As I noted last night, thanks to the federal Rate Review website finally being updated to include the final, approved 2022 rates for both the individual and small group markets in all 50 states (+DC), I've been able to fill in the missing data for my annual ACA Rate Change Project.

As I note there, the overall weighted average looks like it'll be roughly +3.5% nationally.

Normally I write up a separate entry for both the preliminary and approved rate changes in each individual state, but it seems like overkill to create 14 separate entries at once. Besides, in many of these states there's been few if any changes between the preliminary and approved rate changes.

Cigna is joining the Mississippi exchange for 2022, bringing the total number of participating insurers to three. According to ratereview.gov, the following average rate changes have been proposed by Mississippi’s current exchange insurers:

I've once again relaunched my project from last fall to track Medicaid enrollment (both standard and expansion alike) on a monthly basis for every state dating back to the ACA being signed into law.

For the various enrollment data, I'm using data from Medicaid.gov's Medicaid Enrollment Data Collected Through MBES reports. Unfortunately, they've only published enrollment data through December 2020. In most states I've been able to get more recent enrollment data from state websites and other sources. For 2021 Mississippi data, I'm using estimates based on raw data from the Mississippi Division of Medicaid.

Mississippi is one of 12 states which still hasn't expanded Medicaid eligibility under the ACA (13 if you include Missouri, whose voters expanded the program last year...but which the state legislature refuses to fund).

Now that I've developed a standardized format/layout & methodology for tracking both state- and county-level COVID vaccination levels by partisan lean (which can also be easily applied to other variables like education level, median income, population density, ethnicity, etc), I've started moving beyond my home state of Michigan.

The ACA was originally designed with the intention that all documented Americans living in all 50 states (+DC) earning up to at least 138% of the Federal Poverty Level (FPL) would be eligible for Medicaid. Unfortunately, the 2012 NFIB v. Sebelius ruling by the U.S. Supreme Court stated that Medicaid expansion under the ACA had to be left up to each individual state.

This meant that each state had to decide, whether by legislation, executive order (depending on the state) or ballot initiative, whether or not to expand the low-income public health program or not. Under the ACA, any state which does so will have 90% of the cost paid for by the federal government, while the state has to pony up the other 10% of the cost.

Mississippi once again has two carriers offering ACA-compliant individual market coverage in 2021 and six on the small group market. Unfortunately, few filing forms don't seem to be available and the ones which are are redacted, so I can't run weighted averages for either.

The unweighted average rate increases are 2.7% on the individual market and basically flat for small group plans.

For the past two weeks, along with other noteworthy Open Enrollment data numbers, I've been scratching my head over what the deal is in Mississippi:

Once again, Maine remains the worst-performer year over year, mostly due to their expansion of Medicaid. Idaho isn't listed because they're a state-based exchange and haven't reported any data yet. Mississippi, on the other hand, continues to be the top out-performer vs. last year, which is interesting because there doesn't seem to be any particular reason for it.

Unlike some states, Mississippi hasn't implemented any additional subsidies, a mandate penalty or a reinsurance program of any sort. They haven't had any new carriers join the ACA market, nor have any of them left. I don't think either of the carriers on the exchange have significantly expanded their territory or changed their offerings that much either...in fact, average premiums are essentially flat year over year.

In other words, by all rights, Mississippi should be performing almost exactly as they did last year...but enrollments are up 15.5% to date. Huh.

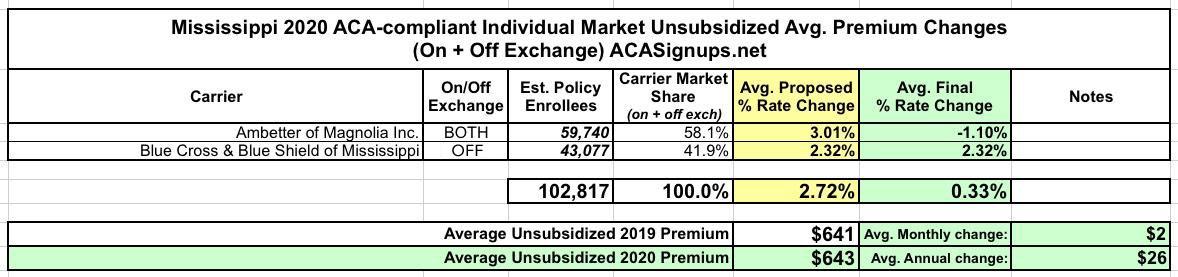

Mississippi once again has two carriers offering ACA-compliant individual market coverage in 2020: Ambetter of Magnolia, which holds 58% of the market, and Blue Cross Blue Shield with the other 42%. Earlier this year they were asking for average rate hikes of 3.0% and 2.3% respectively, but Ambetter's final/approved rates are coming in at a 1.1% reduction, bringing the overall average down to a mere 0.3% rate hike.

OK, my math here is gonna be a bit sloppy, but I'm just trying to illustrate a larger point about how splitting risk pools is, generally speaking, a Bad Thing.

Under the Affordable Care Act, non-ACA compliant healthcare policies were given until December 31st, 2013 to become fully ACA-compliant, including the new regulations mandating guaranteed issue, community rating, essential health benefits, no more annual or lifetime limits on coverage and so forth. All major medical policies offered from that day forward had to be fully ACA compliant (although there were some exceptions for short-term plans and so forth).

However, there was an exception made: Any existing policy which someone had been continuously enrolled in since before the ACA was signed into law by President Obama in March 2010 was considered to be "grandfathered" in. As long as the insurance carrier chose to keep offering those non-compliant policies, existing enrollees could remain enrolled, although premiums would of course increase from time to time. The "locked in" pool of enrollees would gradually dwindle as enrollees died, aged onto Medicare, got jobs with employer coverage and so on.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

{kind=link}