I've mused before about how Avik Roy has a tendency to write lengthy screeds which breathlessly report developments which seem, to him, to be shocking revelations which will no doubt blow the lid off of some sort of nefarious actions on the part of President Obama, the HHS Dept. or Democrats in general...but which, when looked at by a rational person, tend to be fairly innocuous developments which were either already known, patently obvious and/or pretty much non-events in the scheme of things.

For instance, check out this blockbuster from back in March, regarding the HHS Dept's contingency plan in the event that the Obama administration had lost the King v. Burwell case at the Supreme Court (spoiler: they ended up winning):

If you ask most people what the earliest utterly absurd plot point in the original Star Wars movie ("A New Hope", 1977) was, they'd probably say the part about 7 minutes in where Gunnery Captain Bolvan tells Lieutenant Hija (yeah, I looked up their names) to "hold his fire" and not to bother shooting down the escape pod containing R2-D2 and C-3PO, because there were "no life forms onboard" (an odd thing to say in a universe filled with sentient robots...not to mention that Leia could have simply stowed the records on a hard drive or whatever and tossed it into the escape pod by itself for future recovery, but whatever).

Just 2 days ago I posted an analysis of the New York individual market rate increase requests for 2016. My takeaway was that the weighted average requested was 10.0%, with the usual caveats about rounding errors, estimates of the total individual market size and so forth. Plus, of course, these were just requested increases, not final ones.

NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES ANNOUNCES 2016 HEALTH INSURANCE PREMIUM RATES, INCLUDING RATES FOR NY STATE OF HEALTH

Individual Rates for 2016 Remain Nearly 50% Lower than Before Establishment of New York’s Health Exchange

DFS Rate Reduction Actions Will Save Consumers More than $430 million

New Essential Plan Will Lower Premiums to $20 or Less and Provide Better Benefits for Lower-income New Yorkers

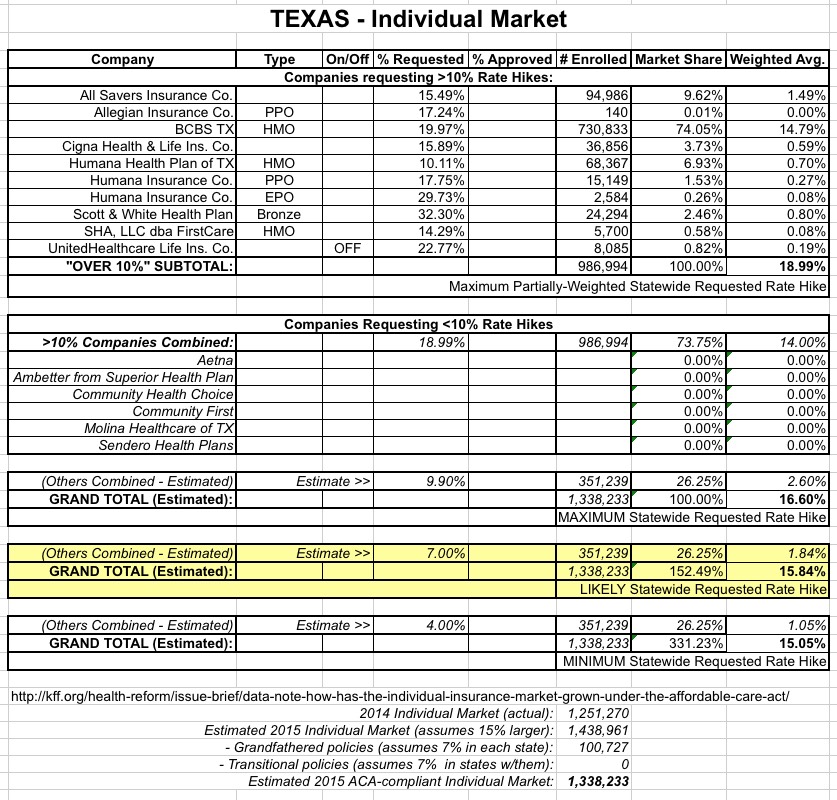

IMPORTANT:See this detailed explanation of how I've come up with the following estimated maximum weighted average rate increase request for Texas.

