The Maine Department of Health and Human Services (DHHS) Office of the Health Insurance Marketplace (OHIM) will release biweekly updates on plan selections through CoverME.gov, Maine’s Health Insurance Marketplace.

Plan selections provide a snapshot of activity by new and returning consumers who have selected a plan for 2024. “Plan selections” become “enrollments” once consumers have paid their first monthly premium to begin insurance. These numbers are subject to change as consumers may modify or cancel plans after their initial selection.

The deadline to select a plan for coverage beginning January 1, 2024 is December 15, 2023. Consumers who select a plan between December 16, 2023 and January 16, 2024 will have coverage beginning February 1, 2024.

The Maine Department of Health and Human Services (DHHS) Office of the Health Insurance Marketplace (OHIM) will release biweekly updates on plan selections through CoverME.gov, Maine’s Health Insurance Marketplace.

Plan selections provide a snapshot of activity by new and returning consumers who have selected a plan for 2024. “Plan selections” become “enrollments” once consumers have paid their first monthly premium to begin insurance. These numbers are subject to change as consumers may modify or cancel plans after their initial selection.

The deadline to select a plan for coverage beginning January 1, 2024 is December 15, 2023. Consumers who select a plan between December 16, 2023 and January 16, 2024 will have coverage beginning February 1, 2024.

As Open Enrollment launches today, tens of thousands of Mainers qualify for help to pay their monthly premiums

AUGUSTA — The Maine Department of Health and Human Services (DHHS) announced today that Maine people can now visit CoverME.gov to shop for and enroll in 2024 coverage that fits their needs at a price that works during the Open Enrollment Period that kicks off today, November 1, 2023.

At CoverME.gov, Maine's Health Insurance Marketplace, Maine people can compare private plans, apply for financial savings, and enroll in a 2024 health or dental insurance plan. All plans offered on CoverME.gov provide quality, comprehensive insurance that protects consumers if they have an accident or major illness and fully pays for preventive screenings. This year, Maine people can continue to take advantage of additional federal financial assistance that makes insurance more affordable.

As Open Enrollment approaches on November 1, 2023, Maine residents can get an early look at 2024 health insurance options that meet their needs and budgets

The Maine Department of Health and Human Services (DHHS) Office of the Health Insurance Marketplace (OHIM) announced today that Maine people can now visit CoverME.gov to preview quality health plans for 2024 in advance of Open Enrollment, which begins on November 1, 2023.

During this “window-shopping” period, consumers can use the Plan Compare Tool to evaluate available private health insurance plans and estimate their costs without having to sign up for an account or complete a full application. The tool also allows consumers to view information about coverage and out-of-pocket costs for prescription drugs.

