Not much to report about the 2024 individual and small group market rate filings. I could only find current enrollment numbers for two of the three indy market carriers and for three of the five small group market carriers. However, based on last year's total enrollment, I'm estimating ND's total indy market at being roughly 50,000 people, which means I was able to make an educated guess at how many are enrolled in Sanford Health Plan policies.

Based on this, I have a (mostly) weighted requested average rate increase of 4.4% for individual market plans and an unweighted average of 6.5% for small group market plans.

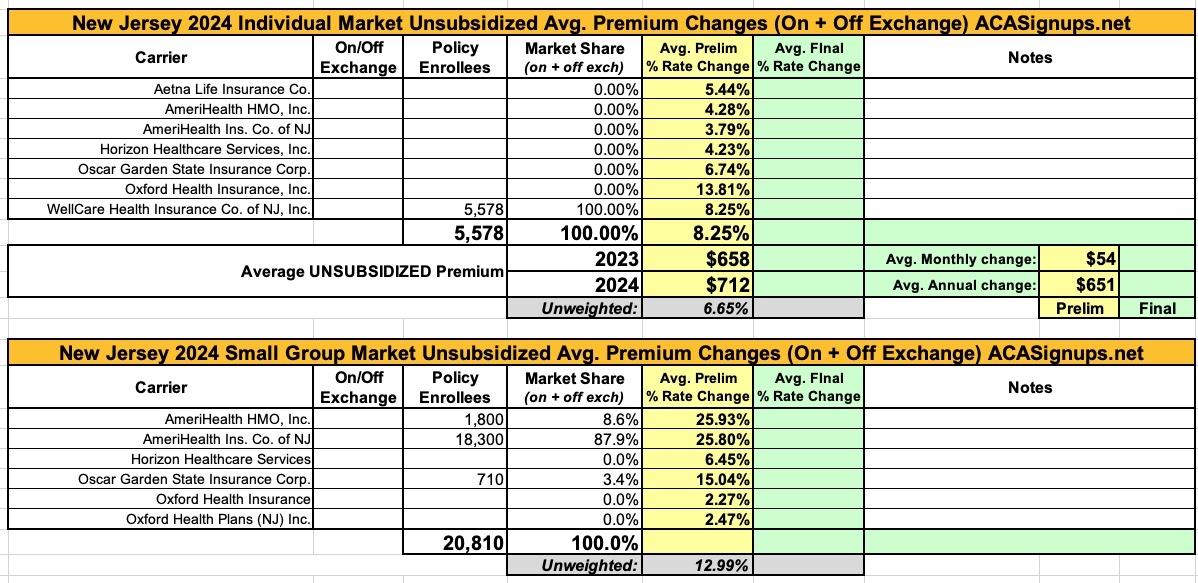

New Jersey individual & small group market carriers are asking for unweighted average rate increases of 6.7% and 13.0% respectively for 2024. However, the unweighted averages don't tell the whole story--the carriers are asking for rate hikes ranging from as low as 3.8% to as high as 13.8% on the individual market, and from as low as 2.3% to a stunning 25.9% for small group plans.

As is the case with far too many states these days, most of the rate filing memorandums are heavily redacted in New Jersey, making it nearly impossible to get ahold of the actual enrollment numbers, which means I have no way of running a weighted average on either market.

The good news about New Hampshire's health insurance market is that they're the only state without its own ACA exchange which produces publicly-accessible monthly reports on individual on-exchange market enrollment. The bad news is that they don't seem to publish the actual rate filings in an easy-to-read format, which means I'm left with the federal rate review website, which sometimes posts average rate requests which don't match up with the actual filings...but it's gonna have to do here.

With these two data sources in hand, New Hampshire's individual market carriers are asking for a weighted average increase of 3.1%. It's important to note that Anthem Health Plans and Matthew Thornton Health Plan are listed as separate carriers on the federal Rate Review website (with separate average rate requests), but on the state's monthly report, they're merged into a single listing.

