A week or so ago, I reported that Connect for Health Colorado's monthly enrollment report contained some very confusing numbers:

Last month I noted that, assuming I was reading Connect for Health Colorado's monthly dashboard report correctly, they were down to 115,890 effectuated exchange enrollees as of 3/31/16, or a whopping 23.1% lower than the official APTC report tally of 150,769 QHP selections as of the end of Open Enrollment.

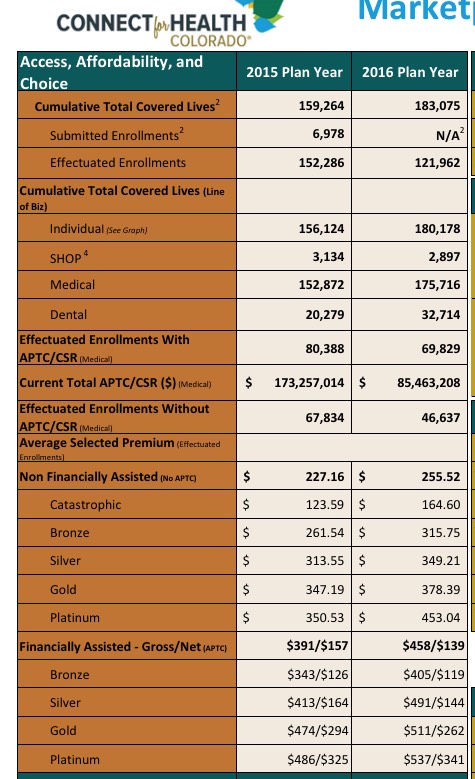

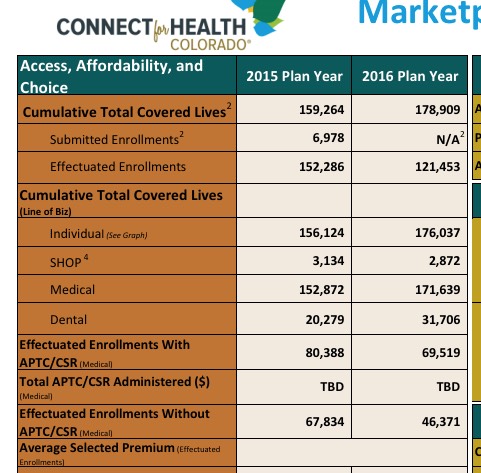

...The 121,962 number at the top seems to be the one I want...except that it also includes SHOP and standalone Dental enrollments (I think).

...OK, so 121,962 includes SHOP, which has a maximum tally of 2,897, which means that the effectuated number as of 4/30/16 could be as low as 119,065...except that "Individual" could also potentially include standalone dental plans, confusing the issue further. Even worse, it says that this "Includes those who effectuated in the current plan year and later terminated a policy".

I can't tell whether that means that those who terminated their policies have been subtracted from the total (accounted for) or if they're included in the total (cumulative).

Last month I noted that, assuming I was reading Connect for Health Colorado's monthly dashboard report correctly, they were down to 115,890 effectuated exchange enrollees as of 3/31/16, or a whopping 23.1% lower than the official APTC report tally of 150,769 QHP selections as of the end of Open Enrollment.

Over the weekend, they released their April dashboard report, and the numbers are actually up slightly...which means that while the net drop compared to the OE3 number is still steep, it's also spread out over a 3 month period instead of 2:

In a classic case of missing the forest for the trees, I posted two very wonky, detailed entries over the past couple of days about Minnesota and Connecticut's latest enrollment numbers...but completely missed one crucially important data point.

There's a bunch of different numbers there, but as far as I can tell, the one I'm looking for is "Effectuated Enrollments with APTC/CSR (medical)" combined with "Effectuated Enrollments Without APTC/CSR (medical)". That's 69,519 + 46,371 = 115,890 effectuated, individual, medical QHP enrollees as of 3/31/16.

Colorado lost their Co-Op...and CO is also one of only two states (Oregon is the other one) to drop their "transitional" policies as of the end of 2015. As a result, Colorado has a lot of people who could still potentially enroll by the end of February thanks to the 60-day Loss of Coverage Special Enrollment Period provision.

Louise Norris noted that there were around 39,000 ex-Co-Op members in Colorado (along with some others) who could still potentially enroll during February via the SEP option; I spitballed anywhere from 10,000 - 20,000 more Coloradoans might yet be added. There are also the normal SEPs for things like getting married, giving birth and so forth.

The last Colorado update, which ran through January 15th, had their numbers at 139,579 private policies (QHPs), 23,017 standalone dental plans, 45,100 in Medicaid and 2,771 in the SCHIP program.

I've just learned that Colorado's final tally as of the January 31st deadline stands at 153,583 QHPs, 25,604 dental, 54,447 Medicaid and 3,549 SCHIP, which means they added just over 14,000 in the final 16 days.

DENVER — Between Nov.1 and Jan. 15, more than 190,000 Coloradans enrolled in health coverage for 2016, either in private health insurance purchased through the state health insurance Marketplace or in Medicaid, or Child Health Plan Plus (CHP+), according to new data released today by Connect for Health Colorado® and the Colorado Department of Health Care Policy and Financing.

“These enrollment figures show strong growth during this open enrollment period,” said Connect for Health Colorado® CEO Kevin Patterson. “But we are now only days away from this year’s enrollment deadline for many. I strongly urge everyone who does not have health insurance provided through their employer to act right now to provide financial security for their families and to avoid a penalty that experts estimate will average nearly $1,000 per household. The final deadline for 2016 coverage for many Coloradans is Jan. 31.”

Connect for Health Colorado® and Colorado Medicaid Report Enrollment Gains of More Than 169,000

January 5, 2016

DENVER — Between Nov.1 and Dec. 31, more than 169,000 Coloradans enrolled in health coverage for 2016, either in private health insurance purchased through the state health insurance Marketplace or in Medicaid, or Child Health Plan Plus (CHP+), according to new data released today by Connect for Health Colorado® and the Colorado Department of Health Care Policy and Financing.

“We are very happy with the enrollment growth during the first two months of this open enrollment period,” said Connect for Health Colorado® CEO Kevin Patterson. “But I want to urge everyone who does not have health insurance provided through their employer to act now to provide financial security for their families and to avoid a penalty of nearly $695 or more. The final deadline for 2016 coverage –Jan. 31 – is fast approaching.”

DENVER (AP) – A new insurance-matching tool similar to Uber car sharing is helping Colorado’s health insurance exchange meet demand during the open enrollment period for people who need to sign up for health coverage , an exchange official said Thursday.

And an extended deadline didn’t hurt.

Open enrollment ends in January for Connect For Health Colorado. But Thursday was the deadline for shoppers to have coverage in effect by Jan. 1.

More than 117,000 people had signed up, though exact figures weren’t available, said Connect For Health spokesman Luke Clarke.

Connect for Health wants to see 217,000 people signed up by next summer. Clarke said the exchange is ahead of last year’s pace, when 113,000 had signed up by the December deadline.

The article doesn't specify what the "thru date" for the 117K figure is, but I'm assuming that it was as of 12/15 since that was the original deadline for January coverage and the story ran today.