NJ Department of Banking and Insurance Releases Initial Health Insurance Rates for the Individual Market for Plan Year 2026

Federal Inaction on Enhanced Premium Tax Credits Among Issues Impacting Consumer Costs

TRENTON — The New Jersey Department of Banking and Insurance today announced that plan year 2026 health insurance initial rates have been submitted by insurance carriers operating in the individual market, which includes Get Covered New Jersey, the State’s Official Health Insurance Marketplace.

Plan year 2026 health and dental insurance rate filings, as proposed, are available for the companies listed below. These filings are subject to actuarial review. Additional companies will be listed as their filings are received. Any insurance filings already approved are available to the public through the NAIC’s System for Electronic Rate and Form Filing (SERFF) interface. There is no fee for using SERFF. Rate info can also be accessed at the Rate Review page at Healthcare.gov

AmeriHealth Caritas VIP Next, Inc:

Company Legal Name AmeriHealth Caritas VIP Next, Inc.

Market for which proposed rates apply (Individual or Small Group) Individual

Total proposed rate change (increase/decrease) 46.20% increase

Effective date of proposed rate change January 1, 2026

This actually came out a couple of weeks ago but ironically, I've been too swamped analyzing & posting 2026 rate filings for other states to get around to posting it here until now.

Overall preliminary rate changes via SERFF database, state insurance dept. website and/or the federal Rate Review database.

Hawaii Medical Service Association:

Our requested rates include only the amounts needed to cover the expected health care benefits of our members, the cost of administering their benefits, expected Affordable Care Act (ACA) fees, and a small charge to help manage the risk of offering benefits to this population.

We based our rate increase request on a review of past costs of benefits and other expenses. These historical costs are adjusted for trend, to account for expected changes in use of medical services, cost inflation, and other factors that affect the cost of care. We also adjusted costs for benefit changes, which were largely made to comply with government mandated plan designs. Administrative expenses have been relatively flat over the past couple of years.

Rate Watch is a convenient way for Hoosiers to access key data on Accident and Health rate filings submitted to the IDOI on or after May 1, 2010. Use it to determine which companies have requested rate changes, their originally requested overall % rate change, and the overall final % rate change approved. These are overall rate changes and are not individually specific. The table below is searchable and sortable. You can also download your filtered results by pressing the Save Excel File button at the bottom of the table. If you need the full data set, including a few additional columns, you can download the CSV file.

Vermont has around ~32,000 residents enrolled in ACA exchange plans, 93% of whom are currently subsidized. I estimate they also have another ~2,000 unsubsidized off-exchange enrollees.

Combined, that's ~35,000 people, although the official carrier rate filings claim it's more like 36,000 statewide.

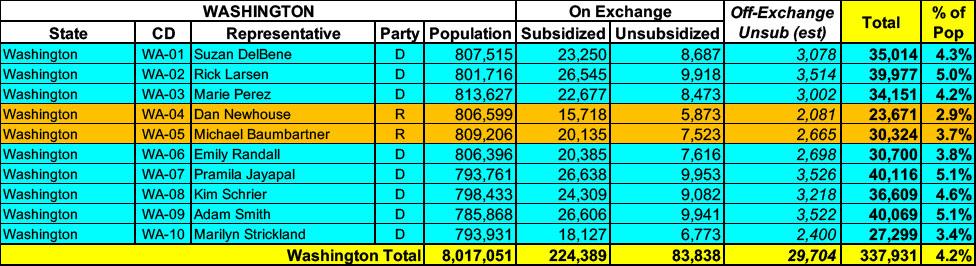

Washington State has around ~308,000 residents enrolled in ACA exchange plans, 73% of whom are currently subsidized. I estimate they also have another ~29,000 unsubsidized off-exchange enrollees.

Utah has around ~421,000 residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. I estimate they also have another ~17,000 unsubsidized off-exchange enrollees.

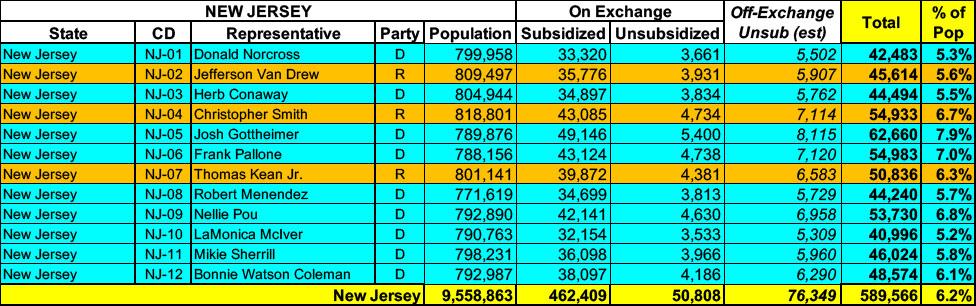

New Jersey has around ~513,000 residents enrolled in ACA exchange plans, 85% of whom are currently subsidized. I estimate they also have another ~76,000 unsubsidized off-exchange enrollees.

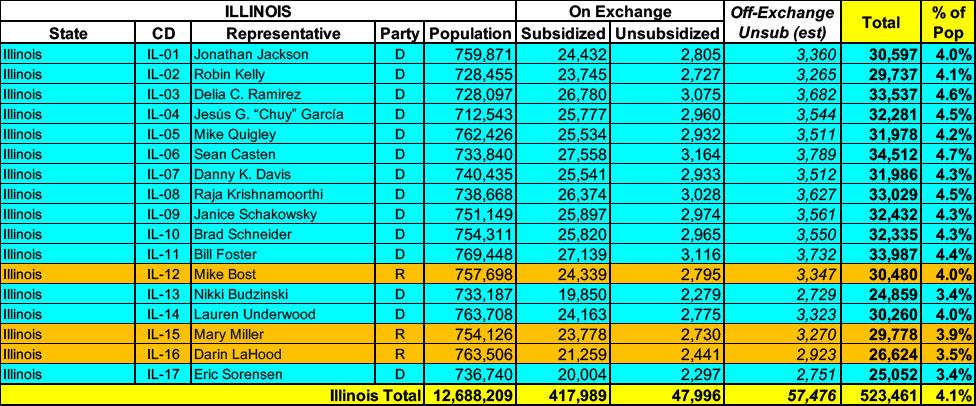

Illinois has around ~466,000 residents enrolled in ACA exchange plans, 90% of whom are currently subsidized. I estimate they also have another ~57,000 unsubsidized off-exchange enrollees.