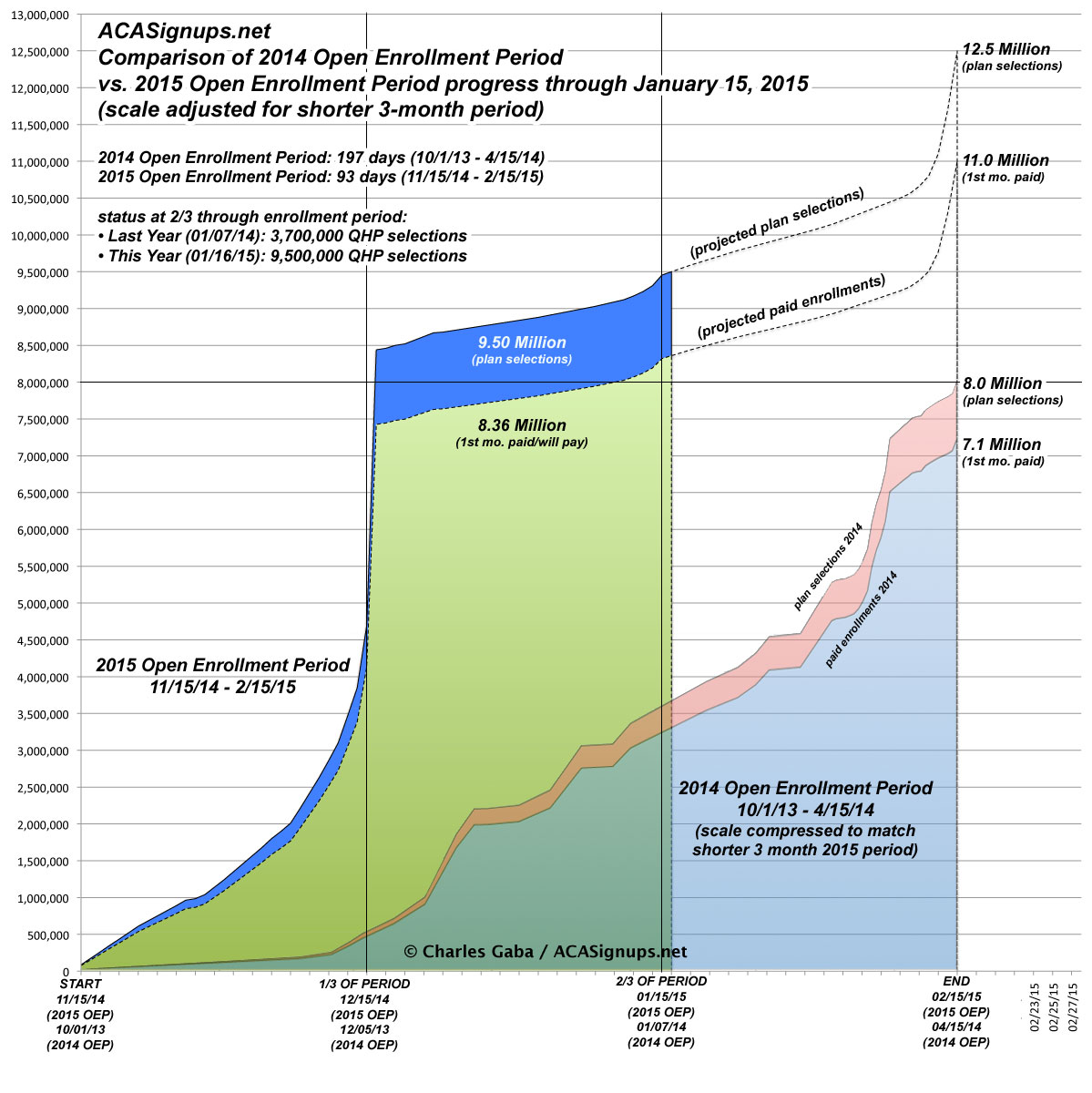

I put together a year-over-year overlay 1/3 of the way through open enrollment (right after the 12/15 deadline) and again at around the halfway point, both of which were pretty well-received, so now that we've crossed the 2/3 mark I've done an updated version.

I was going to use 1/15 as the cut-off date, but since the HHS "weekly snapshots" run through Fridays, I wanted to avoid the confusion of 2 different projection numbers, so I included the extra day to line this up with my 1/16 projection of 9.5 million QHPs even.

At the 2/3 point last year (around January 9th), total QHP selections were at around 3.7 million, versus the 9.5 million who should have enrolled for 2015 as of Friday night, or almost 2.6x as many. This gap will obviously close quickly once we move into the home stretch, but this period should still end with roughly a 50-60% increase over last year.

The following are, again, ACA/healthcare stories which I simply never had time to do write-ups on. Some of these are several weeks old, so please forgive any outdated-ness:

The Supreme Court on Monday rejected a 2-year-old legal challenge to a central provision of ObamaCare from a conservative doctors group.

The case, which was led by the Association of American Physicians and Surgeons, sought to strike down the law’s individual mandate, which fines individuals who fail to purchase health insurance.

The plaintiffs’ argument had been rejected twice before: first by a district court judge in 2012 and then by the D.C. Circuit Court of Appeals in March 2014.

As I reported Wednesday, brokers and small businesses using the D.C. Health Link exchange say the website is plagued with technical problems that have led to ongoing delays and frustrations. Among the problems: frozen screens, lost enrollment information, repeat error messages and other glitches. They also described ongoing delayed responses when they've reached out to the help resources for D.C. Health Link.

California's Obamacare exchange rejected a bid from the nation's largest health insurer to start selling coverage statewide next year.

The Covered California board adopted new rules Thursday that sharply limit where industry giant UnitedHealth Group Inc. could offer policies to individuals.

I haven't checked in on the Medicaid/CHIP enrollment situation in awhile, but with last week's revelation that California's Medicaid enrollment is a whopping 500,000 higher than previously thought, I probably should have done so earlier.

Well this one was unexpected: It's not a formal press release, but this story from the Hawaii Reporter--which actually has a pretty negative slant to it--is chock full of actual, current enrollment data points for Hawaii...and they're pretty good, relatively speaking.

None of the numbers are precise--they're all rounded off...but it's still a breath of fresh air from the Aloha state, and brings the number of states which haven't provided renewal data down from 3 to two (of course, the other two are California and New York, but still...)

...The Connector had about 1,000 people enrolled at this time last year. As of Thursday, that number had grown to 16,000.

...More than 365 small businesses, with 2,400 enrollees, have joined the Connector through the Small Business Health Options Program, or SHOP, in part because of tax deductions available to them, Kissel said.

So, that brings their total up to 91,430 as of...um...well, "the last week alone" suggests 7 days, which would mean either 1/07 - 1/13 or 1/09 - 1/15 (which would leave a 2-day gap). Fortunately, they then followed up with this:

Two months of open enrollment down & more than 125,000 Kentuckians have newly enrolled 4 health coverage or renewed their plans thru #kynect