I've writte a lot about the so-called "woodworker effect" with Medicaid expansion over the past 2 1/2 years: People who were already eligible for Medicaid before the ACA, but who never signed up for it for a variety of reasons (they didn't know they qualified; didn't know the process for signing up; were too embarrassed to do so; etc etc). I estimated about 3 million "woodworker" enrollees in 2014, although I downshifted that later on and now have the tally estimated at around 3.8 million nationally as of the end of 2015. That's a lot of people being added to the system who would have been eligible for Medicaid even if the ACA had never been passed.

Last week, a major report from the National Bureau of Economic Research confirmed what I've been saying all along (although their estimates are somewhat lower--around 2 million in 2014 plus an unknown number for 2015), which was written about in a feature story by Kimberly Leonard of U.S. News & World Report.

I haven't written much about West Virginia, and the last time I addressed their Medicaid expansion data was way back in September 2014, when they hit around 150,000 enrollees...or 100% of the total number thought to be eligible for the program.

Either those estimates were off, or the economic situation has changed over the past year or two. It's also conceivable that the state has deliberately nudged some "traditional" Medicaid enrollees over to "expansion" status in order to save money (remember, the federal government only pays 74% of the cost of "traditional" Medicaid, but 100% of expansion, though this gradually drops to 90% over the next few years).

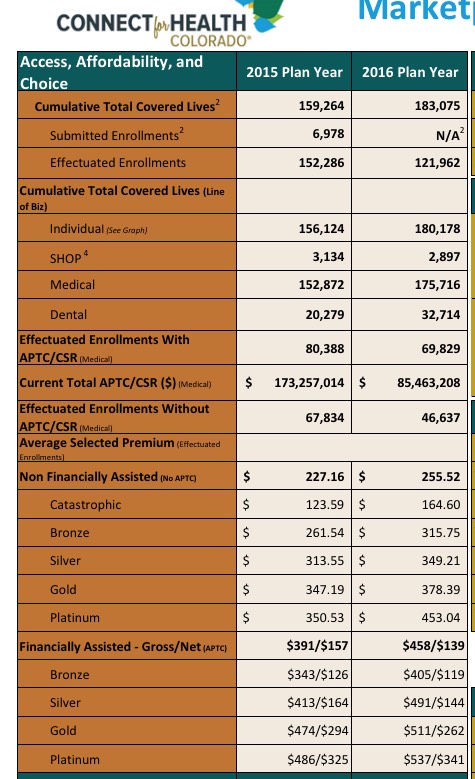

Last month I noted that, assuming I was reading Connect for Health Colorado's monthly dashboard report correctly, they were down to 115,890 effectuated exchange enrollees as of 3/31/16, or a whopping 23.1% lower than the official APTC report tally of 150,769 QHP selections as of the end of Open Enrollment.

Over the weekend, they released their April dashboard report, and the numbers are actually up slightly...which means that while the net drop compared to the OE3 number is still steep, it's also spread out over a 3 month period instead of 2:

As I noted at the time, normally, all 90 panels are chosen by a NN committee, but this year they decided to leave 10 slots open to “public voting”, allowing anyone to create a NN account, log in and vote daily for their favorite panel.

Throughout last September and October, I chronicled the dominos-like downfall of a dozen ACA-created Co-Op insurance carriers. They tumbled, one by one, as a result of a perfect storm of problems, some of which dated back to the final version of the ACA which was signed into law; others which cropped up along the way:

Conrad's plan called for $10 billion of government grants distributed among nonprofit, member-owned health insurance startups. The money came with few restrictions. Competing against big for-profit insurers is difficult, Conrad said. The co-ops needed as much freedom as possible to ensure their survival.

Republican lawmakers maneuver to force a vote on KidsCare, reviving a debate over the role of government in people's lives vs. personal responsibility

Chastened and angry over their failure to reinstate KidsCare, Republican lawmakers in the Arizona House got Democrats to join them Thursday in a successful bid to revive the children’s health-insurance program.

May 15 officially marked the start of the 2016 rate review season. What that means for Americans is that over the next month or so, newspapers and web sites across the country will start running stories with scary-sounding headlines like this:

Some Oregonians could face major insurance rate hikes next year

Health plans request double-digit premium increases

… or, more reassuringly, like this:

Lower rate increases, more plans proposed for state’s health exchange in 2016

The articles will throw a bunch of numbers around, saying that the “average” premium rate increase for a given state is expected to be X percent, followed by examples of the highest and lowest increases. There may even be a few “Company Y will actually be reducing their rates!” thrown in.

Before you freak out, there are a few important things to look for.

