One of the more obscure provisions of the ACA is the ability/funding for states to set up something called a "Basic Health Plan" for residents who are low income, but not that low income; it's sort of a "Medicaid Plus" program, in a way; here's the Kaiser Family Foundation's explanation:

The Patient Protection and Affordable Care Act (ACA) gives states the option to implement a Basic Health Program (BHP) that covers low-income residents through state-contracting plans outside the health insurance marketplace, rather than qualified health plans (QHPs). In March 2014, the Centers for Medicare & Medicaid Services (CMS) issued final regulations on the requirements for a BHP and the methodology for calculating federal payments to states. States can choose to implement BHP beginning in 2015.

I wrote about this last night as part of a larger piece, but the "Young Invincible Risk Pool" issue from yesterday's official Open Enrollment Report seems to be generating a lot of hand-wringing, so I decided to write something specifically about it.

One of the biggest concerns people have about the ACA exchanges is whether or not there are enough so-called "Young Invincibles" (ie, young adults aged 18-34 years old) in the market to help balance out the risk pool. The assumption is that "YI's" are considerably healthier than older folks, and therefore should help reduce the overall cost of medical services over the coming year. From an insurance carrier POV, it's a lot more profitable to have 10,000 healthy customers than 1,000 cancer or diabetes-ridden customers. In the past, of course, this meant that carriers would cherry-pick their enrollees; if they suspected you'd be a high risk customer, they'd simply tell you to go pound sand.

I'm not going to get into everything here, of course; a lot of this stuff is beyond my pay grade (which is to say, zilch, as I'm not paid to operate this site), while other stats just aren't of any particular interest to me, though obviously they may be useful to others. I'm mostly just running through all 81 pages (27 in the main report, 54 in the state-level supplemental) to see what catches my eye.

This entry will focus purely on the main report; I'll look at the supplemental report (which goes into state-level data) tomorrow.

Within the Marketplaces as a whole (all 50 states +DC):

(note: I'm live updating as I type this stuff, so keep checking back, I'll be adding more updates/analysis over the next hour)

Wow! OK, I'm back from my kid's field trip (nature center; they learned about how animals handle the winter via hibernation, migration & adaptation...learned about fossils...went on the nature trail to look for animal tracks...and even dissected owl pellets, hooray!!). Of all the days to miss a major HHS/CMS conference call, this was a big one. I'm furiously poring over the HHS Dept's ASPE January Enrollment Report which, as I expected this morning, was just released less than two hours ago.

There's some sort of press conference call this afternoon with official updates on the 2016 Open Enrollment Period. Unfortunately, I have a field trip to attend with my kid all afternoon, and a client call after that, so I won't be able to get in on the call, nor will I be able to write anything up about whatever's discussed (or any press releases which come out after the call) until several hours later.

Since enrollments over the past two weeks have been virtually dead due to a) the January coverage deadline having passed for all states; b) Christmas week and c) New Year's week, my guess is that the major reasons for today's call will include:

Here's what I wrote last July, when Gallup released their 2015 Q2 Uninsured Rate survey (which pegged the uninsured rate among adults (over 18) at 11.4%:

Going forward, I'm actually not expecting the Q3 2015 Gallup survey to show much of a change; we're in the heart of the off-season, the #ACATaxTime additions have already been accounted for, and Montana is the only state which is expected to expand Medicaid anytime soon, so Q3 will probably hold steady at 11.4%, give or take; the rate might even inch up a few tenths of a percent due to attrition. Still, the overall picture is pretty dramatic: Whatever else you can say about the ACA in terms of cost, it's definitely accomplishing the other half of its goal: The total number of uninsured Americans has been cut by about 16 million people since October 2013.

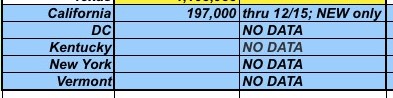

If you look at the State-By-State OE3 enrollment breakdown, you'll notice that there are still 4 blank fields all the way down at the bottom, plus a special note regarding California:

I launched the "State by State" chart feature towards the end of the 2015 Open Enrollment period last time around, and it proved to be pretty popular, so I've brought it back this year.

It's important to note that I'm still missing data from some state exchanges; I have bupkis from DC, Kentucky, New York or Vermont. I also only have partial data from others (California includes new enrollees only, while several other states only have data for the first couple of weeks).

With all those caveats out of the way, here's where things stand. Just like last year:

So what about this week? Well, it should play out very much the same: Practically all QHP selections going forward should be for new additions, and we have New Year's Eve and Day included. Sure enough, last year there were just 103K added to HC.gov from 12/27 - 01/02...slightly more than Christmas week.

Assuming this year follows a similar pattern, there should be roughly 80,000 people tacked onto the HC.gov total for Week 9, bringing the cumulative total up to just over 8.6 million.

If this does happen, then yes, I'll have to seriously re-evaluate my current 14.7 million OE3 projection...because that will suggest that the final 5 weeks are gonna play out a good 20% lower than my expectations.

And if that's the case, then instead of another 3.5 million new folks signing up, it'll only be around 2.8 million...bringing a grand total of right around 14.0 million even.

Ah. OK. Well, this time it's different, because this time, the Republican-controlled Senate has signed onto repealing the ACA as well, which means that it'll actually make it as far as President Obama's desk for once, requiring him to...pull out a pen and veto it.

...as Majority Leader Kevin McCarthy puts it, that’s the goal: “With this bill, we will force President Obama to show the American people where he stands.”