The ACA's language didn't account for the possibility that some states might not expand Medicaid, which is why the lower-end range of exchange plan subsidy eligibility starts off at 100% FPL...

Unfortunately, those earning less than 100% FPL are still stuck without any viable options besides either "going bare" and praying they don't get sick or injured or possibly buying a junk plan of some sort. According to the Kaiser Family Foundation, there's around 2.2 million Americans still caught in the "Medicaid Gap", where they don't qualify for Medicaid but don't earn enough to be eligible for subsidized ACA exchange policies (Kaiser estimates another 1.8 million uninsured adults in these states in the 100 - 138% "overlap" cateogory, plus around 356,000 who are eligible for Medicaid but still haven't enrolled for one reason or another).

NOTE: This is an updated version of a post from a couple of months ago. Since then, there's been a MASSIVELY important development: The passage of the American Rescue Plan, which includes a dramatic upgrade in ACA subsidies for not only the millions of people already receiving them, but for millions more who didn't previously qualify for financial assistance.

Much has been written by myself and others (especially the Kaiser Family Foundation) about the fact that millions of uninsured Americans are eligible for ZERO PREMIUM Bronze ACA healthcare policies.

I say "Zero Premium" instead of "Free" because there's still deductibles and co-pays involved, although all ACA plans also include a long list of free preventative services from physicals and blood screenings to mammograms and immunizations with no deductible or co-pay involved.

Missouri just voted #YesOn2 to expand Medicaid, and now, because of YOUR vote, over 230,000 hardworking people will have access to life-saving healthcare!pic.twitter.com/azHN0GJjEW

— YesOn2: Healthcare for Missouri (@YesOn2MO) August 5, 2020

Last summer, when activists in both Missouri and Oklahoma were preparing for this historic vote, I wrote the following:

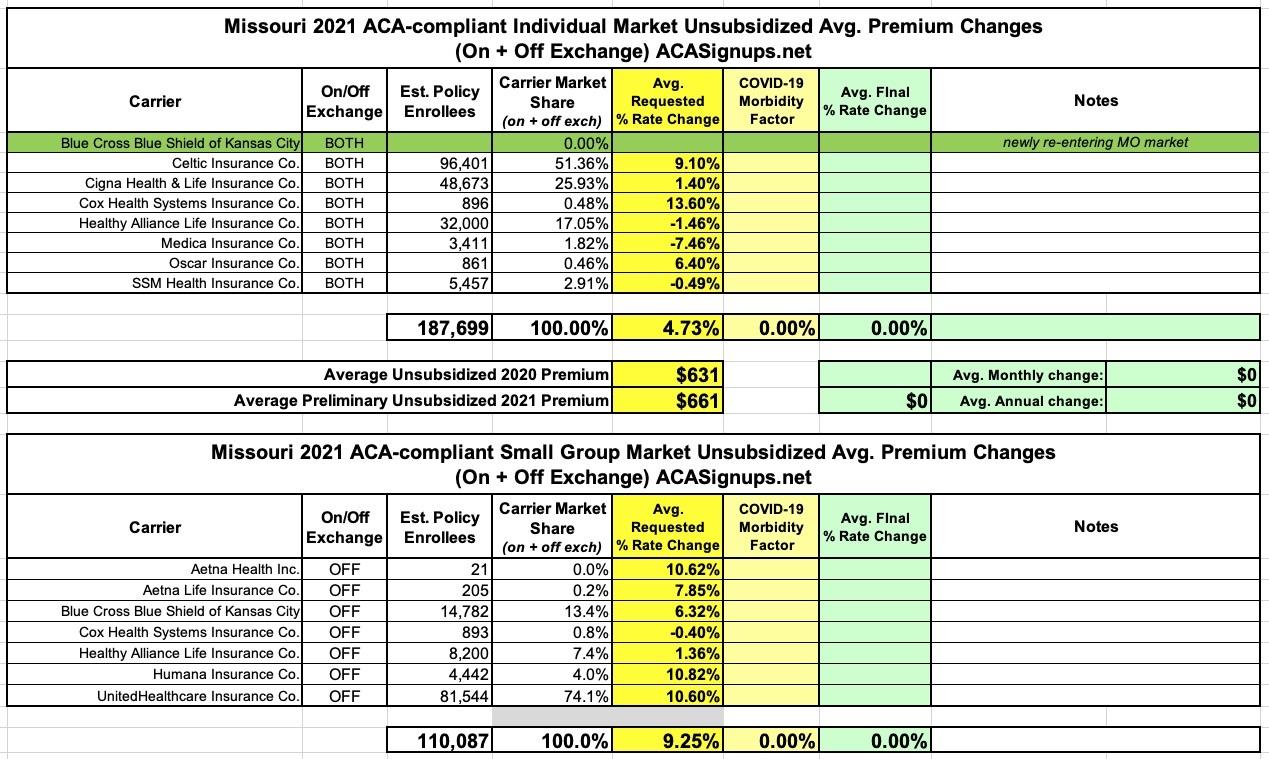

Missouri's preliminary avg. 2021 unsubsidized premium rate changes have been posted. There's one new entrant into the individual market this year (Blue Cross Blue Shield of Kansas City, which actually mostly pulled out of MO a couple of years back). Nothing too noteworthy--the average requested 2021 premium is going up 4.7% on the individual market and 9.3% on the small group market.

On Tuesday, August 4, all Missourians will have the chance to vote Yes On 2 to bring more than a billion of our tax dollars home from Washington every year – money that’s now going to places like California and New York instead.

By bringing our tax dollars home, we can protect thousands of frontline healthcare jobs, help keep rural hospitals open, and deliver healthcare to Missourians who earn less than $18,000 a year. That includes thousands of veterans and their families, those nearing retirement, working women who don’t have access to preventive care, and other hardworking Missourians whose jobs don’t provide health insurance.

When I first read the quote, I assumed it was either a paraphrase, out of context or sarcasm. Sadly, it was none of those:

A series of controversial remarks by Missouri Gov. Mike Parson on a St. Louis radio show are getting widespread attention — and some pushback.

In an interview on Friday with talk-radio host Marc Cox on KFTK (97.1 FM), Parson indicated both certainty and acceptance that the coronavirus will spread among children when they return to school this fall. The virus has killed 1,130 people in the state despite a weekslong stay-at-home order in the spring that helped slow the virus’ spread — and the state set a record on Saturday with 958 new cases.

...Parson’s comment on the coronavirus signaled that the decision to send all children back to school would be justified even in a scenario in which all of them became infected with the coronavirus.

Back in 2018, I was all over the trend of deep red states putting ACA Medicaid expansion on the ballot after getting fed up with years of their elected leaders refusing to do so. Idaho, Utah and Nebraska voters all did exactly that, passing it by solid margins. Unfortunately, state Republicans got in the way (or at least tried to) in all three states, adding hurdles, barriers and caveats which have either delayed or partly weakened them.

The recent elections in Virginia, Kentucky and Louisiana had two things in common: The first is that all three were huge victories for Democrats (they took control of both the state House and Senate in Virginia, flipped the Governor's seat in Kentucky and held onto it in deep red Louisiana).

The second is that all three elections were won in large part based on...Medicaid expansion.

Yet Edwards won, in large part, by also stressing his implementation of the Affordable Care Act’s Medicaid expansion in the state during his first term. Indeed, Edwards’s lead pollster, Zac McCrary, told me during an interview that no single issue was more important in driving the governor’s victory.

Missouri's final/approved avg. 2020 unsubsidized premium rate changes have finally been posted by CMS. For the most part they're following the same pattern as most other states this year with modest increases or decreases and a statewide weighted average decrease of 2.0% year over year. On average, unsubsidized ACA enrollees should pay about $13/month less next year than they are today.

However, what is noteworthy is that not one, not two but three new insurance carriers are entering the MO individual market this fall, bringing the total up to seven operating statewide: Cox Health Systems, Oscar Insurance (which was cofounded by Jared Kushner's brother, FWIW) and SSM Health Insurance.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions: