Former Acting CMS Administrator Andy Slavitt and Huffington Post healthcare reporter Jeff Young have each written up a fairly comprehensive list of the various types of ACA/healthcare sabotage which the Trump Administration and/or other Republicans in Congress or at the state level have attempted (or are in the process of attempting today).

As I noted last week, the Republican-controlled Michigan state Senate rammed through a draconian work requirement bill for ACA Medicaid expansion enrollees in spite of the fact that it would serve no positive purpose and would only "save money" by kicking thousands of low-income Michiganders off their healthcare coverage while actually harming the economy.

I further noted that while I was pretty sure the bill would easily pass the state Senate (where the GOP holds a supermajority) and will likely pass the GOP-controlled state House as well, there is a decent chance that it could be vetoed by GOP Gov. Rick Snyder. Snyder is guilty of a long list of sins during his time as Governor, including being indirectly responsible for the water supply for the entire city of Flint being poisoned a few years back. At the same time, oddly, once in a blue moon he'll actually do something decent and good, and the one he deserves the most praise for on this front is pushing to get Medicaid expansion through in the first place.

WAIT, I MISSED THIS: The Trump Administration DIDN’T INCLUDE OFF-EXCHANGE ACA POLICIES in their 100K - 200K projection?? I heard something about it but assumed they were just pulling numbers out of their asses. This is actually worse in some ways. https://t.co/S2qJetjdTS

It's important to keep in mind that they knew damned well that killing the mandate penalty without replacing it with some other type of "negative inducement" to encourage people to enroll in a fully ACA-compliant policy was a really, really bad idea. Proof? Both the GOP House and Senate versions of their ACA "replacement" bill included an alternative to the mandate penalty:

Under the AHCA, the individual mandate is wiped out...except it's replaced with a 30% premium surcharge for people who don't maintain continuous coverage for more than 2 months.

(sigh) OK, gather 'round children, and let me tell you the story of how Cost Sharing Reductions went from being a thorn in the side of the Obama Administration to becoming a massive tree branch jammed into the kidney of Congressional Republicans. The following is an updated version of a lengthy post of mine from about six months ago.

The Cost Sharing Reduction (CSR) payment controversy has only really been sucking up a huge amount of political and policy oxygen for the past year and a half, since Donald Trump took office, but actually started long before then. Why? Because the whole reason the CSR payments were discontinued in the first place is a federal lawsuit filed by John Boehner on behalf of the House Republican Caucus back in 2014.

(sigh) Dammit, sure enough, as I expected, the full Michigan state Senate has gone ahead and passed the state Senator Mike Shirkey's "God's Safety Net" bill which would impose 29-hour-plus work requirements on 680,000 low-income Medicaid enrollees even though the vast majority of them already work, go to school, are medically fragile, take care of other medical fragile family members, elderly relatives or children and so forth. It was, as you'd expect, a party-line vote:

Able-bodied Medicaid recipients in Michigan may soon have to choose between finding a job or losing health insurance.

...Democrats condemned the proposal as harmful to thousands of Medicaid recipients who would not meet the several exemptions spelled out in SB 897 and said such a move is also illegal. Majority Republicans brushed aside those objections, and the bill passed 26-11.

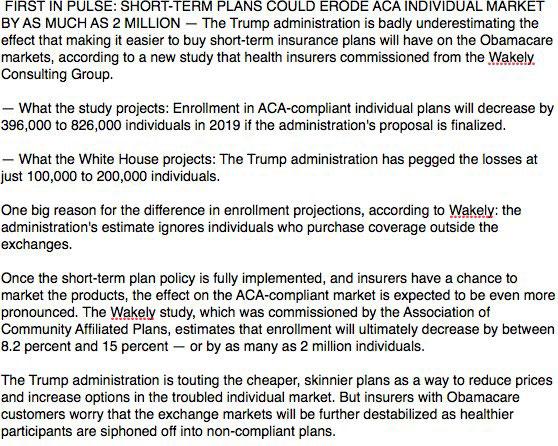

I've repeatedly written about how Donald Trump is still deperately trying to sabotage the ACA by any means necessary. Last year it was all about a combination of regulatory and legislative attacks, but aside from repealing the ACA's individual mandate (which was, admittedly, a pretty ugly blow), the GOP-held Congress was unsuccessful at tearing it down legislatively.

Therefore, for 2018, Trump has decided to double down on the regulatory side...and one of the main ways he hopes to achieve this is by opening up the floodgates on so-called "Short-Term, Limited Duration" policies, which aren't subject to most ACA requirements and therefore are a) free to siphon off healthy ACA-compliant enrollees into b) substandard healthcare plans which can leave thousands of people in dire straits.

Two more Democratic senators are introducing a bill that would create a version of Medicare for some working-age Americans, offering yet another sign that government-run insurance will figure prominently into the Democratic Party’s health care agenda going forward.

By my count, there are now a total of 5 different Universal Coverage policies officially on the table from Congressional Democrats, in addition to the two "ACA 2.0" bills proposed (both of which are presumably meant as stopgap measures until one of the UC bills can also get passed and take hold and be implemented a few years later). These bills include ones from Bernie Sanders ("Medicare for All"); Tim Kaine/Michael Bennet ("Medicare X"); Brian Schatz ("Medicaid Option"); and my preferred option of those I've seen so far, the plan from the Center for American Progress ("Medicare Extra"). The newest entry from Sen. Merkley & Murphy is apparently called "Medicare Part E":

Over at the Kaiser Family Foundation, Karen Pollitz and Gary Claxton have published a handy explainer which goes over the basics of the various types of NON-ACA individual market policies...specifically, the "Short Term" and "Association" plans which Donald Trump is attempting to flood the market with by essentially removing any restrictions or regulations on them, but also the "Idaho Style" plans which were rejected by HHS for being flat-out illegal as well as the "Farm Bureau" junk plans which Iowa recently decided to open the floodgates on (Tennessee already had a similar setup, and sure enough, it has proven pretty devastating to Tennessee's ACA market since 2014 as a result). The whole thing is worth a read, but in the early part of their explainer, however, they also happened to neatly lend support to my estimates from last week regarding the unsubsidized market:

...Maitre, 62, spends dozens of hours each week babysitting her grandchildren and providing their working parents with free child care. But none of that time or her community service would count as work under an advancing plan that would require Medicaid recipients to spend 29 hours a week at a job or risk losing their health care coverage.

...The Republican-led Senate Competitiveness Committee approved the legislation a short time later in a 4-1 vote. The lone committee Democrat voted against the plan to reform the government health care program for lower-income residents, which has grown significantly in recent years after the state expanded eligibility under former President Barack Obama’s signature health care law.

It now moves on to the full state Senate, as I expected.