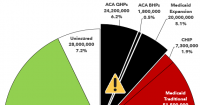

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

Back in March, the Health & Human Services (HHS) Dept. and the Centers for Medicare & Medicaid Services (CMS) proposed a so-called "Marketplace Integrity & Affordability Rule" which would include sweeping changes to how the ACA exchanges (both the federal one (HealthCare.Gov) and the 20-odd state-based ones (Covered California, MNsure, etc) operate, as well as who is or isn't eligible to enroll in ACA exchange coverage, restrictions on subsidy eligibility and so forth.

Many of these changes are simply repeals/reversals of improvements put into place during the Biden Administration; others are completely new ones being put into place by the Trump Regime under RFK Jr. & Dr. Oz.

However, until today, these were still technically only proposed changes. Now they're official. The final version isn't quite as bad as it could have been, and there's one or two items on the list which I'm not that upset about, but overall...yeah, it's pretty ugly.

16 Million Americans Would Become Uninsured Due to Reconciliation Bill and Loss of Tax Credits; 8.2 Million in Marketplaces Alone

Leaders from State-based Health Insurance Marketplaces, Enrollees, Providers, and Small Business Highlight Potential, Devastating Impacts

(Washington, DC) The Congressional Reconciliation bill and loss of federal tax credits would result in 16 million Americans losing health coverage, including 8.2 million enrolled in Health Insurance Marketplaces. By stripping millions of lives from the Marketplaces, health care will be more expensive, harder to access, create a strain on health care systems, and hurt small businesses.

Rep. Boyle: The one thing I would point out, though, is this bill is actually significantly worse [than the GOP's ACA repeal attempt in 2017], because this piece of legislation will throw 13.5 million, almost 14 million Americans off their healthcare.

First, you're cutting people off Medicaid. But second, this does include very deep cuts to Obamacare as well. And finally, I have breaking news for you tonight, that literally just came out in the last few minutes as I've been sitting here: The nonpartisan Congressional Budget Office, the official authority on these figures, has now confirmed that this bill, in addition to Medicaid cuts, in addition to Obamacare cuts, includes $500 BILLION WORTH OF CUTS TO MEDICARE that is now in this bill as well.

With potential Federal cuts to Medicaid on the horizon, renewing enhanced premium tax credits to ensure affordable insurance through the marketplace takes on greater significance

AUGUSTA— The Maine Department of Health and Human Services (DHHS) Office of the Health Insurance Marketplace (OHIM) today announced its support for renewing the enhanced premium tax credits for consumers of the health insurance marketplace.

The enhanced premium tax credits, which were first implemented in 2021 through the American Rescue Act and extended in the Inflation Reduction Act are set to expire at the end of this year unless Congress acts. Allowing these federal tax credits to expire will result in higher health insurance premiums for Maine consumers, potentially putting health coverage out of reach for thousands of Mainers. Overall, the enhanced tax credits are saving Mainers a conservative estimate of nearly $90 million in health care premium savings this year.

UPDATED 5/22/25: Welp. House Republicans did indeed follow through with passing their horrific (and disgustingly-titled) "One Big Beautiful Bill" Act which will effectively repeal the bulk of the ACA without officially repealing it, and that's just for starters.

The final vote was 215 - 214, with every Republican except a handful voting for it (and the two who voted against it openly admitted to the NY Times that they would have voted for it if their votes had been needed), and every Democrat voting against it. There were 2 Republican "no" votes...but both of those were only because they wanted the final bill to be even more draconian.

With all the understandable focus on Congressional Republicans efforts to effectively end Medicaid coverage for nearly 21 million Americans enrolled via ACA expansion, there's been much less attention paid to the other looming threat to healthcare coverage: The expiration of the upgraded financial subsidies for ~24.2 million ACA exchange enrollees, which are currently scheduled to end this New Year's Eve.

As I've explained numerous times before, the ACA's original premium subsidy formula was always far too stingy to make individual market policies affordable for many people...and worse yet, the subsidies cut off entirely for households making more than 4 times the Federal Poverty Level (FPL).

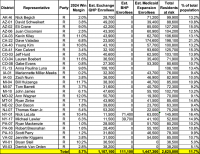

As you can imagine, this has been a monumental task; not only did I have to crunch a lot of data to break out the statewide numbers into House district-level estimates, I also had to convert that data into nearly 480 easy-to-read graphics...and then I doubled my workload by going one step further and adding high-res PDF versions for folks to print out in large format for town halls, rallies and #HandsOff protests nationally.

RE-UPPED 1/31/22: It was announced this morning that John James, who lost not one but two statewide U.S. Senate races back to back in 2018 & 2020, is taking a third swing at elected office in 2022. This time he's setting his sights lower, going for Michigan's new open 10th Congressional district, which is still competitive but which definitely has more of a GOP-tilt to it. In light of that, I decided to dust off this post again.

RE-UPPED 4/9/25: It was announced yesterday that John James, who finally made it into elected office as a U.S. Representative in Michigan's 10th Congressional District (only to essentially abandon his district the moment he got re-elected in 2024) is now running for statewide office again, this time for Governor. In light of that, I decided to dust off this post again (again).

A month ago, incumbent Democratic Senator Gary Peters of Michigan and his Republican challenger John James were both interviewed as part of a Detroit Regional Chamber series on several issues, including healthcare policy and the ACA.

This was actually announced a few weeks ago, but I was knee-deep in my Congressional District-level Enrollment Breakout Pie Chart project so I didn't get around to posting about it until now.

Today, the Centers for Medicare & Medicaid Services (CMS) released a proposed rule to address the troubling amount of improper enrollments impacting Affordable Care Act (ACA) Health Insurance Marketplaces across the country. CMS’ 2025 Marketplace Integrity and Affordability Proposed Rule includes proposals that take critical and necessary steps to protect people from being enrolled in Marketplace coverage without their knowledge or consent, promote stable and affordable health insurance markets, and ensure taxpayer dollars fund financial assistance only for the people the ACA set out to support.