Usually when state regulators publicize their approved rate changes for carriers on the independent market, they list the various carriers and the approved average rate changes for each. I then simply plug these into my existing spreadsheet and get a before/after comparison against how much the carriers actually requested.

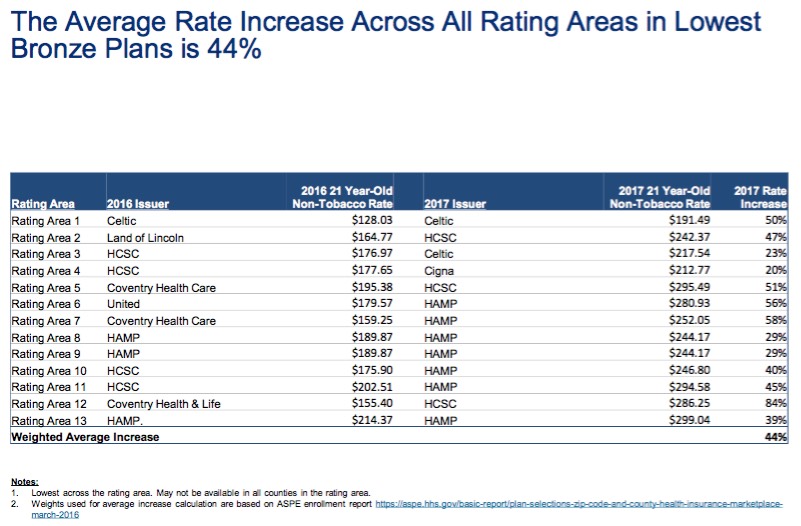

In the case of illinois, it's a little trickier. Unless I'm missing something, the only official notice the IL DOI has released is this PDF, which--while including lots of useful info about rating areas and so forth--doesn't actually list the overall statewide average approved rate increases by carrier.

Instead, it lists the averages based on metal level, and even then doesn't list all of the plans, just selected ones: Lowest-price Bronze, Lowest and 2nd Lowest-price Silver, and Lowest-price Gold, like so:

Virginia was the very first state which I ran an estimated 2017 average requested rate hike for, way back in mid-April.

Since then, aside from Humana pulling out (leaving just 1,800 current enrollees to find a new policy), Virginia's ACA exchange market has actually been remarkably calm; the state somehow managed to escape the wrath of both UnitedHealthcare and Aetna relatively intact, with both carriers still participating in the state's exchange next year as of this writing.

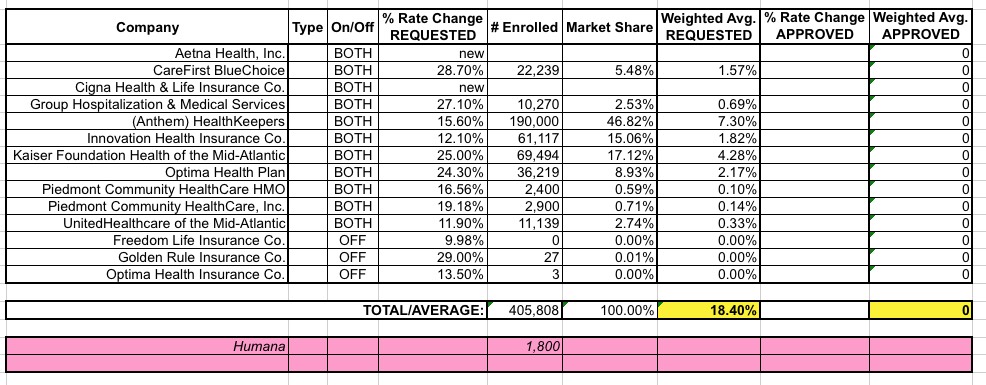

There have, however, been a few other changes to some of the rate filings here and there, found via this updated PDF on the VA DOI website as of July 19th. The overall average requested hikes don't really change much, but do nudge a bit higher than I had previously estimated, from 17.5% to 18.4%:

Physicians Health Plan of Northern Indiana announced Tuesday that it will quit selling individual insurance coverage next year through the federal Affordable Care Act.

The nonprofit PHP becomes the second insurer to announce it is leaving the HealthCare.gov insurance marketplace that serves residents of northeast Indiana. UnitedHealthcare said last spring it would drop out of the exchange in most states, including Indiana.

