Thanks to commenter "Junaed S" who directed me towards this simple, cut 'n dry PDF from the Connecticut Dept. of Insurance detailing the requested rate hikes for the CT individual and small group markets for 2017:

In addition, Anthem has decided not to offer its PPO (Preferred Provider Organization) individual plans in 2017. In all, the Colorado Division of Insurance said Monday around 92,000 people with individual plans from Anthem, UnitedHealth, Humana, and Rocky Mountain Health Plans will have to find other coverage during open enrollment in the fall.

Last month I noted that the Washington Healthplanfinder was reportingcurrently effectuated QHP enrollment at 170,527 as of the end of March, a 15.0% drop from the official number of QHP selections during the 2016 Open Enrollment Period. I also noted that due to some confusion about how the numbers are reported by the exchange, it could also be argued that WA has seen just a 6.6% net drop, depending on how you look at it.

However, since 200,691 is the official number included in the ASPE report, I'm finally letting that one go...and actually, that's OK, because a 15% drop by 3/31 is fairly close to what I would expect anyway (a bit higher than the 13% national drop from last year, but not out of line).

Anyway, the WA exchange just released their May report (with data through the end of April), and it's actually pretty good--there's only been a very slight net drop since March, for an overall drop of just 15.2% from the 200K figure:

A simmering dispute over the risk corridor program has broken into the presidential campaign, with Senator Rubio crowing that an arcane budget move has “kill[ed] Obamacare” and “saved the American taxpayer $2.5 billion.” On account of that move, health plans are set to receive only pennies on the dollar from the risk corridor program, which was supposed to cushion them from big losses.

...The administration has vaguely said that it will “use other sources of funding for the risk corridors payments, subject to the availability of appropriations.” But the budget bill limits the administration’s power to dip into other funds, and a Republican-controlled Congress isn’t likely to appropriate money for a program that’s been decried as an insurer bailout.

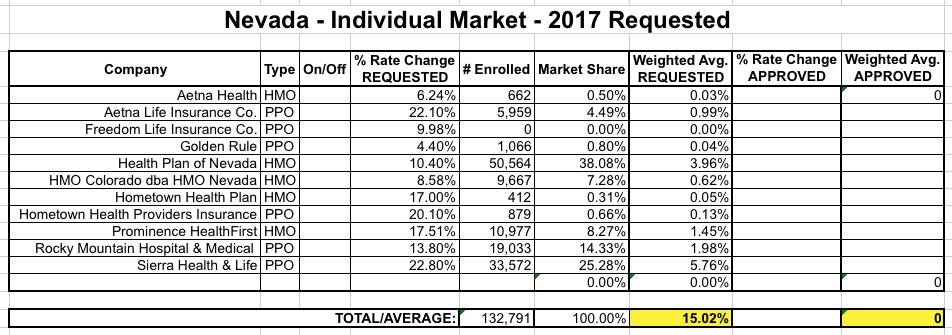

Can I first say that I absolutely love the way Nevada's rate filing database is set up, especially their (apparently proprietary and mandatory) filing format system?

Unlike the standard SERFF database, which is comprehensive but also can be confusing as hell, Nevada's system is simple, clean, easy to navigate and, most of all, every single carrier filing listed displays the number of current enrollees clearly.This is a huge pet peeve of mine, which is understandable given what I'm trying to do here!

OK, that said, here's what things look like in the Silver State:

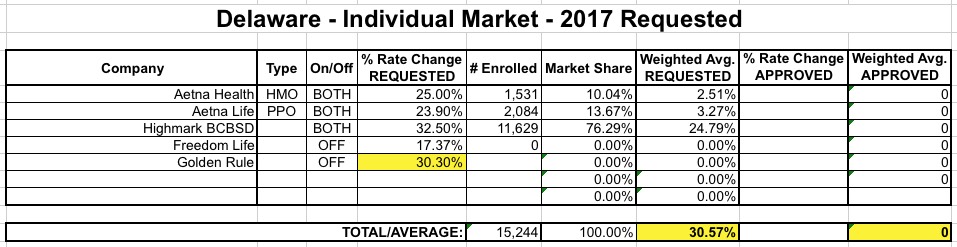

Delaware is a small state, and only has a total of 4 carriers offering individual polcies (2 on exchange, 2 off). One of those, however, is once again "Freedom Life" which, once again, is asking for precisely a 17.37% rate hike on their almost-certain-to-be-nonexistent enrollees. So...never mind them. That leaves Aetna (split into HMOs and PPOs) and Highmark BCBS offering policies on the exchange, and Golden Rule off the exchange.

Unfortunately, I can't find Golden Rule's actual current enrollment number, but as you can see below, it really doesn't matter:

As you can see, no matter how many enrollees Golden Rule has, their 30.3% average hike request is very close to the 30.6% average of the other carriers. The very most it could do is nudge the weighted average down by a tenth of a point or two, so let's call it 30.5%.

On Wednesday I noted that a whopping 175,000 Louisianans had somehow managed to enroll in the state's just-launched Medicaid expansion program within less than 12 hours of the floodgates being opened up. This was even more amazing when you consider that number represents 47% of the total people estimated to be eligible for the program state-wide (375K).

