The Washington Health Benefit Exchange today announced that more than 200,000 people purchased their 2019 health insurance coverage through Washington Healthplanfinder, the state’s online health insurance marketplace, during the most recent open enrollment period held Nov. 1 through Dec. 15 of last year.

Even with the four percent decrease in total number of enrollments reported from February of 2018, the Exchange saw more than 90 percent of those who selected a 2019 health plan during the open enrollment period make their initial premium payment.

A 4% drop may sound bad, but total QHP selections during OE6 were actually down 8.3% year over year (from 243K to 223K), so this is actually an improvement in that sense. 90.5% of those who selected policies are still effectuated as of February this year vs. 86.4% as of February in 2018.

Vermont is among the few states which also releases their off-exchange numbers, and it's a good thing they do that because it helps explain the 12.3% drop in on-exchange enrollment this year. In short, thanks to VT making the move to active #SilverSwitching for 2019, several thousand people moved from on-exchange Silver ACA plans to nearly-identical off-exchange Silver plans.

Anyway, today they issued a formal press release with additional details...and at the same time bumped up the official enrollment tally by a bit:

2019 Individual Enrollment Report Shows More Vermonters are Covered

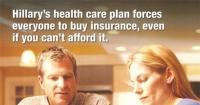

Shoutout to James Medlock for digging up this relic from the 2008 Presidential primariy race: A lit piece from then-Senator Barack Obama's campaign slamming then-Senator Hillary Clinton over her insistence on her proposed healthcare policy bill including an Individual Mandate Penalty. How many Republican talking points can you spot below?

There's a lot going on here. For starters, the couple on the first page are basically 2008 versions of "Harry & Louise"...it's a white, middle-age, middle-class suburban couple poring over their finances. Considering that the 1993 "Hillarycare" proposal was destroyed in large part due to the health insurance lobby's successful series of Harry & Louise "there's got to be a better way" ads, Obama using this same tactic had to sting.

HealthSource RI enrollments up by nearly 2,000 customers as RI’s uninsured rate reaches all-time low

Feb 25, 2019

According to the latest Rhode Island’s Health Information Survey, only 3.7% of Rhode Islanders were uninsured in 2018, down from 4.2% in 2016.

HealthSource RI’s individual and family enrollments increased by 1,849. This Open Enrollment, 32,486 customers enrolled and paid compared to 30,637 last year.

The "...and paid" caveat is important. Last month HealthSource RI reported 34,533 QHP selections after the 2019 OEP wrapped up, so that's an impressive 94% paid/effectuated rate. For comparison, last year 30,637 paid out of 33,021, or 92.8%, so they've improved on that front as well.

By the close of this year’s Open Enrollment, Coloradans had selected 169,672 medical insurance plans, which compares to 165,777 medical plan selections for the 2018 Open Enrollment period.

Hmmm...I'll have to look into these numbers a bit further. Colorado's 2018 Open Enrollment total was indeed 165,777 according to C4HCO...but according to CMS's official report it was only 161,764 QHP selections. This is the same thing which happened last year, when C4HCO reported 172,361 QHPs vs. CMS's 161,568. It's therefore possible that the final/official 2019 CMS report will put Colorado's total around 4,000 enrollees lower than my own numbers.

However, either way, Colorado joins Massachusetts in increasing their ACA open enrollment numbers every year for five years straight, bucking the national trend!

A couple of weeks ago, Louise Norris gave me a heads up that not only has the New Mexico Insurance Dept. restricted the sale of non-ACA compliant "short-term, limited duration" plans to be...you know...both short term and of limited duration via regulation...

In September 2018, the New Mexico Office of the Superintendent of Insurance (OSI) and Health Action NM (an advocacy group for universal access to health care) presented details about potential state actions to stabilize the individual market. OSI has the authority to regulate some aspects of the plans, including maximum duration, but they noted that legislation would be needed for other changes, including minimum loss ratios and benefit mandates.

New Mexico’s insurance regulations were amended, effective February 1, 2019, to define short-term plans as nonrenewable, and with terms of no more than three months. The regulations also prohibit insurers from selling a short-term plan to anyone who has had short-term coverage within the previous 12 months.

Last week, the state of Arkansas released its latest round of data on implementation of its Medicaid work reporting requirement – the first in the country to be implemented. As readers of SayAhhh! know, over 18,000 lost coverage in 2018 as a result of not complying with the new reporting rules. And the policy is clearly failing to achieve its purported goal – incentivizing work – with less than 1% of those subject to the new policy newly reporting work or community engagement activities.

Minnesota's new Democratic (pardon me..."Democratic-Farmer-Labor", or DFL) Governor, Tim Walz, has just posted his proposed state budget for the next fiscal year, and it includes some fantastic expansions & improvements to the healthcare system of Minnesota, including both state-level ACA enhancements and a push for a robust Public Option, along with other ideas.

Bill expanding ‘Insure Oklahoma’ program passes Senate committee

A Senate bill seeking to expand the Insure Oklahoma program has advanced out of committee Monday morning.

Senate Bill 605, authored by Sen. Greg McCortney, R-Ada, directs the Oklahoma Healthcare Authority to implement "the Oklahoma Plan" within Insure Oklahoma. An agency spokesperson said the program provides premium assistance to low-income working adults employed by small businesses.

The latest numbers from Insure Oklahoma show less than 19,000 are enrolled.

According to McCortney, the intent of his bill is to provide insurance for Oklahomans who would qualify for Medicaid in states which opted to expand but are currently not insured.