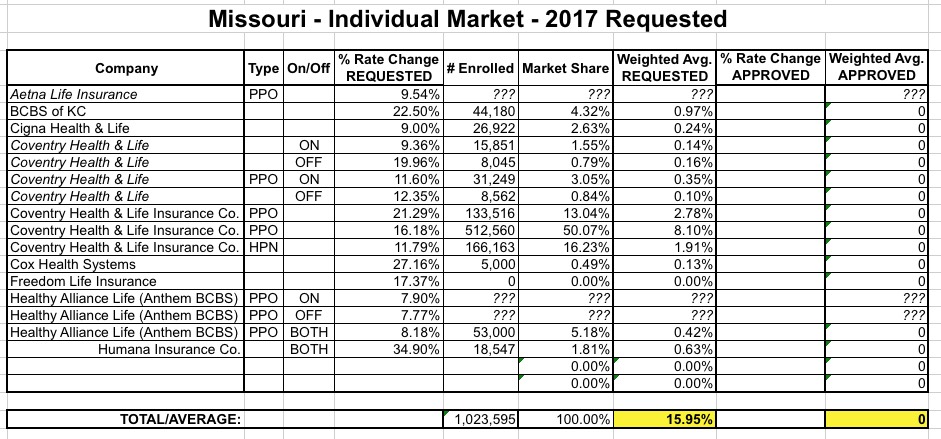

OK, there's something very odd going on with Missouri's 2017 rate filings for the individual market. According to the Kaiser Family Foundation, Missouri's entire individual market was around 344,000 people in 2014. While it's likely increased by around 25% since then, that would still only bring it up to around 430,000 people including both grandfathered and transitional enrollees, which sounds about right to me (290,000 enrolled via the ACA exchange, which would leave around 140,000 off-exchange).

And yet, when I plug in the official rate filings for Missouri's individual market for 2017, here's what it looks like:

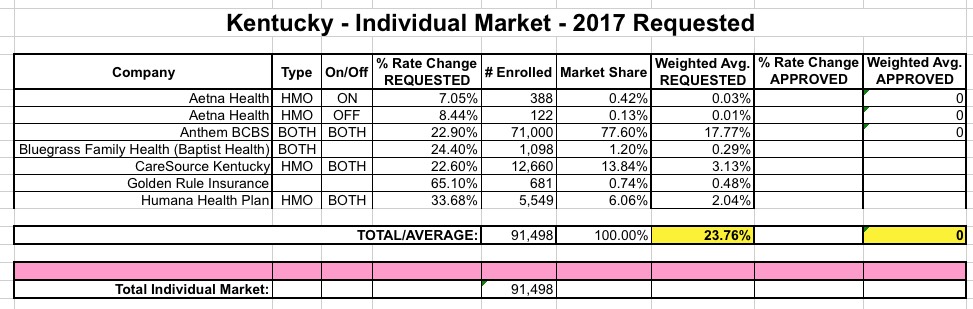

Not much to say about the bluegrass state...taken together, the 6 carriers offering individual policies in Kentucky appear to be requesting an average rate hike of 23.8%, ranging from Aetna's single-digits for a few hundred people up to Golden Rule's stroke-inducing 65% hike. One thing to note is that KY's total individual market was around 163,000 people in 2015, and is likely around 25% higher today (around 203,000), so over half of the market is likely missing from this table:

With only 584,000 residents, Wyoming is the smallest state, with a population over 10% smaller than even the District of Columbia or Vermont. Last year there were only 2 insurance carriers offering individual policies on the ACA exchange, Blue Cross and WINhealth. The average rate increase for 2016 was right around 10% even.

WINhealth sent along this release saying: As of October 8, 2015, WINhealth has chosen not to participate in the individual market, to include the federal exchange, for the 2016 plan year. The decision not to participate stems from a recent announcement from the federal government regarding the risk corridor program .

Last year, the Texas ACA-compliant individual market carriers requested an average rate hike of around 16%, although it was a pretty fuzzy guesstimate since I couldn't track down the average rate hikes for about 25% of the market other than knowing that whatever it was, it was under 10%.