Nevada used to be a state where the annual individual & small group rate filings were fairly transparent. They have a pretty easy-to-use searchable filing database which clearly lists the carriers, market, maximum & minimum rate changes and even includes the SERFF Tracking numbers for every filing.

Unfortunately, this year at least, most of that proves useless for my purposes. The average rate changes are posted, but the enrollment data is still hidden from public view--entering the SERFF Tracking Numbers still brings up nothing in the SERFF database, and the actuarial memos posted at RateReview.HealthCare.Gov are mostly redacted. As a result, I'm only able to enter enrollment data for one of the nine carriers on the Nevada individual market, and none on the small group market.

Interestingly, the one I have enrollment data for (Aetna Health of Utah) also has a curious discrepancy: The filing itself lists the average requested rate increase as being 6.97%, but on the RR.HC.gov site it only shows up as 1.36%. The other eight carriers all match up (or are within a tenth of a percentage point, anyway).

Massachusetts, which is arguably the original birthplace of the ACA depending on your point of view (the general "3-legged stool" structure originated here, but the ACA itself also has a lot of other provisions which are quite different), has 10 different carriers participating in the individual market.

One thing which sets Massachusetts (along with Vermont) apart from every other state is that their Individual and Small Group risk pools are merged for premium setting purposes.

Normally you would think this would make my job easier, since I only have to run one set of analysis instead of two...but until recently, it was surprisingly difficult to get ahold of exact enrollment data for each carrier on the merged Massachusetts market (and even more difficult to break out how many are enrolled in each market since they're merged...not that that's relevant to the actual rate changes).

Kentucky is yet another state where the actuarial memos are heavily redacted, making it difficult to acquire information such as the number of enrollees...which in turn makes it impossible to run a weighted average requested rate change for the individual or small group markets.

There are four carriers offering policies on the KY individual market (Anthem, CareSource, Molina and WellCare), with an unweighted average rate change request of 4.1%. Molina has provided an unredacted actuarial memo which includes their enrollment...but it's only 505 people, while KY's total indy market is likely closer to 75,000 or so including the off-exchange market.

The IDOI will finalize its review of the 2024 ACA compliant filings both on and off the federal Marketplace by August 17, 2023. The Centers for Medicare and Medicaid Services (CMS) will issue the ultimate approval for the Marketplace plans sold in Indiana. CMS will issue its approval on or before September 20, 2023.

Not a whole lot stands out to me other than Cigna apparently dropping out of the states indy market and Humana pulling out of the small group market. Otherwise, neither market has rate changes which seem terribly surprising--they come to a weighted average increase of 4.3% for individual market plans and 6.6% for the small group market.

As always, these are subject to state regulatory review and approval.

The most noteworthy developments below are that in addition to Friday, Oscar and Bright Health Plans all leaving the Colorado market (as documented/reported on several times earlier this year), it looks like Anthem is reducing its offerings on the individual market, while Aetna and Humana both appear to be dropping out of the states small group market.

Update: Correction, apparently I misread that about Anthem; they have the same total number of plans available after all...not sure how I messed that up; apologies. Their Rocky Mountain division is offering off-exchange policies only, abut aren't listed on CO DARA's summary for whatever reason.

In any event, the weighted average increase being requested is 9.8% on the individual market and 10.6% for the small group market.

Each year, the Idaho Department of Insurance posts rate changes of individual and small group health insurance products so consumers can review and provide comments on the proposed increases. Insurance companies submit proposed rates for the upcoming calendar year to the Department, along with descriptions and justifications for why the rates are reasonable and not excessive.

The Department of Insurance is seeking public input for rate changes of individual and small group health insurance products to improve insurer accountability and transparency. By following the links below, the public can access a summary of the increase amounts and the carrier justifications for the rates. Please submit any comments to the Department for consideration.