Four other insurers offered individual policies through HealthCare.gov this year in the Fort Wayne area and apparently will continue to do so in 2017. Insurers had until Tuesday to notify the state of their plans, and all four are among federal marketplace filings the Indiana Department of Insurance submitted Tuesday to the Department of Health and Human Services.

Fort Wayne-based PHP said it is paying $1.20 in medical expenses for every dollar it receives in premium payments from HealthCare.gov customers and has lost millions of dollars on the policies.

Following announcements by for-profit commercial carriers Humana and United Healthcare, nonprofits Health Alliance Plan and Priority Health are notifying agents they are pulling all PPO plans for 2017 from the Michigan health insurance exchange, Crain's has learned.

HAP has already announced it is pulling eight Personal Alliance individual preferred provider plans for individuals from the exchange and four PPO plans in the open market next year. HAP will continue to offer HMO individual plans on and off the exchange.

"We believe that these (PPO) plans do not represent the best value for the consumer," said Mary Ann Tournoux, HAP's senior vice president and chief marketing officer, in a statement. "At this time of cost-consciousness, we believe our remaining plans are the most cost-effective and offer our members and consumers greater value for their hard-earned insurance dollar."

About a month ago, when I first plugged in the average requested 2017 rate hikes for Georgia's ACA-compliant independent market, I came up with an overall weighted average of around 27.7%. However, there was one major gap in the data: I had trouble finding Ambetter/Peach State's enrollment numbers or even their average rate hike request, so I reluctantly left them out of the calculation completely.

When Aetna announced that they were dropping out of the Georgia exchange-based independent market, I went back and removed them from the mix. Since Aetna's request had been 15.5% on a substantial share of the market, this meant that the rest of the statewide average shot up to 32.0%.

Today I was able to track down the missing Ambetter/Peach State data--both the average requested rate hike (around 8.0%) as well as the number of current enrollees impacted...around 73,000:

With the growing concerns over expected large premium rate hikes next year, combined with the Big Announcements that major exchange players like UnitedHealthcare, Humana and Aetna are dropping out of most of the ACA exchange markets they're currently participating in, the HHS Dept. has obviously been under quite a bit of pressure to reassure exchange enrollees (both current and potential) to stay the course and not panic.

Thus, it's not surprising at all that an hour or so ago they released a new report which reminds people that nearly 4/5 of current ACA exchange enrollees will still be able to find an exchange-based Qualified Health Plan for $100 or less per month (and 3/4 could find one for $75 or less per month) after applying APTC assistance in the event of an across-the-board 25% premium rate increase in 2017:

OK. Last week I wrote up a post speculating about the potential impact to the state- and national-level average rate hike requests of Aetna dropping out of the ACA exchanges in 11 states. My conclusion was that the average will increase in some states...but may actually drop in others, since Aetna would otherwise have asked for rate hikes higher than the average requested by the other carriers in that state. Of course, this isn't really a positive development, since their current enrollees are still losing their plans entirely, and since a 50% hike from Aetna could still end up costing less than a 10% hike from one of the other carriers...but as always, this is the best I can do here.

According to a release from the company on Tuesday, the firm will no longer offer individual market plans through the Affordable Care Act in Dallas, Texas, and New Jersey.

..."We hope to return to these markets as we carry on with our mission to change healthcare in the US."

The "we hope to return" part suggests that Oscar will continue to be available off the exchange in New Jersey, since completely pulling out of a state means a carrier has to wait at least 5 years before re-entering. So...there's that, anyway.

...Oscar currently covers 7,000 people in Dallas and 26,000 in New Jersey.

As noted a couple of weeks ago, all three of the major insurance carriers participating in Tennessee's individual market ACA exchange asked for massive rate hikes this year, ranging from 44-62%. Blue Cross Blue Shield asked for 62% in the first place; Cigna and Humana resubmitted their original requests for higher ones.

Tennessee's insurance regulator approved hefty rate increases for the three carriers on the Obamacare exchange in an attempt to stabilize the already-limited number of insurers in the state.

...BlueCross BlueShield of Tennessee is the only insurer to sell statewide and there was the possibility that Cigna and Humana would reduce their footprints or leave the market altogether.

This was a double headache: First, because the actual enrollment numbers were only available for 3 out of 11 carriers via the filings; I had to get the rest from the MA exchange's monthly dashboard report. Secondly, even with the dashboard report, I had to merge together 2 different enrollment numbers for each carrier due to MA's unique "ConnectorCare" program.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}