NATIONAL COALITION LAUNCHES “GET COVERED 2021” URGING AMERICA TO MASK UP AND GET INSURED – FOCUS ON COVID AND COVERAGE FOR 16 MILLION AMERICANS ELIGIBLE FOR FINANCIAL HELP NOW

“Get Covered” is a call to wear a mask to prevent the spread of COVID as well as a public statement that you want your family and friends to get health insurance.

COVID underscores why insurance matters - but not just because of the pandemic - coverage can help people stay healthy and provide a pathway to care for diseases like cancer, diabetes, and many others that impact people’s lives.

Get Covered 2021 will focus on getting the estimated 16 million uninsured people across America eligible for financial help – through their Affordable Care Act marketplace, or free coverage through Medicaid – insurance coverage now.

The Get Covered 2021 coalition announced that December 10th will be Get Covered America Day -- a day of action where everyone will be encouraged to keep wearing their mask and post a picture of themselves on social media, including a personal message about how friends, family and neighbors can get financial help for insurance now, sharing the website GetCovered2021.org and using the hashtag #GetCovered2021.

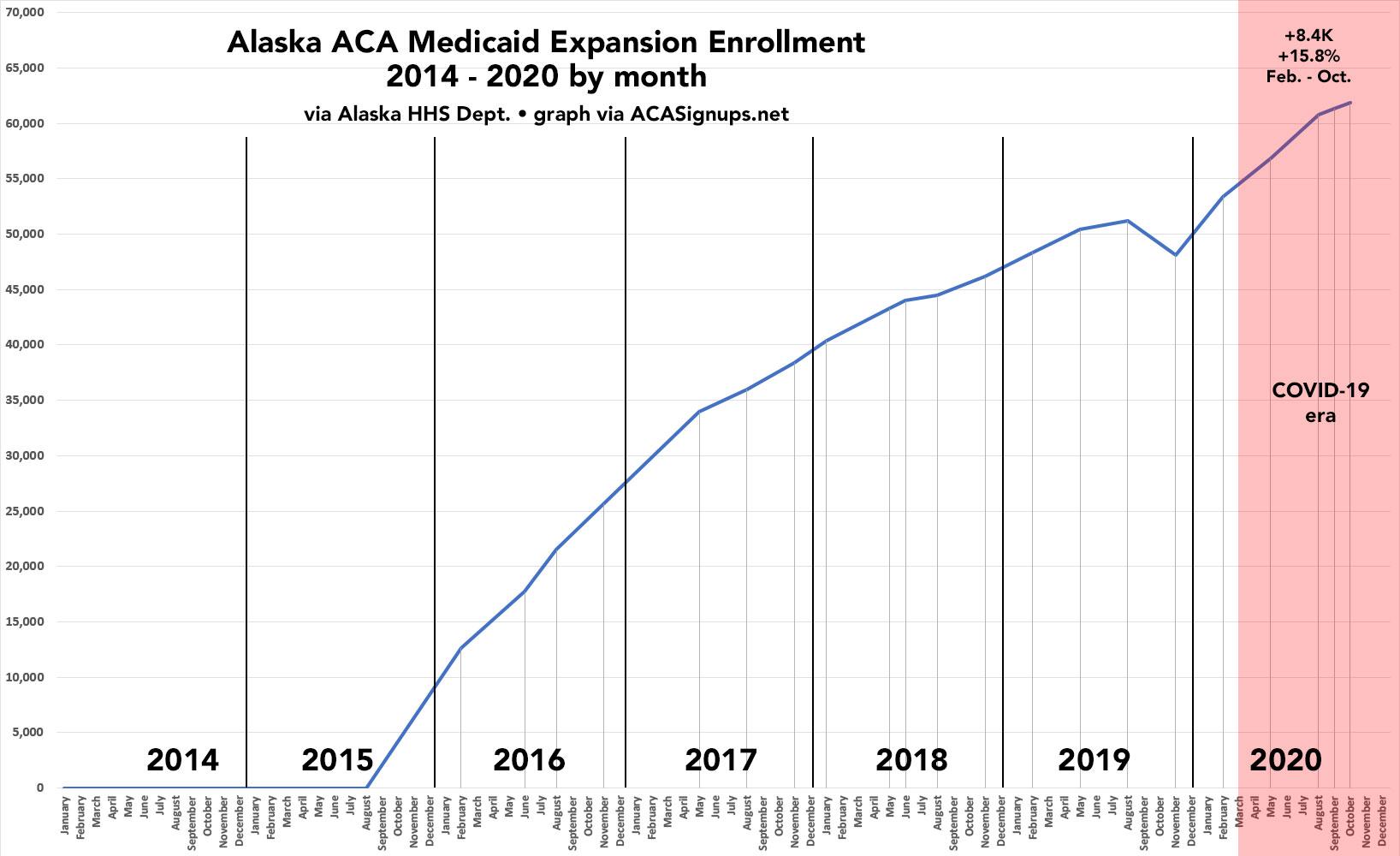

Over at Xpostfactoid, my colleague Andrew Sprung has been doing a great job of tracking ACA Medicaid expansion enrollment growth since the onset of the COVID-19 pandemic this past February/March at the macro (national) level, by looking at around a dozen states which have monthly reports available. He puts the overall enrollment growth rate at 23.6% from February thorugh October 2020.

