The survey also finds a lack of awareness about new rules for coverage introduced by the ACA. Among all those with ACA-compliant coverage, fewer than half (47 percent) know that preventive services are covered completely by their plans, while a third (33 percent) think that copays or deductibles apply to preventive services and one in five (20 percent) are not sure. Among those in high-deductible plans, awareness is even lower: 41 know that preventive services are covered with no cost-sharing.

The Kaiser Family Foundation has just released their 3rd Annual survey of people enrolled in the "Non-Group Health Insurance Market", otherwise known as the Individual market. It's important to note that this survey includes Americans enrolled in all individual market plans, both on and off-exchange. There are technically 5 separate categories, although they can effectively be merged into three categories for most purposes:

1. EXCHANGE-based QHPs (Qualified Health Plans)

2a. OFF-Exchange QHPs

2b. OFF-Exchange ACA-compliant non-QHPs

3a. OFF-Exchange NON-ACA compliant "Grandfathered" plans (ie, enrolled in prior to 2010)

3b. OFF-Exchange NON-ACA compliant "Transitional" or "Grandmothered" plans (ie, enrolled in between 2010 and 2013)

I tend to merge #2 & 3 together (off-exchange, ACA-compliant) in virtually all cases, and merge #4 & 5 together (grandfathered/grandmothered) except in cases where I need to make a distinction.

A source who doesn't wish to be named attended the annual meeting of the Wisconsin Common Ground Co-Op the other day (Common Ground is one of the 11 Co-Ops which survived last year's Risk Corridor Massacre), and forwarded a few tidbits of info:

CG is open to considering outside investment funding now that CMS is allowing the Co-Ops to pursue it, but isn't scrambling to seek it out just yet. They did note that Wisconsin has a law applying to the Co-Op which requires that all board members use it for their own insurance (which makes total sense, actually). Since any outside investor would likely be on the board, they'd also have to utilize CG coverage.

I was also provided with an image of their overall financials for 2015 (see below). They didn't have much to say about this year since it's only May but seemed comfortable with how things are proceeding so far, and said their MLR (medical loss ratio) is "dropping" although from what to what I have no idea.

UnitedHealth Group is pulling out of New Jersey’s Obamacare marketplace in 2017.

The company’s subsidiary, Oxford Health Plans, will stop offering individual plans on the state’s federally facilitated health insurance marketplace, according to a letter from the state Department of Banking and Insurance.

The letter was obtained by POLITICO through an Open Public Records Act request and the company later confirmed it will not offer exchange plans next year.

“Individuals impacted by these decisions will continue to have access to their current health benefits until the end of 2016, when they will need to pick new plans for 2017. Our small and large group business, Medicare and Medicaid businesses will not be impacted by this decision,” the company said in an emailed statement.

The good news is that it's easy to use, and lists all of the carrier rate hike requests in a clearcut manner...except, oddly, for CHRISTUS, which I'm pretty sure is being offered this year.

The bad news is that it doesn't include any of the actual market share/enrollment numbers, making it impossible to come up with a weighted average. Some of these are available via redacted filings over at the federal RateReview.Healthcare.Gov site, but not all of them. I have New Mexico Health Connections estimated at 48,000 based on this report, but I have no idea how many CHRISTUS or Presbyterian enrollees there are.

The RateReview site lists CHRISTUS as ranging from 9.4 - 15.2%, but without market share numbers I can't even come up with a proper rate hike request, so I've split the difference for now at 12.3%.

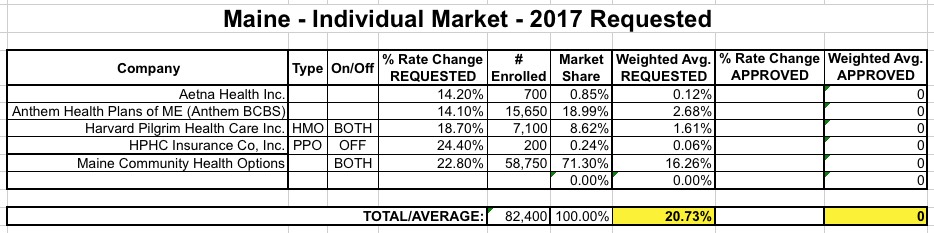

Well, now...this is about as cut & dry as it gets! They don't display the actual enrollment numbers for each carrier, but that's OK because the only real reason I need it in the first place is to weight the increases by market share...which the New York Dept. of Financial Services has helpfully already done!

And there you have it: A weighted average requested rate increase of 17.3% across the entire state's ACA-compliant individual market. Remember that NY never allowed transitional plans anyway, and there are likely only a handful of grandfathered plans left on the individual market, so this should cover well over 90% of the market.

They also included the Small Group market, which I take note of when available but don't really track nearly as closely as the indy market:

Many single payer advocates have been either confused or angry with me (to put it mildly) for not being a fan of Bernie Sanders's proposed national SP plan.

I've explained repeatedly that while I am a SP proponent, I just don't see it happening at the national level all at once. There are too many barricades and too many logistical, economic and political problems in doing so to make it remotely feasible to bring SP to the country in this fashion. In addition, I have major problems with the utter lack of detail in Bernie's plan.

HOWEVER, I've also repeatedly stated that I do strongly support getting the ball rolling at a smaller level first--either by partially expanding existing SP programs such as (Medicare, Medicaid, CHIP); consolidating existing private systems into larger risk pools (ie, merging the risk pools of the individual & small group markets, as a few states have done already); and/or by getting SP enacted at the state level, then using that as a model for other states and/or as a national model if it works out.

Name: Zahir

Organization: We want to write for acasignups.net

Hi there,

This is Zahir from a Hair Transplant company, we would like to provide you some high quality uniquely written articles and tips on Hair loss related issues at free of cost. The article will be nowhere posted; it will be dedicated for your website only.

Should we provide you our 1st article so that you can take a look?

For 2017, UnitedHealthcare, along with most of its subsidiaries, is discontinuing its participation in the individual market in Colorado, both on and off the exchange. However, Golden Rule Insurance, a subsidiary of UnitedHealthcare, will continue to offer its individual plans in Colorado off of the exchange. UnitedHealthcare will also continue its small and large group business in the state.

Humana will continue in the small group market for 2017 off the exchange, while exiting the individual market for both Humana Health Plans and Humana Insurance Company.