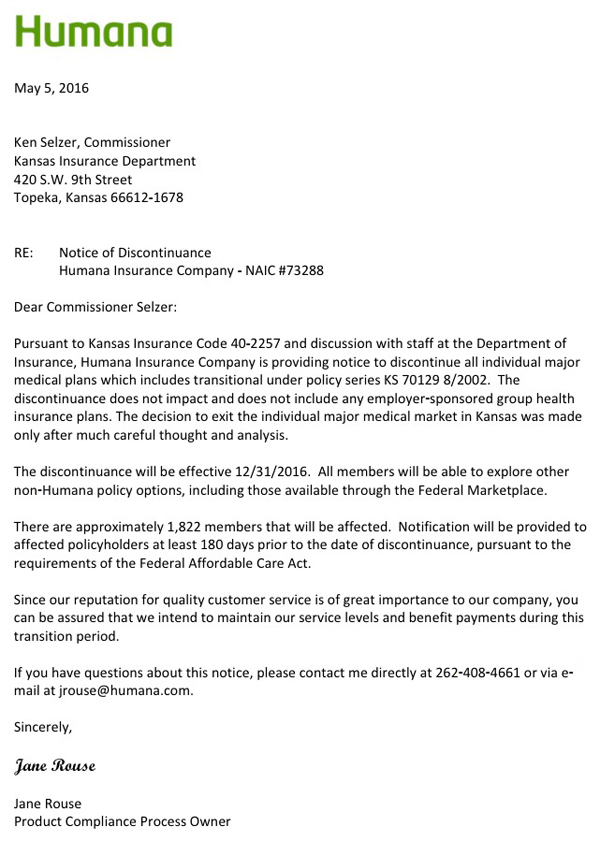

This is really just a summary of my last 4 posts. I've combed through the SERFF databases for every state which uses the system for rate filings, and while very few have the actual 2017 rate filing requests listed yet, at least 4 of them have official individual market exit letters submitted for 2017 from Jane Rouse, the Product Compliance Process Owner for Humana Insurance Co:

This list may grow as additional state filing data and/or press releases come out from Humana, but assuming these are the only 4 states Humana is bailing on, the news isn't quite as bad as it appears at first.

To be clear, I'm not saying this is a good development; when you combine it with the recent UnitedHealthcare Dropout Odometer it's more of a drip-drip-drip sort of thing. But it isn't disasterous for the exchanges either (at least not yet).

UPDATE: I've been informed by a reliable source that Humana is also dropping out of the individual market in Nevada next year, although I don't have any actual enrollment data there. Humana is not currently participating on the Nevada exchange, however, so any dropped enrollments would be OFF-exchange only. In fact, I'm pretty sure that the only individual market enrollees Humana has in Nevada are grandfathered policies anyway, so the numbers should be pretty nominal there.

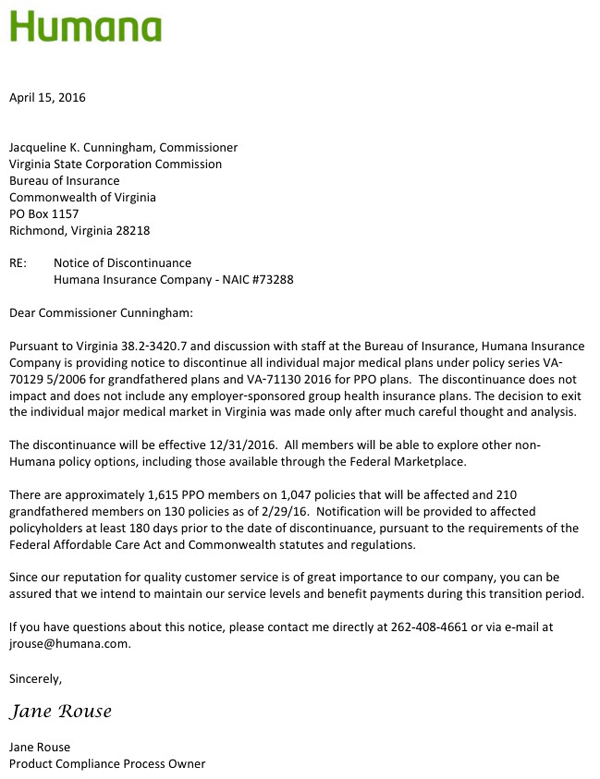

Yep, sure enough, Humana is following UnitedHealthcare out the door of multiple states next year. That's 1,800 people impacted, although they're all OFF-exchange only:

It's also worth noting that "grandfathered" enrollees only make up around 11% of Humana's total Virginia individual market as of this spring, which is somewhat higher than my overall ballpark estimate of around 1 million nationally.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}