With all the understandable focus on Congressional Republicans efforts to effectively end Medicaid coverage for nearly 21 million Americans enrolled via ACA expansion, there's been much less attention paid to the other looming threat to healthcare coverage: The expiration of the upgraded financial subsidies for ~24.2 million ACA exchange enrollees, which are currently scheduled to end this New Year's Eve.

As I've explained numerous times before, the ACA's original premium subsidy formula was always far too stingy to make individual market policies affordable for many people...and worse yet, the subsidies cut off entirely for households making more than 4 times the Federal Poverty Level (FPL).

CVS Plans To Exit Obamacare In 2026, Affecting 1 Million Aetna Members

CVS Health plans to exit the individual health insurance business also known as Obamacare next year, leaving about 1 million Aetna members in 17 states looking for new coverage in 2026.

...CVS’ move to exit the individual insurance market comes as the Donald Trump White House and Republicans in Congress ponder cuts to health insurance benefits to pay for tax cuts for wealthy Americans. Trump has never been a fan of Obamacare, which he tried and failed several times to repeal in his first term, and his administration has already made moves to cut spending on such health benefits, already slashing what the federal government spends on navigators that help people sign up for Obamacare coverage.

Meanwhile, it remains unclear whether subsidies Americans use to buy individual coverage will remain once Congress has passed its budget.

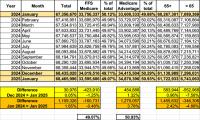

So far, after a 2-month initial delay, the Musk/Trump Regime has been posting updated Medicare enrollment data roughly once per month. We'll see if that continues.

Whether the data posted since January 20, 2025 is accurate or not, I can't say for certain, but at least they're updating it...and so far, at least, I don't see anything in their November 2024, December 2024 or January 2025 reports which is setting off any obvious red flags.

As of this writing, the same can't be said for the monthly Medicaid/CHIP enrollment reports, which are usually updated the same day as the Medicare reports, but which have remained stuck on October 2024 since before Trump was inaugurated in January.

In any event, according to the latest report, as of January 2025:

On March 30, 2023, a federal district court judge issued a sweeping ruling, enjoining the government from enforcing Affordable Care Act (ACA) requirements that health plans cover and waive cost-sharing for high-value preventive services. This decision, which wipes out the guarantee of benefits that Americans have taken for granted for 13 years, now takes immediate effect.

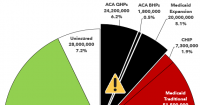

As you can imagine, this has been a monumental task; not only did I have to crunch a lot of data to break out the statewide numbers into House district-level estimates, I also had to convert that data into nearly 480 easy-to-read graphics...and then I doubled my workload by going one step further and adding high-res PDF versions for folks to print out in large format for town halls, rallies and #HandsOff protests nationally.

On Monday, Gov. Dan McKee said his team has identified 650,000 people whose personal information was stolen in the recent cyberattack on the state’s IT system for social services.

...Earlier this month, the cyberattack shut down the state’s IT system known as RIBridges, which serves as an eligibility database for a host of social services, such as SNAP and Medicaid, along with subsidized health insurance through HealthSourceRI.

...According to McKee, the state aims to turn the system back on in January. In the meantime, R.I. Human Services Director Kim Merolla-Brito said people will still receive benefits through SNAP, Medicaid and other cash-assistance programs. She said EBT cards should be refilled for January under normal distribution methods.

She added that nobody will be terminated from Medicaid while the system is down.

Every year around this time I start my annual individual & small group market rate filing analysis project. This involves spending months painstakingly tracking every insurance carrier rate filing for the upcoming year to determine just how much average insurance policy premiums on the individual market are projected to change.

Carriers tendency to jump in and out of the market, repeatedly revise their requests, and the confusing blizzard of actual filing forms sometimes make it next to impossible to find the specific data I need.

The actual data I need to compile my estimates are actually fairly simple, however. I really only need three pieces of information for each carrier: How many effectuated enrollees they have in ACA-compliant policies this year; the average projected rate change for those policies; and, ideally, a breakout of the rationale behind the changes.

Usually the reasons given are fairly vague things like "increased morbidity" (ie, a sicker risk pool) or the like. Sometimes, however, there's a very specific reason given for some or all of the premium changes. Major examples of this include:

As of today, 650,000 North Carolinians have access to affordable health care thanks to Medicaid expansion! When leaders come together across political differences, we can make people’s lives better.

Now we must come together to defend this bipartisan victory from proposed federal cuts. People’s health and our health care system depend on it.

Governor Josh Stein announced that as of today, 650,000 newly eligible North Carolinians have gained access to affordable health care through Medicaid expansion, including veterans and workers in child care, construction, hospitality, home health care and other industries essential to the state.

I thought I had finally wrapped up my ambitious Congressional district-by-district healthcare program enrollment pie chart project (for all 435 districts...actually 436 w/DC included). I knew I'd still have to update the numbers every few months, but at least the dust had finally settled on the layout and what info I'd include on each graphic.

RE-UPPED 1/31/22: It was announced this morning that John James, who lost not one but two statewide U.S. Senate races back to back in 2018 & 2020, is taking a third swing at elected office in 2022. This time he's setting his sights lower, going for Michigan's new open 10th Congressional district, which is still competitive but which definitely has more of a GOP-tilt to it. In light of that, I decided to dust off this post again.

RE-UPPED 4/9/25: It was announced yesterday that John James, who finally made it into elected office as a U.S. Representative in Michigan's 10th Congressional District (only to essentially abandon his district the moment he got re-elected in 2024) is now running for statewide office again, this time for Governor. In light of that, I decided to dust off this post again (again).

A month ago, incumbent Democratic Senator Gary Peters of Michigan and his Republican challenger John James were both interviewed as part of a Detroit Regional Chamber series on several issues, including healthcare policy and the ACA.