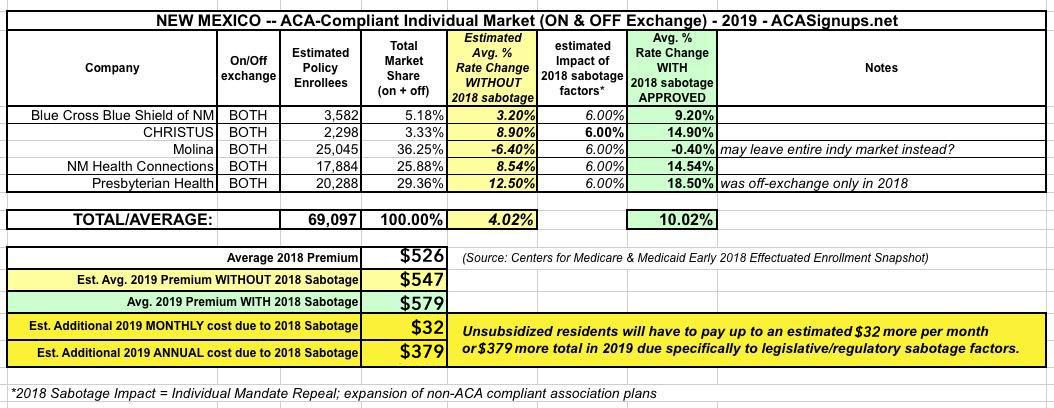

New Mexico was one of the earlier states to post their initial, requested 2019 ACA individual market premium hikes back in June. At the time, the five carriers asked for rate increases ranging from a slight drop (-0.4% for Molina) to as high as an 18.5% increase for Presbyterian Health, which is currently only offering off-exchange policies this year. Based on their preliminary filings, New Mexico was looking at a weighted average increase of around 10.0% next year, which would have been more like 4% if not for this years sabotage efforts by Trump and the GOP (mandate repeal & expansion of #ShortAssPlans):

A few weeks ago, I posted about New Jersey's preliminary 2019 ACA-compliant individual market rate filings. At the time, the official New Jersey Dept. of Banking & Insurance specifically stated that:

Normally at this point in the year I only do full rate hike write-ups for states when their approved rate changes are made public by insurance regulators. I'm making an exception for Texas, however, because my preliminary analysis of the statewide average premium changes back in June was missing a huge portion of the market--I only had around half the ACA individual market accounted for, and I repeatedly warned that the missing enrollment and rate change data could easily skew the statewide average higher or lower.

Well, it's early September now, and not only do I have access to pretty much all of the missing data now, some of the rate filings have changed significantly as well. At the time, I estimated Texas carriers as requesting average rate increases of just 1.5% overall, with them dropping around 10.6% if not for the ACA's individual mandate being repealed and Trump's expansion of #ShortAssPlans.

Back in April, I started an ambitious project which set out to track every legislative or regulatory measure taken by every state to counter, cancel out or mitigate sabotage of the Affordable Care Act by the Trump Administration and Congressional Republicans. It resulted in this color-coded spreadsheet, which lists dozens of bills, proposals, amendments and so on at various stages of completion.

The bad news is that project has proven to be too large for me to keep up with--there's simply too many bills, too many stages and too much other stuff going on for me to keep track of it all.

DOI Completes Review of Individual and Small-Group Health Insurance Rate Filings

The Kentucky Department of Insurance (DOI) announced today that it has completed its review of the individual and small-group insurance rates filed in the Kentucky market. The rates will be used to calculate insurance premiums in the 2019 benefit year.

Kentuckians in the individual market will once again experience changes in premiums and plan offerings. The rates that will be used reflect an average rate increase of 4.3 percent for Anthem Health Plans of Kentucky (Anthem) and 19.4 percent for CareSource. Since the actual premium charged will vary by individual and the plan level selected, some individuals may see a decrease in rates.

This just in from the Florida Office of Insurance Regulation...

OIR Announces 2019 PPACA Individual Market Health Insurance Plan Rates

TALLAHASSEE, Fla. – The Florida Office of Insurance Regulation (OIR) announced today that premiums for Florida individual major medical plans in compliance with the federal Patient Protection & Affordable Care Act (PPACA) will increase an average of 5.2 percent beginning January 1, 2019. Per federal guidelines, a total of nine health insurance companies submitted rate filings for OIR’s review in June with final rate determinations due by August 22, 2018.

Following OIR’s rate filing review, the average approved rate changes on the Exchange range from a low of -1.5 percent to a high of 9.8 percent. This information can be located in the Individual PPACA Market Monthly Premiums for Plan Year 2019 document available here.

With the deadline for submitting 2019 rate filings having passed a week or so ago, the approved rates from the various state insurance regulators have been popping up left and right. Today I took a look at the Arkansas Insurance Dept. website and sure enough, they've posted the approved filings for all 4 carriers on the individual market (as well as the small group market).

On the one hand, the statewide average rate increase hasn't changed much from the preliminary average; it dropped 0.4 points from 4.5% to 4.1%...and some of that change is simply because I had misestimated the actual enrollment/market share for a couple of the carriers.

On the other hand, in Arkansas, at least, it appears that the carriers don't think the repeal of the individual mandate and/or the Trump Administration's expansion of short-term and association health plans will have nearly as big of an adverse selection impact as other estimates/projections have...including my own.

Ensure that young adults can continue to remain on their parents’ health insurance plans until age 26

Prohibit insurers from using applicants’ gender to set premiums

Prohibit insurers from rejecting an application based on an applicant’s medical history, or imposing coverage exclusions based on pre-existing conditions.

Today, however, there were major developments regarding #ShortAssPlan restrictions (and a few other important patient protection bills) in three states: Two positive, one negative.