Arkansas is a problematic state for many reasons, but I have to give their insurance dept. website high praise for posting their annual rate filings in a clear, simple & comprehensive fashion (which is to say, not only do they post the avg. premium changes for each carrier, they also post the number of covered lives for each, which is often difficult for me to dig up). Better yet, they also include direct links to the filing summaries and include the SERFF tracking number for each in case I need to look up more detailed info.

Anyway, there's nothing terribly noteworthy in the 2025 filings. Insurance carriers are seeking an average 4.2% rate hike on the individual market and 9.6% for small group plans.

HMO Partners (Health Advantage) appears to be dropping out of the small group market, but otherwise it looks pretty calm.

The big news on the individual market is that Aetna is seeking massive rate hikes of over 34% next year, though the weighted average across the board being requested is "only" a still ugly 13.3% increase.

On the small group market, average increases are the lower but still-not-great 8.8%. More significantly here is that Aetna and Optimum Choice are pulling out of the Delaware small group market entirely, reducing the number of carriers from six to just two, since Aetna had three divisions operating there.

The overall proposed average rate increase for 2025 Indiana individual marketplace plans is -1.6%.

The IDOI will finalize the review of the 2025 ACA compliant filings both on and off the federal Marketplace by August 16, 2024. The Centers for Medicare and Medicaid Services (CMS) will issue the ultimate approval for the Marketplace plans sold in Indiana. CMS will issue its approval on or before September 18, 2024.

CONNECTICUT INSURANCE DEPARTMENT RELEASES HEALTH INSURANCE RATE REQUEST FILINGS FOR 2025

The Connecticut Insurance Department (CID) has received eight rate filings from seven health insurers for plans that will be available on the individual and small group market, both on and off the state-sponsored exchange, Access Health CT. As part of our regulatory responsibilities, we will conduct a thorough examination of these filings to ensure that the requested rates comply with Connecticut’s insurance laws and regulations.

Hawaii only has two health insurance carriers serving the individual market, Hawaii Medical Service Assocation and Kaiser Foundation Health Plan. Both of them have submitted their proposed premium rate filings for 2025: HMSA is requesting a 7.6% hike, while Kaiser is only asking for a 4.0% bump. The weighted average is 6.4%.

On the small group market, the 5 carriers participating are requesting unweighted average increases of 7.1% statewide.

UPDATE 9/19/24: Hawaii regulators have uploaded the approved 2025 rate filings for the individual market only (I assume the small group filings will be uploaded soon). HMSA's rates will be going up slightly more than originally requested, but overall not much changed.

It's worth noting that Hawaii has a larger portion of its individual market enrolled in off-exchange policies than most states...around 37%, which means only 53% of the total indy market is subsidized at the moment.

Florida state law gives private corporations wide berth as to what sort of information, which is easily available in some other states, they get to hide from the public under the guise of it being a "trade secret." In the case of health insurance premium rate filing data, that even extends to basic information like "how many customers they have."

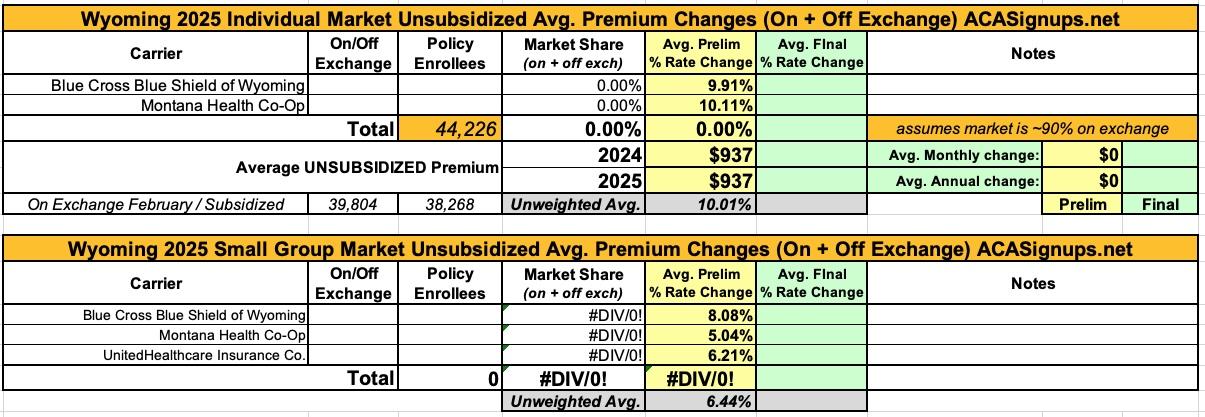

The bad news for Wyoming residents who earn too much to qualify for any federal ACA subsidies is that the state has the second highest unsubsidized premiums in the country after West Virginia. The good news is that, thanks to the Inflation Reduction Act, there are far more residents who do qualify for federal subsidies, which chop those premiums down to no more than 8.5% of their income....at least until the end of 2025, at which point the upgraded IRA subsidies are currently scheduled to expire.