This year, the good news is that CMS has started postingall rate change requests whether over or under 10%, making it easier to fill in some of the data. The bad news is that 3 of the 19 carriers offering individual policies next year redacted any data giving a clue as to what their current enrollment numbers are: CHRISTUS, Community First and Oscar Insurance.

The other 16 carriers did provide those numbers pretty clearly (except for Sendero, which only gave a projection of "member months" which I had to divide by 12 to get a rough enrollment estimate).

When the dust settled, there were 11 Co-Ops left standing, but most of them were still on pretty shaky ground, with all but a handful placed under "enhanced oversight" by their states (and I have to admit that the term sounds an awful lot like a euphamism, a la "enhanced interrogation technique").

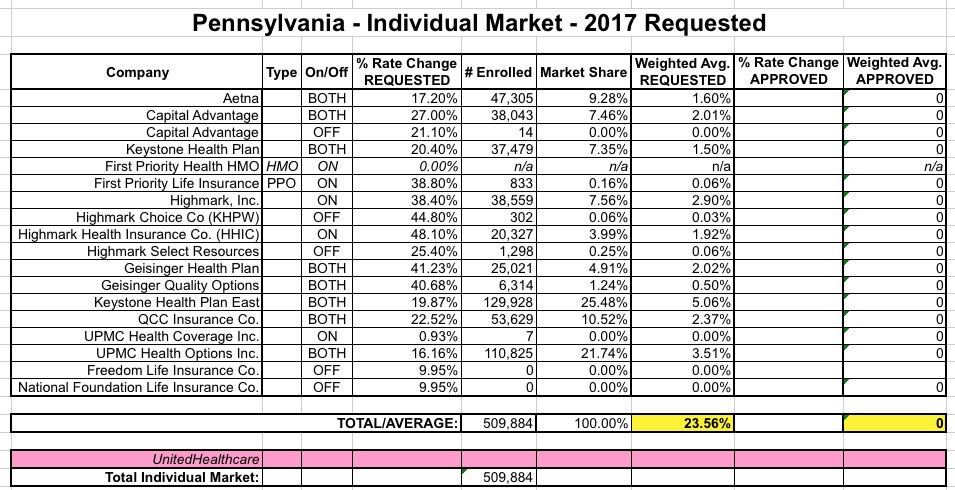

Last year, the insurance carriers in Pennsylvania asked for a weighted average 15.6% rate increase for individual market policies...but in the end state regulators knocked these down by over 1/5th to around 12% overall.

This year the picture is uglier, as expected. While four of the filings are for rate hikes of under 10%, this is misleading because one of them appears to be brand new while the other 3 have a combined enrollment of...7 people. Not 7,000, not 700...seven.

The rest of the filings range from 16% to a whopping 48% increase request from Highmark Health Insurance for over 20,000 enrollees. Ouch.

Overall, the weighted state-wide average requested rate hike on the individual exchange is 23.6%.

What Would Happen if Donald Trump’s Healthcare Plan Was Implemented?

Imagine this scenario next year.

In January, President Donald J. Trump asks Congress on his first day in office to repeal Obamacare.

The House and Senate oblige and eight months later on Oct. 1 the Affordable Care Act (ACA) goes out of business.

In its place, the seven-point healthcare plan listed on the Trump campaign website is implemented.

...“It will make the healthcare industry more affordable and more accessible,” Sam Clovis, the national co-chairman and a policy advisor for the Trump campaign, told Healthline.

However, five experts interviewed by Healthline don’t see quite as rosy a picture.

...“Not everybody needs to have health insurance,” said Clovis. “Healthy people having to pay the insurance costs of unhealthy people is a nonstarter.”

The good news about estimating the DC exchange rate hike requests is that the DC Dept. of Insurance, Securities & Banking is pretty transparent about posting this info, and they keep it simple. It's simpler still because like Vermont, DC requires that all individual and small group policies be sold on the exchange, so there's no off-exchange data to track down.

The bad news is that it's a little bit too simple: Only two carriers (CareFrist and Kaiser) offer policies via the individual exchange, and only CareFirst is offering PPOs: