A couple of weeks back, the Kaiser Family Foundation crunched the numbers to see just how much insurance carriers would likely raise their full-price premiums on individual market policies to make up for lost CSR assistance reimbursements in the event that Donald Trump makes good on his threat to discontinue them. Their conclusion?

A new Kaiser Family Foundation analysis finds that the average premium for a benchmark silver plan in Affordable Care Act (ACA) marketplaces would need to increase by an estimated 19 percent for insurers to compensate for lost funding if they don’t receive federal payment for ACA cost-sharing subsidies.

Again, that's an average onf 19% on top of whatever the carriers would otherwise be increasing rates for other reasons.

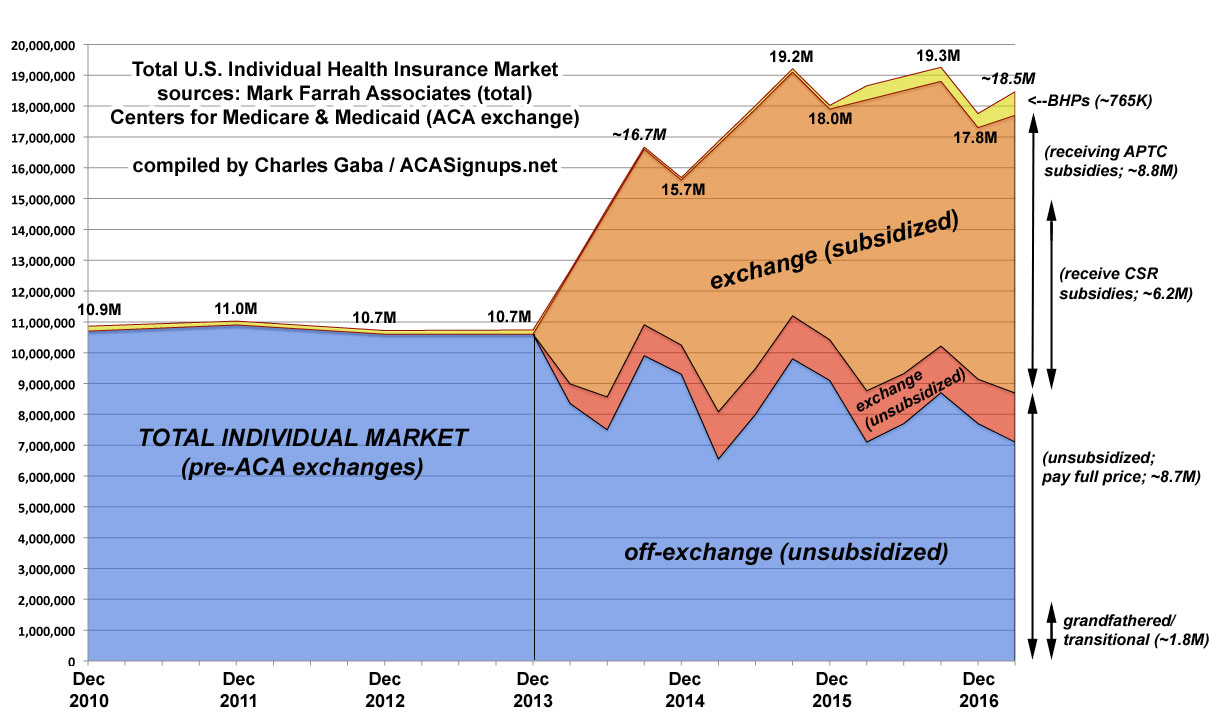

As I posted yesterday, here's a rough overview of what total Individual Market Enrollment has looked like since 2010, and how Trump's threat to cut-off CSR reimbursements would impact it:

The blue section is off-exchange enrollees...around 7 million people today, all of whom are paying full price. This includes perhaps 1.8 million people still enrolled in Grandfathered or Transitional plans (which are part of a separate risk pool), although that number is highly speculative.

Well THAT figures: Insurance carriers finally breaking even on ACA exchanges just in time for GOP to tear up the law.

Health insurers may finally be seeing improved results on their Obamacare plans just as a newly elected president is poised to follow through on promises to end the controversial coverage program, a new report suggests.

An analysis out Thursday says that health insurers are expected in 2016 "to start reversing" financial losses on their Obamacare business after "hitting bottom" in 2015.

And 2017 "will likely see continued improvement" for those insurers selling individual health plans, "with more insurers getting close to breakeven or better," according to the report by Standard and Poor's Global Ratings.

UPDATE: ...or, perhaps not. Latest word is that there's basically little to see here; lots of big talk about pushing forward but very little action. Or perhaps there will be next week, who the heck knows? Wash, rinse, repeat.

On March 24th, just after the AHCA (Trumpcare) bill was yanked from the House floor with literally minutes to go, I posted the following headline:

CELEBRATE A FEW HOURS. Then come back and read this.

...and then went on to conclude that, given the insane amount of uncertainty and confusion about what Donald Trump, Tom Price and the Congressional GOP in general has in mind for the 2018 insurance market, on top of normal stuff like inflation, an aging population and so on, that there are five likely scenarios:

Now, put yourself in the position of an insurance carrier executive and/or one of their actuaries. The level of uncertainty in the air is mind boggling. You have five choices for your initial filing:

Last week, former CMS Administrator Andy Slavitt conveyed a warning to the Trump Administration and the GOP about how critical confirming ongoing Cost Sharing Reduction reimbursements (not just for the rest of 2017, but continuing into 2018) is, by paraphrasing multiple anonymous sources within the health insurance industry.

The Trump administration says it is willing to continue paying subsidies to health insurance companies under the Affordable Care Act even though House Republicans say the payments are illegal because Congress never authorized them.

The statement sends a small but potentially significant signal to insurers, encouraging them to stay in the market.

UPDATE 6/8/18: Welp. Given last night's bombshell development that Donald Trump's Department of Justice has decided to not only abandon doing their jobs by defending the law of the land but to actually actively argue in favor of tearing away the ACA's prohibition of denying coverage for (or charging more for) pre-existing conditions, it seemed appropriate to dust off this entry from over a year ago.

A couple of important caveats: The individual market has shrunk by one or two milion people since a year ago (due in large part to other forms of Trump/GOP sabotage, I should note), so most of the estimates for the last column are likely a bit smaller as well, although those with pre-existing conditions are the least-likely to drop their coverae for that very reason. Also, a good half-dozen Congressional Districts have had special elections over the past year and now have new members of Congress (SC-05, MT-AL, PA-18 and so on) or currently have vacancies not shown below (MI-13, TX-27, etc).

Last fall, when the insurance carriers were jacking up their rates on the individual market by an (unsubsidized) national weighted average of around 25%, aside from the understandable grumbling about such a dramatic all-at-once increase, the big question was whether that would be enough to stabilize the market going forward, or whether this was just the beginning of an inevitable Death Spiral, etc etc.

An analysis out Thursday says that health insurers are expected in 2016 "to start reversing" financial losses on their Obamacare business after "hitting bottom" in 2015.

And 2017 "will likely see continued improvement" for those insurers selling individual health plans, "with more insurers getting close to breakeven or better," according to the report by Standard and Poor's Global Ratings.

The report also says big price increases for Obamacare plans in 2017 were likely a "one-time pricing correction."

OK, I was about to go with the more obvious saying: "Sh*t or get off the pot", but I'm trying to avoid blatant profanity in the headlines, at least.

Here's a tweetstorm from fomer director of the Centers for Medicare & Medicaid, Andy Slavitt, from yesterday/continuing through today. He confirms everything I've been sounding the alarm about, especially regarding the CSR payment crisis:

One of the questions I get asked most frequently is why don't more health plans speak up about what a disaster AHCA would be. 1

A new Kaiser Family Foundation analysis finds that the average premium for a benchmark silver plan in Affordable Care Act (ACA) marketplaces would need to increase by an estimated 19 percent for insurers to compensate for lost funding if they don’t receive federal payment for ACA cost-sharing subsidies.