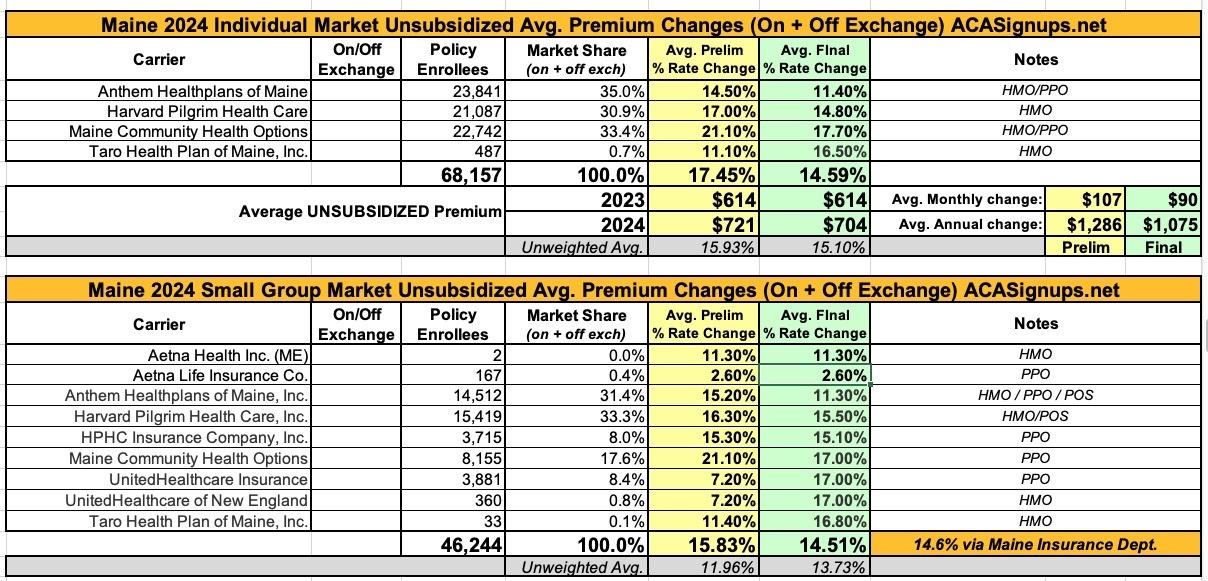

At the time, the weighted average rate increases requested by insurance carriers in Maine were a steep 17.9% hike for the individual market and a 15.8% increase on the small group market.

Each year insurers that sell Individual and Small Group plans in Maine's pooled risk market must submit their proposed forms and rates to the Bureau of Insurance, using the System for Electronic Rate and Form Filing (SERFF). Details of the filings submitted to the state since June 10, 2010 can be viewed in the system.

To see details of a filing, click on the Search Public Filings button below and paste or type in the relevant SERFF Tracking Number listed in the table (no need to complete the rest of the form).

Individuals losing eligibility for MaineCare can enroll in plans on CoverME.gov through July 31, 2024

AUGUSTA— The Maine Department of Health and Human Services (DHHS) announced today the launch of a Special Enrollment Period (SEP) through CoverME.gov, Maine’s Health Insurance Marketplace, to help Maine people transitioning from MaineCare coverage after the COVID-19 pandemic explore affordable health insurance options and avoid gaps in coverage. The Special Enrollment Period began on April 15, 2023, and will continue through July 31, 2024, allowing Maine individuals found no longer eligible for MaineCare to apply for plans through CoverME.gov outside of the annual Open Enrollment Period.

The Maine Department of Health and Human Services (DHHS) is urging Maine residents who lack affordable health insurance to sign up by the deadline of Sunday, January 15, for a 2023 health plan through CoverME.gov, Maine’s health insurance marketplace.

At CoverME.gov, Maine people can compare private plans, apply for financial assistance, and enroll in a 2023 health plan. Health plans offered on CoverME.gov provide quality, comprehensive insurance that protects consumers if they have an accident or major illness and fully pays for preventive screenings for diseases such as cancer and diabetes. This year, more Maine people than ever can get financial help to afford their plans.

The Maine Department of Health and Human Services (DHHS) Office of the Health Insurance Marketplace (OHIM) will release biweekly updates on plan selections through CoverME.gov, Maine’s Health Insurance Marketplace.

Plan selections provide a snapshot of activity by new and returning consumers who have selected a plan for 2023. “Plan selections” become “enrollments” once consumers have paid their first monthly premium to begin insurance. These numbers are subject to change as consumers may modify or cancel plans after their initial selection.

The deadline to select a plan for coverage beginning January 1, 2023 is December 15, 2022. Consumers who select a plan after that date will have coverage beginning February 1, 2023.

CoverME.gov Activity Through December 24th, 2022

62,494 Mainers have selected plans for affordable health coverage in 2023

This includes 7,449 new consumers and 55,045 returning consumers.

The Maine Department of Health and Human Services (DHHS) Office of the Health Insurance Marketplace (OHIM) will release biweekly updates on plan selections through CoverME.gov, Maine’s Health Insurance Marketplace.

Plan selections provide a snapshot of activity by new and returning consumers who have selected a plan for 2023. “Plan selections” become “enrollments” once consumers have paid their first monthly premium to begin insurance. These numbers are subject to change as consumers may modify or cancel plans after their initial selection.

The deadline to select a plan for coverage beginning January 1, 2023 is December 15, 2022. Consumers who select a plan after that date will have coverage beginning February 1, 2023.

CoverME.gov Activity Through December 10th, 2022

59,032 Mainers have selected plans for affordable health coverage in 2023

This includes 3,834 new consumers and 56,098 returning consumers.