I've decided to take a closer look at individual states. The graph below shows how many Arizonans have been actively enrolled their Medicaid expansion program (awkward named the Arizona Health Care Cost Containment System, or AHCCCS):

As I've noted several times before, two more states have split off from the federal ACA health insurance exchange (HealthCare.Gov) this year. New Jersey and Pennsylvania have joined twelve other states (and DC) in operating their own full ACA enrollment platform.

Over at Xpostfactoid, my colleague Andrew Sprung has been doing a great job of tracking ACA Medicaid expansion enrollment growth since the onset of the COVID-19 pandemic this past February/March at the macro (national) level, by looking at around a dozen states which have monthly reports available. He puts the overall enrollment growth rate at 23.6% from February thorugh October 2020.

Instead of replicating his work, I decided to take a closer look at individual states. The graph below shows how many Alaskans have been actively enrolled in our Medicaid expansion program (Healthy Michigan) every month since it was launched in September 2015:

ST. PAUL, Minn.—Since the start of MNsure's open enrollment period on November 1, nearly 102,000 Minnesotans have signed up for 2021 private health insurance coverage – approximately 10% more than this time last year.

MNsure's open enrollment period runs until December 22, 2020, a week longer than the federal open enrollment period.

“Every Minnesotan should have the peace of mind that comes with knowing you've got comprehensive health coverage, especially during the COVID-19 pandemic,” said MNsure CEO Nate Clark. “You can sign up through MNsure.org through December 22 for coverage beginning January 1, 2021. Don’t delay. Contact a MNsure-certified assister who can walk you through the enrollment process.”

Over at Xpostfactoid, my colleague Andrew Sprung has been doing a great job of tracking ACA Medicaid expansion enrollment growth since the onset of the COVID-19 pandemic this past February/March at the macro (national) level, by looking at around a dozen states which have monthly reports available. He puts the overall enrollment growth rate at 23.6% from February thorugh October 2020.

Instead of replicating his work, I decided to take a closer look at individual states, starting with my own: Michigan. The graph below shows how many Michiganders have been actively enrolled in our Medicaid expansion program (Healthy Michigan) every month since it was launched in April 2014 (we had a 3-month delay in the program due to the state legislature refusing to implement the new law with immediate effect; I have no idea why):

Health Insurance Coverage is More Important Than Ever – In Person Help Still Available during New Statewide Restrictions

The 2021 open enrollment period is underway, and Washingtonians are now signing up for health plans, including in new Cascade Care health plans. After months of a global pandemic – needs have changed due to job loss, or working from home, or family income changes. Individuals seeking health coverage can now shop more options this year, along with financial assistance, by visiting Washington Healthplanfinder to sign up for health and dental coverage.

“With infection rates climbing and economic uncertainty across Washington state, now is the time to sign up for health coverage,” said Chief Executive Officer Pam MacEwan. “There are many resources available to help individuals understand their options.”

It’s still 2020, so it only seems appropriate that we all have a lot on our plates. Despite the Texas v. California court case causing some news as it went before the Supreme Court this week, we continue to stay focused on our current Open Enrollment Period.

It is of note this year that individuals making up to $51,040 per year or a household of four making up to $104,800 annually may be eligible for financial help to lower their monthly premiums, healthcare discounts, or both. Nearly three quarters of all Connect for Health Colorado enrollments are financially assisted.

And, since plans and prices change every year, you can point people to our Quick Cost and Plan Finder Tool to see their options.

LANSING – Emergency orders Gov. Gretchen Whitmer has issued under the Emergency Powers of Governor Act are struck down, effective immediately, the Michigan Supreme Court said Monday in a 4-3 order that added an exclamation mark to an Oct. 2 ruling.

...Monday's Supreme Court ruling is in response to a lawsuit brought by the Michigan Legislature. The Oct. 2 ruling, which was a 4-3 decision striking down the Emergency Powers of Governor Act of 1945, was in response to questions sent to the court by a federal judge handling a lawsuit brought by medical service providers in western Michigan.

Monday's ruling means hundreds of thousands of Michiganders could lose their unemployment benefits "in a matter of days," Whitmer spokeswoman Tiffany Brown said. Among the orders struck down, and not replaced by a health department order, is one that extended Michigan unemployment benefits to 26 weeks, up from 20.

House Speaker Lee Chatfield, R-Levering, hailed the ruling.

The data below comes from the GitHub data repositories of Johns Hopkins University, except for Utah, which come from the GitHub data of the New York Times due to JHU not breaking the state out by county but by "region" for some reason.

Note that a few weeks ago I finally went through and separated out swing districts. I'm defining these as any county which where the difference between Donald Trump and Hillary Clinton was less than 6 percentage points either way in 2016. There's a total of 198 Swing Counties using this criteria (out of over 3,200 total), containing around 38.5 million Americans out of over 330 million nationally, or roughly 11.6% of the U.S. population.

With these updates in mind, here's the top 100 counties ranked by per capita COVID-19 cases as of Saturday, November 14th (click image for high-res version). Blue = Hillary Clinton won by more than 6 points; Orange = Donald Trump won by more than 6 points; Yellow = Swing District