Now, obviously there's no way that 16,000 people per hour were individually visiting HealthCare.Gov or their local state health agency; on it's busiest day (December 15, 2015), HealthCare.Gov was averaging 25K/hour...but that was across 38 states, many of which are much larger than Louisiana. Instead, I assumed that LA had done something similar to Oregon/West Virginia's "fast-track" programs, where they use existing food stamp/welfare databases to automatically enroll people, not "officially" pulling the trigger until after the stroke of midnight.

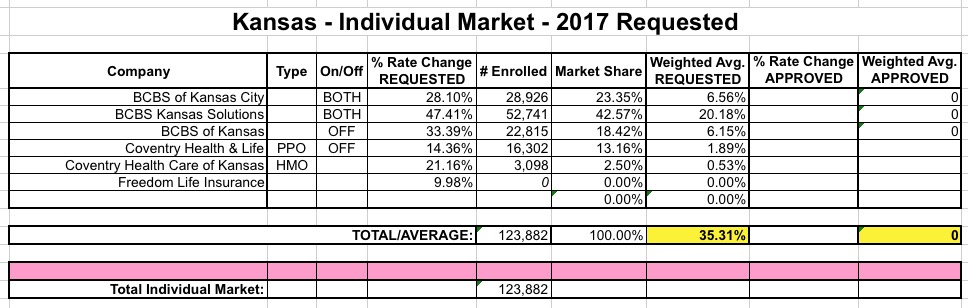

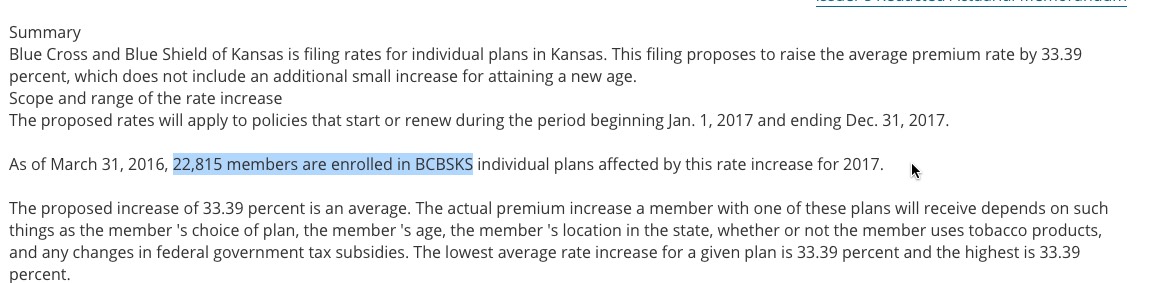

The good news about Kansas is that 5 of the 6 carriers which have submitted 2017 individual market rate filings included their current enrollment totals in a clear, easy to see format...and the 6th one is (once again) "Freedom Life" which, judging by the dozen other states they've popped up in, almost certainly has only 1 or 2 enrollees (or none at all) anyway.

The bad news is...well, the requested rate hikes are pretty ugly: About 35.3% on weighted average.

Also, is it really necessary for Blue Cross Blue Shield to operate under three nearly-identical names? Really?

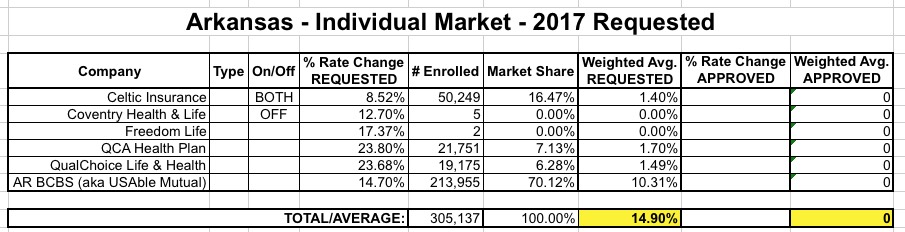

Arkansas was a little weird...while the rate filings for 5 carriers are listed over at RateReview.HealthCare.Gov, the carrier with the largest individual market share in the state, BCBS (aka "USAble Mutual") is nowhere to be seen (there's a sm. group listing for them, but not individual). However, when I went directly to the AR SERFF database, there they were--and it's listed specifically as "2017 Individual QHP Rates", so there's no question here about whether they plan on offering ACA-compliant policies in 2017.

Anyway, between the HC.gov site and the SERFF site I was able to cobble together pretty much all of Arkansas' indy market. The numbers seem about right; AR's indy market was around 303K in 2014; while it's likely up to 375K or so today, the "missing" 70K can easily be attributed to UnitedHealthcare dropping out and/or grandfathered/transitional enrollees.

At 14.9% on average, this is actually good news for 2017, relatively speaking.

Oklahoma's entire individual market (including grandfathered/transitional plans) was around 172,000 people in 2014. Assuming it's grown roughly 25% (in line with the national increase), it should be up to perhaps 215,000 people by today, of which perhaps 195K are ACA-compliant.

This is significant because there appear to be only 3 carriers offering individual policies in Oklahoma next year...one of which is the infamous "Freedom Life Insurance Co." which I wrote about last night. Since Freedom Life has (as usual) only a single enrollee in the state, it's really a nonfactor for calculating the weighted rate hike average.

That leaves Blue Cross Blue Shield of Oklahoma, which has a whopping 170,000 enrollees...and CommunityCare (which is in turn broken into HMO and PPO divisions)...unfortunately, their rate filing doesn't include their enrollment number; all it says is that it's "too small to be credible" to be used as the basis of their rate hike request. In addition, UnitedHealthcare is dropping out of the OK indy market; I don't know how many enrollees they actually have.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}