(note: I'm live updating as I type this stuff, so keep checking back, I'll be adding more updates/analysis over the next hour)

Wow! OK, I'm back from my kid's field trip (nature center; they learned about how animals handle the winter via hibernation, migration & adaptation...learned about fossils...went on the nature trail to look for animal tracks...and even dissected owl pellets, hooray!!). Of all the days to miss a major HHS/CMS conference call, this was a big one. I'm furiously poring over the HHS Dept's ASPE January Enrollment Report which, as I expected this morning, was just released less than two hours ago.

There's some sort of press conference call this afternoon with official updates on the 2016 Open Enrollment Period. Unfortunately, I have a field trip to attend with my kid all afternoon, and a client call after that, so I won't be able to get in on the call, nor will I be able to write anything up about whatever's discussed (or any press releases which come out after the call) until several hours later.

Since enrollments over the past two weeks have been virtually dead due to a) the January coverage deadline having passed for all states; b) Christmas week and c) New Year's week, my guess is that the major reasons for today's call will include:

Here's what I wrote last July, when Gallup released their 2015 Q2 Uninsured Rate survey (which pegged the uninsured rate among adults (over 18) at 11.4%:

Going forward, I'm actually not expecting the Q3 2015 Gallup survey to show much of a change; we're in the heart of the off-season, the #ACATaxTime additions have already been accounted for, and Montana is the only state which is expected to expand Medicaid anytime soon, so Q3 will probably hold steady at 11.4%, give or take; the rate might even inch up a few tenths of a percent due to attrition. Still, the overall picture is pretty dramatic: Whatever else you can say about the ACA in terms of cost, it's definitely accomplishing the other half of its goal: The total number of uninsured Americans has been cut by about 16 million people since October 2013.

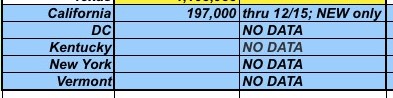

If you look at the State-By-State OE3 enrollment breakdown, you'll notice that there are still 4 blank fields all the way down at the bottom, plus a special note regarding California:

I launched the "State by State" chart feature towards the end of the 2015 Open Enrollment period last time around, and it proved to be pretty popular, so I've brought it back this year.

It's important to note that I'm still missing data from some state exchanges; I have bupkis from DC, Kentucky, New York or Vermont. I also only have partial data from others (California includes new enrollees only, while several other states only have data for the first couple of weeks).

With all those caveats out of the way, here's where things stand. Just like last year:

So what about this week? Well, it should play out very much the same: Practically all QHP selections going forward should be for new additions, and we have New Year's Eve and Day included. Sure enough, last year there were just 103K added to HC.gov from 12/27 - 01/02...slightly more than Christmas week.

Assuming this year follows a similar pattern, there should be roughly 80,000 people tacked onto the HC.gov total for Week 9, bringing the cumulative total up to just over 8.6 million.

If this does happen, then yes, I'll have to seriously re-evaluate my current 14.7 million OE3 projection...because that will suggest that the final 5 weeks are gonna play out a good 20% lower than my expectations.

And if that's the case, then instead of another 3.5 million new folks signing up, it'll only be around 2.8 million...bringing a grand total of right around 14.0 million even.

Ah. OK. Well, this time it's different, because this time, the Republican-controlled Senate has signed onto repealing the ACA as well, which means that it'll actually make it as far as President Obama's desk for once, requiring him to...pull out a pen and veto it.

...as Majority Leader Kevin McCarthy puts it, that’s the goal: “With this bill, we will force President Obama to show the American people where he stands.”

One of the many standard Republican talking points when it comes to healthcare is this old chestnut:

"Let insurance carriers sell their products across state lines!!"

I've never quite understood why this was supposed to be such a panacea, but I guess it's supposed to have something to do with "removing burdensome government regulations!" and "allowing the Invisibile Hand of the Free Market" to work it's wonders, bla bla bla. The idea is that the carriers have, until now, staked out their turf and aren't allowed to compete with each other outside of their home states; presumably, if they were allowed to do so, prices would drop accordingly due to competitive pricing, etc etc.

Long-time readers may have noticed that unlike private QHP enrollment, I've sort of given up on trying to track Medicaid expansion numbers at the state-level on the Medicaid Spreadsheet this year. Quite frankly, there's simply too much missing data and way too much "churn" in Medicaid for me to keep track of it at that granular level. Instead, I've just been looking at the Medicaid numbers from the national level, guided by CMS's monthly reports...but I've proven to be pretty accurate with my proejctions on those trends so far, so I'm not too concerned about it.

Starting Friday, low-income Montanans covered by Montana’s expanded Medicaid program can start using their coverage – and 20,000 people have already signed up.

Connect for Health Colorado® and Colorado Medicaid Report Enrollment Gains of More Than 169,000

January 5, 2016

DENVER — Between Nov.1 and Dec. 31, more than 169,000 Coloradans enrolled in health coverage for 2016, either in private health insurance purchased through the state health insurance Marketplace or in Medicaid, or Child Health Plan Plus (CHP+), according to new data released today by Connect for Health Colorado® and the Colorado Department of Health Care Policy and Financing.

“We are very happy with the enrollment growth during the first two months of this open enrollment period,” said Connect for Health Colorado® CEO Kevin Patterson. “But I want to urge everyone who does not have health insurance provided through their employer to act now to provide financial security for their families and to avoid a penalty of nearly $695 or more. The final deadline for 2016 coverage –Jan. 31 – is fast approaching.”