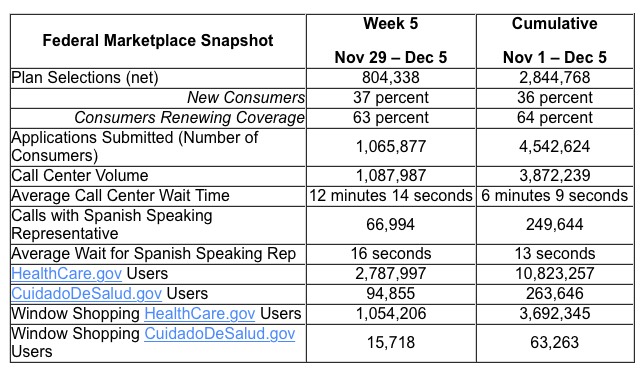

As expected, the December Surge started in Week 5, and should really be taking off even as I type this on Wednesday of Week 6. I overshot a bit this time:

Week 5 Projection: 840K / Actual: 804K (over by 4.4%)

Cumulative Projection: 2.88M / Actual: 2.84M (over by 1.2%)

I'm sticking to my guns for Week 6, projecting an even 1.5 million QHP selections via HealthCare.Gov, bringing the grand total to 4.34 million as of 12/12.

REMEMBER, as always, that this only includes the 38 states included on the federal exchange; when you throw in the other 13 running their own exchanges, the grand total by the 12th should be roughly 5.76 million QHPs nationally.

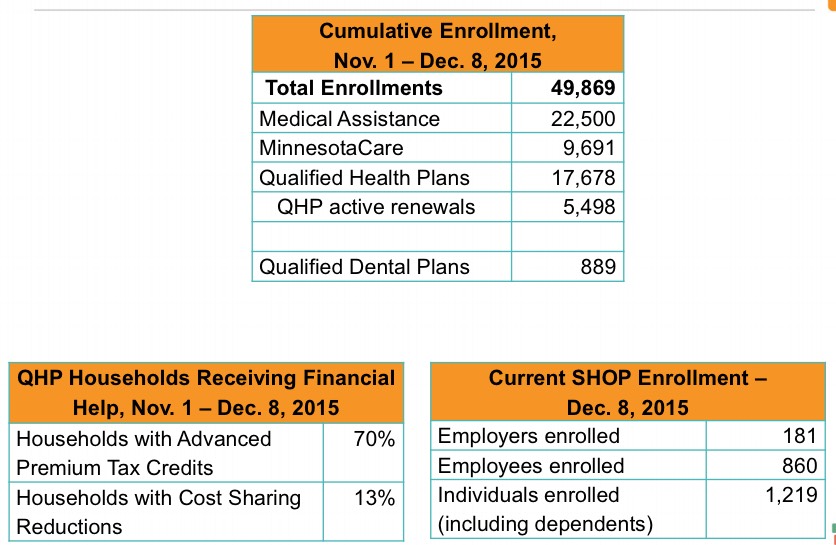

Thanks to Louise Norris for the heads up! MNsure held their monthly board meeting today as well, bringing their data right up to date through yesterday:

I launched the "State by State" chart feature towards the end of the 2015 Open Enrollment period last time around, and it proved to be pretty popular, so I've brought it back this year.

It's important to note that I'm still missing data from some state exchanges; I have bupkis from DC, Idaho, Kentucky, New York and Vermont. I also only have partial data from others (California includes new enrollees only, while several other states only have data for the first couple of weeks).

In addition, there are three states (Connecticut, Rhode Island and Washington State) where I have the opposite situation--they've front-loaded their autorenewals of current enrollees, with the understanding that those folks can still drop their coverage or switch to a different policy between now and December 15th (CT) or December 23rd (RI & WA).

As I note every week, between Rhode Island's tiny population, tinier ACA exchange numbers and especially their decision to "front-load" autorenewals of all current enrollees ahead of the 12/23 deadline for January coverage, their official QHP selection tally is only going up a few hundred per week. Week Five is no diffferent:

INDIVIDUAL AND FAMILY ENROLLMENT As of December 5, 2015:

31,500 individuals are enrolled in 2016 coverage through HSRI, paid and unpaid.

Nearly all of these individuals are current HSRI enrollees that have been auto-renewed into a 2016 plan.

1,592 individuals have selected a plan for 2016 coverage, and are new to HSRI this year or returning after being enrolled with HSRI at some point during a prior year.

I have a doctor's appointment myself this afternoon which I have to leave for soon (irony!!), so the second half of my weekly analysis (state level) will have to wait until I get back, but here's the major story.

With the December 15th deadline just 1 week away and the December Surge starting to kick in, CMS decided to hold a full press conference call this morning ahead of the Week 5 HC.gov Snapshot report.

UPDATE 12/03/15: OK, strike that. This has been nagging at me all day. I'm bumping my HC.gov Week Five projection up further to 840,000 for 11/29 - 12/05 (2.88 million cumulatively), or around 3.77 million nationally.

Washington Healthplanfinder Sees 123,000 Select Qualified Health Plans in First Month of Open Enrollment

The Washington Health Benefit Exchange today announced that more than 123,000 residents have selected Qualified Health Plans for 2016 coverage since the launch of the third open enrollment period on Nov. 1. Approximately 112,000 customers renewed plan selections from the previous year, with automatic renewals accounting for more than 84,000 of the 123,209 plans selected through December 1.

All residents who qualify must select a Qualified Health Plan throughwahealthplanfinder.org by December 23 to receive coverage by Jan. 1, 2016. Data collected from the first two open enrollment periods indicate a significant increase in sign-ups as the Dec. 23 deadline approaches. Open enrollment runs through Jan. 31, 2016.

Here's what Democratic Kentucky Governor Steve Beshear's official "Healthier Kentucky" webpage looked like yesterday. Outdated, of course (no updates since the end of the 2015 Open Enrollment Period), but lots of data touting the thousands and thousands of people the Affordable Care Act (aka OBAMACARE, guys) has helped receive healthcare coverage via either private policies or Medicaid expansion:

One more tidbit regarding the debate over how many people are "gaming the system" by abusing the Special Enrollment Periods allowing off-season exchange enrollment: Last spring, after the official Open Enrollment Period (along with the week-long "overtime" period tacked on for people "in line by midnight") ended, the HHS Dept., along with almost all of the state-based exchanges, decided to allow a 6-week "Tax Filing Season" special enrollment period. The idea was that this was the first year that people who hadn't gotten covered with ACA-compliant healthcare coverage the previous year would be hit with a tax penalty ($95 or 1% of their household income), and that as such, it was a bit unfair to dump that on those who truly "had no idea" that there was any sort of financial penalty for not doing so.

As I noted a few weeks ago, Covered California has an annoying policy (they did this last year as well) of not publicizing how many current QHP enrollees have renewed their policies (or switched to a different exchange-based one) until well after the December deadline has passed.

As of Monday, Dec. 7, more than 83,000 Californians had selected plans through Covered California since open enrollment began on Nov. 1.

“Thousands of people are signing up every day for Covered California, and we’re off to a good start to meet our forecasted enrollment of 295,000 to 450,000 new enrollees during this third open-enrollment period,” Lee said.