Governor Andrew M. Cuomo today announced that the Special Enrollment Period for uninsured New Yorkers will be extended for another 30 days, through September 15, 2020, as the State continues to provide supportive services during the COVID-19 public health crisis. New Yorkers can apply for coverage through NY State of Health, New York State's health insurance marketplace, or directly through insurers.

"While we've crushed the curve of the virus, we are still in challenging times for hard-working families throughout the state who need access to quality, affordable health care," Governor Cuomo said. "The state has maintained low infection rates and is moving in the right direction, but we know we're not out of the woods yet. By offering this special enrollment period, we're making sure New Yorkers who need affordable and at times live-saving health care coverage can get it."

Back in March I noted that while the U.S. Supreme Court has indeed agreed to hear the Texas Fold'Em lawsuit to strike down the Affordable Care Act (aka "Texas vs. Azar", aka "Texas vs. U.S.", aka "CA vs. TX") sometime this fall, the odds of actually getting a final decision in the case from SCOTUS before the November election (or even before either Trump or Biden are sworn into office in January) is extremely unlikely:

#SCOTUS grants petition filed by California & other states, as well as petition filed by Texas on whether individual mandate can be separated from rest of ACA. Argument is likely in the fall, w/decision to follow by June 2021.

It was just a few weeks ago that the Montana Insurance Department posted the preliminary 2021 rate filings for the individual & small group markets. At the time, the individual market carriers were requesting a 3.2% average rate increase, while the small group carriers wanted a 2.4% bump.

Unfortunately, the actual actuarial filing memos ("Part II Justification") weren't available as of this writing, so I couldn't tell whether there's any COVID-19 impact specifically mentioned or not. Montana is one of the states with the fewest casese of COVID per capita, so I wasn't expecting much, but it would be nice to know.

Today I checked again and it looks like they've not only posted the Actuarial Memos (which don't mention COVID-19 at all, as I expected), but it also looks like Montana is the first state to publish their final/approved 2021 rate changes as well. They also modified the estimated enrollment numbers somewhat. Here's what it looks like now:

The good news is that both of last years' individual market carriers (Blue Cross Blue Shield and Bright Healthcare) do have listings for 2021 in the SERFF database.

The bad news is that those listings don't include actual rate filings, just some other forms.

The good news is that rate filings for every state appear to be available at RateReview.HealthCare.Gov this week.

The bad news is that the filings at RR.HC.gov appear to be incomplete so far; BCBS is listed but Bright isn't (and since I do have other forms for Bright being listed in 2021, I'm pretty sure it's not because they're pulling out of the Alabama market).

Welcome to the latest chapter in the long, epic CSR Lawsuit Saga which has been slogging along for six years now.

Here's a quick recap (again):

The ACA includes two types of financial subsidies for individual market enrollees through the ACA exchanges (HealthCare.Gov, CoveredCA.com, etc). One program is called Advance Premium Tax Credits (APTC), which reduces monthly premiums for low- and moderate-income. The other is called Cost Sharing Reductions (CSR), which reduces deductibles, co-pays and other out-of-pocket expenses for low-income enrollees.

In 2014, then-Speaker of the House John Boehner filed a lawsuit on behalf of Congressional Republicans against the Obama Administration. They had several beefs with the ACA (shocker!), including a claim that the CSR payments were unconstitutional because they weren't explicitly appropriated by Congress in the text of the Affordable Care Act (even though the program itself was described in detail, including the payment mechanism/etc.)

The data below comes from the GitHub data repositories of Johns Hopkins University, execpt for Rhode Island, Utah and Wyoming, which come from the GitHub data of the New York Times due to the JHU data being incomplete for these three states. Some data comes directly from state health department websites.

Here's the top 100 counties ranked by per capita COVID-19 cases as of Saturday, August 15th (click image for high-res version):

