Last week I posted an exclusive story over at healthinsurance.org regarding attempts by the Minnesota Republican-held legislature to sneak in a nasty amendment which, had it passed and been signed into law, would have given insurance carriers the right to offer policies which cover, basically nothing whatsoever.

The story ended on a happy note a few days later, as the massive negative backlash caused the state GOP to yank the amendment from the bill in question just before it went to the final vote. Awesome!!

However, I never really explained exactly what bill the pulled amendment was attached to in the first place. I should have written up a full entry on this, but have been swamped all week due to the political insanity and rapidly-changing situation on everything, so here's the basics:

It's Back! Okay, folks, it's time to call your legislators, because the Drazkowski bill is back, and the GOP is giving it a full hearing TODAY!

This is the bill that would allow insurance companies to sell policies that do not cover chemotherapy, diabetes treatments, mental health services, maternity care, and many more benefits that are currently required to be covered by MN law.

The photo included is the Minnesota Statute 62Q, which is the statute that is being amended with this bill. These are the services that would be allowed to no longer be covered.

I've decided that for all future ACA enrollment data reports, I'm going to tack on "...on brink of possible ACA repeal" to the headline. Seems appropriate.

It's been quite awhile since I've written much of anything about the ACA's SHOP programs, which are the small business counterpart to the individual/family exchanges. The reason is pretty simple: SHOP enrollment is mostly a rounding error compared to either the ACA's Individual exchange enrollments or Medicaid expansion numbers.

SHOP enrollment (a mere 120K - 170K nationally, as far as I can tell) is even dwarfed by BHP program enrollment (around 700,000)...and that's only available in 2 states (Minnesota and New York). Heck, I don't even bother tracking them on my spreadsheets or graphs (I tried in 2014 but gave up on it the following year).

In Minnesota, assuming 116,000 people enroll in private exchange policies by the end of January, I estimate around 58,000 of them would be forced off of their private policy upon an immediate-effect full ACA repeal, plus another 234,000 enrolled in the ACA Medicaid expansion programand around 62,000 covered by their Basic Health Plan (BHP) program (aka MinnesotaCare) for a total of 354,000 residents kicked to the curb.

As for the individual market, my standard methodology applies:

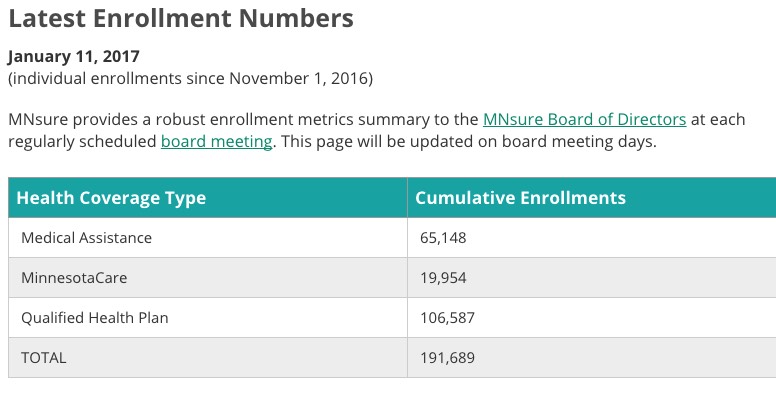

A few days ago I noted that MNsure, Minnesota's ACA exchange, has skyrocketed from last place to first in terms of achieving my personal OE4 enrollment targets, having enrolled 103,578 people in Qualified Health Plans (QHPs), plus another 19,960 in MinnesotaCare (MN's BHP program) and 65,164 in Medicaid.

Yestrerday they updated their numbers once again:

That's a further increase of 3,009 Minnesotans in QHPs in the past week or so. MN has already blown past my original projection (86K) and has reached 92% of my revised target (116K).

Minnesota is a different story. They started out Open Enrollment with a bang, racking up enrollees at up to 12x last year's pace...but that was mainly due to their unique "enrollment cap" policy this year. Once the caps were filled and current enrollees were all squared away, new enrollments appear to have dropped off dramatically. They're now dead last percent-of-target wise (again, I can't include NY or VT here since neither has enough data available).

This Just In...(Minnesota was one of the few states which stuck with the original 12/15 deadline for January coverage):

ST. PAUL, Minn.— MNsure has enrolled 54,586 Minnesotans in private health care coverage, far outpacing the approximately 27,000 who had enrolled at a similar stage of open enrollment last year.

Additionally, since the start of open enrollment, 14,020 Minnesotans have eligibility determinations in MinnesotaCare and 43,327 in Medical Assistance.

The 2015-2016 open enrollment period set a record for the most Minnesotans enrolled in private health plans, but the 2016-2017 period has been even more brisk. By December 28, 2015, the deadline for January 1 enrollment last year, about 27,000 had enrolled, meaning enrollment numbers are twice what they were at the same time last year.

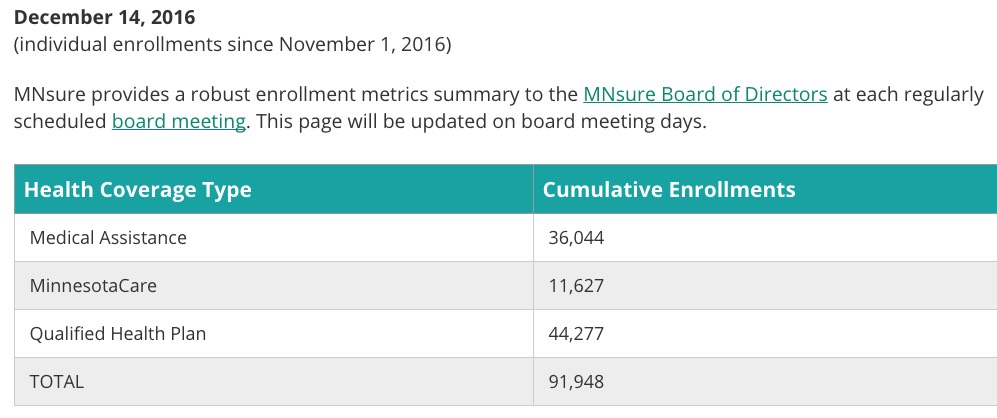

Just a couple of days ago, MNsure reported 41,882 QHP selections as of December 11th (there was some confusion about the date but I've since confirmed this).

Minnesota's "first-come-first-serve" enrollment cap system caused a massive surge in early QHP selections...so much so that they kicked things off by signing people up at a pace twelve times faster than last year in the first few days.

With more than four weeks of open enrollment in the books, more than 57 percent of Minnesotans enrolling in a private health insurance plan through MNsure are qualifying for financial help available only through the state-based health insurance marketplace. The average tax credit amount going to MNsure customers will be more than three times higher in 2017 than it was in 2016.