Unfortunately, once again, I've been unable to get ahold of enrollment data for any of Wyoming's carriers on either the individual or small group markets, so I can only run unweighted averages for both markets.

With that said, the unweighted average rate hikes being asked for are 10% on the indy market and 6.4% for small group plans.

Wisconsin has the most competitive ACA markets in the country, at least in terms of the sheer number of insurance carriers offering policies on both the individual (14) and small group (16) markets. Their small group market is losing 2 carriers next year (All Savers and Common Ground Health Co-op), but it's still pretty robust.

The bad news is that it's once again extremely difficult to acquire Wisconsin's actual rate filings prior to the actual Open Enrollment Period launching, meaning I can only run unweighted average requested rate increases/decreases for the most part, although I've made a crude attempt at a partially-weighted average for the individual market.

With that in mind, individual market carriers are requesting unweighted increases of around 9.1%, while small group carriers are seeking hikes of around 7.4% overall.

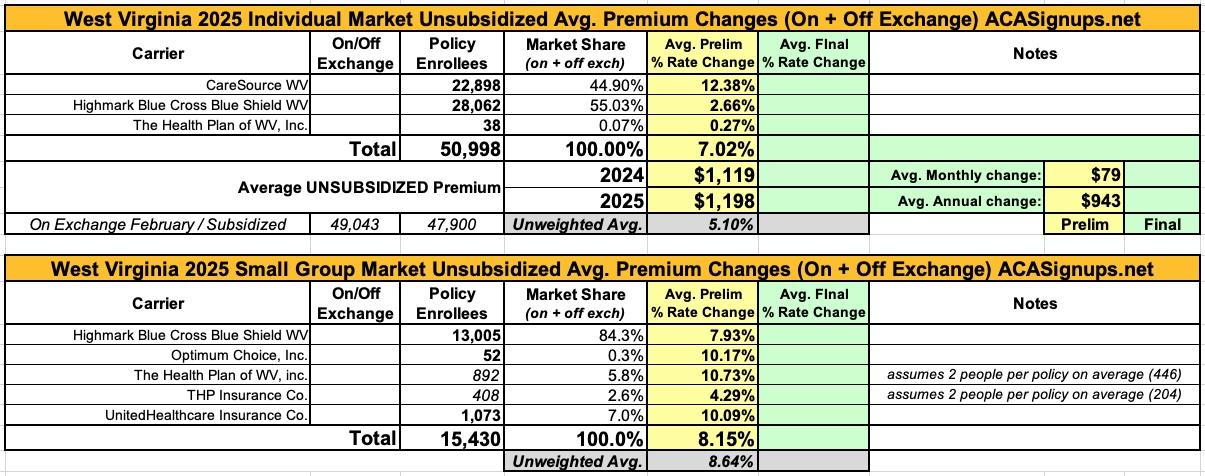

Well whaddya know? After years of their actuarial memos being redacted and/or filing summaries missing critical info, this year I'm suddenly able to access all the data I need!

West Virginia carriers are asking for average rate hikes of 7% on the individual market and 8.2% for small group plans.

The 7% hike is pretty close to the average nationally on a percentage basis...but since West Virginia also already has by far the highest average unsubsidized premiums in the nation, that's ugly news, especially if the enhanced ACA subsidies provided by the Inflation Reduction Act are allowed to expire starting in 2026...

Utah's preliminary 2025 individual and small group market rate filings are listed below. They launched a handy new website specifically dedicated to insurance filings, which is nice to see.

Unless there's a change in the final/approved rates, unsubsidized individual market plan premiums are increasing by around 10.4% in 2025, while small group plans will go up 8.9% on average.

It's worth noting that Cigna Health & LIfe is pulling out of Utah's individual market next year, while Angle Insurance Co. is dropping out of the small group market.

It's also worth noting that virtually all of Utah's individual market enrollment appears to be on exchange this year...over 95% of it! It's slightly lower than that since I don't know how many enrollees Cigna has at the moment, but they only reported around 3,000 effectuated enrollees as of a year earlier, so unless they had massive growth this year (which could have happened, I suppose), it would only knock the on exchange percentage down a point or two.

Cigna notwithstanding, this means that in Utah:

95.3% of all indy market enrollees are on exchange