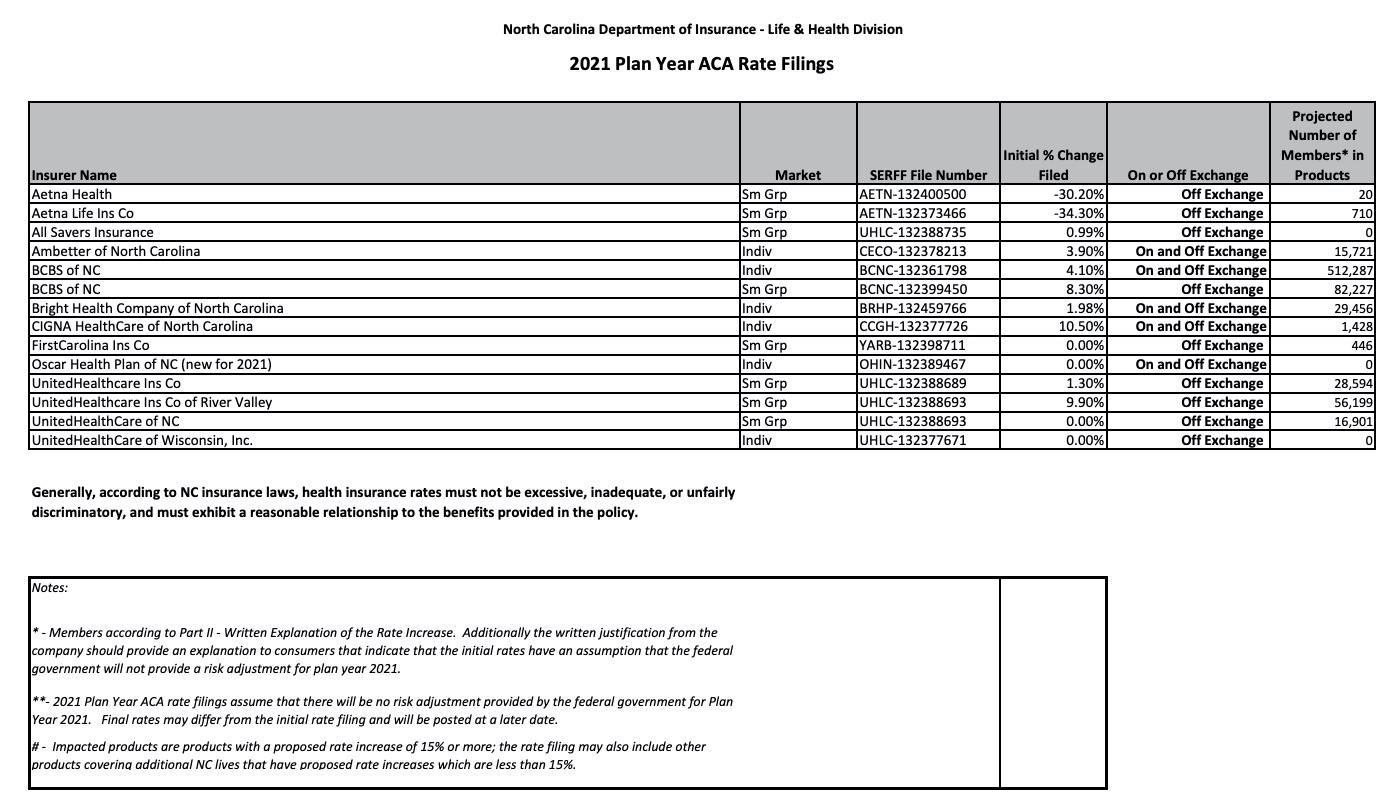

The good news is they include the number of people enrolled by each carrier in both markets, making it easy to calculate a weighted average, and th ey even include the SERFF tracking number for each.

The bad news is they don't include links to the actuarial memos, and even plugging the tracking numbers into the SERFF database only brings up the memos for three of the six carriers on the individual market...and of those, two of the three have been redacted (Oscar and Cigna), while the third (UnitedHealthcare) is brand-new to the North Carolina market anyway and therefore has no COVID-19 impact on their rate changes to speak of.

Are you turning 26 soon and still on your parent’s health insurance policy? Did you know that you will need to take action or you may no longer have health insurance? Don’t worry, you have options!

If you have a job that offers insurance, you can enroll in that coverage as turning 26—known as aging out—is considered a qualifying life event and will enable you to enroll in job-based coverage outside of your job’s open enrollment period.

Get covered through your school

If you are a college student, you may be able to enroll in a student health insurance plan through your school. Find out more

Nolan Finley is the conservative editorial page editor of The Detroit News.

Two weeks ago, he tweeted this out in response to criticism of the COVID-19 policy recommendations by himself and Michigan Republican legislative leadership:

Florida 20 million population, 6100 deaths. Michigan 10 million population, 6400 deaths. https://t.co/O1tNoyWwB0

Let's take a look at the data, shall we? Here's a graph of official COVID-19 positive test cases and fatalities per capita for both Michigan and Florida. Cases are per 1,000 residents; deaths are per 10,000 in order to make the trendlines more visible:

As I noted last year, the Nevada Insurance Dept. website is both helpful and frustrating when it comes to tracking down the type of data that I need. On the one hand they make it very easy to view the individual & small group market rate filing summaries: Carrier names, markets, sumission dates, status, effective dates and most importantly, the proposed and approved average rate changes are all easily found.

On the other hand, they don't actually link to the filing memos or URRT forms, which means I can't find the actual effectuated enrollment numbers for each carrier, the impact of COVID-19 on each carrier's request or other noteworthy info about the filings. Oddly, they do include the SERFF tracking numbers...except that plugging those into the SERFF database still doesn't bring anything up, which kind of defeats the point.

Fortunately, the NV DOI does provide the weighted average of the entire market and COVID-19 impact elsewhere. I've also been able to piece together the total market enrollment (both on & off-exchange) using some other public data.