UPDATE 8/4/15: Revised table to display maximum, likely and minimum statewide average increase requests:

Assuming you've read through the explanation linked to above, here's my best estimate of the maximum possible rate increase requests for the Texas individual market:

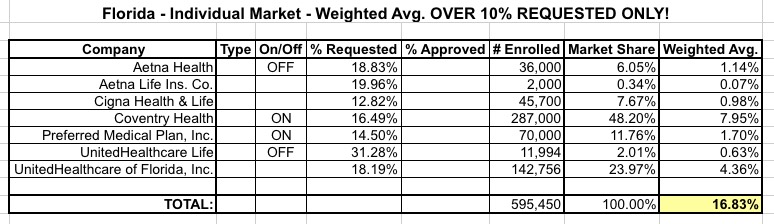

When I was crunching the numbers to come up with my rough estimate of the weighted average rate increase requests for Florida yesterday, I had a revelation: While Healthcare.Gov's Rate Review database, frustratingly, only includes rate requests higher than 10% (thus ignoring dozens of requests of under 10%, or even rate reductions in some cases), it doesstill at least provide guidance as to what the maximum average could possibly be.

For instance, let's say that there's a state with 4 insurance carriers, each of which has exactly 10,000 enrollees. Two of them are asking for a 20% and 15% increase respectively. Since those are both above 10%, they'll both show up on the Rate Review site:

In addition to the normal off-season "Qualifying Life Events" which allow roughly 7,500 people to select a private policy nationally every day, it looks like up to 100K additional people might be added to either the QHP or Medicaid tally over the next month or so:

CMS will offer a special enrollment period to thousands of Healthcare.gov enrollees who were incorrectly told that they qualified for fewer subsidies than they should have received or none at all, due to a Social Security-related glitch in the eligibility system that inflated household income.

...Tricia Brooks, a senior fellow at Georgetown University's Center for Children and Families who frequently writes on the issue, estimates that the glitch affects around 40,000 households.

Not sure how this slipped by me earlier today...I've been so busy trying to figure out the 2016 rate increases for each state that I missed this report from HHS about the 2015 premium and competition changes at Healthcare.Gov (this doesn't include the state-based exchanges, but still covers 2/3 of the states and 3/4 of total private enrollments):

Competition and Choice in the Health Insurance Marketplace Lowered Premiums in 2015

The Health Insurance Marketplace established by the Affordable Care Act allows consumers to compare health insurance plans based on key factors, such as covered services, providers, and importantly, price. According to a report released today, choice and competition increased in the 2015 Marketplace and consumers benefitted as new issuers entered and price competition intensified. In 2015, 86 percent of Marketplace-eligible consumers could choose from at least three issuers, up from 70 percent in 2014.

The Rate Review database at Healthcare.Gov is a very useful tool for any insurance company requesting rate increases above 10%, but it's completely useless for requests below 10%. As such, I have hard data on the requested increases for about 600,000 Florida residents:

If Florida's entire ACA-compliant individual market was only 600K people, that would be the end of the story.

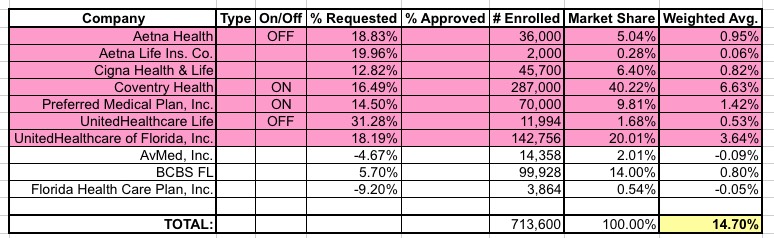

However, Florida actually has 16 different insurance companies selling individual policies...and the other 9 are all asking for lower than 10% hikes. After poking around the Florida Office of Insurance Regulation website as well as contacting the department directly, I've been able to pull together covered lives data for all 16, and requested rate change data for 3 more of them...2 of which are actually requesting rate decreases. When I add those 3 companies into the mix, the picture changes like so:

The Office of the Inspector General released a big report today which confirms what most healthcare/ACA observers have known for awhile now: The CO-OP organizations established by the ACA across 2 dozen states to help increase competition and keep the private, for-profit insurance companies (somewhat) honest...haven't been doing very well overall.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}