A year ago, rate filings caused widespread anxiety, as multiple carriers announced withdrawals from the ACA market, and state officials struggled to fill bare counties. Many of those remaining filed enormous rate increases. In 2018, marketplace enrollment was stable, while unsubsidized enrollment continued its multi-year decline. So far, this year’s rate filing season has been sprinkled with news of entry and expansion, and proposed rate hikes that are generally more moderate. With no announced market exits thus far, it seems likely that in 2019 there will be net entry into the ACA marketplace.

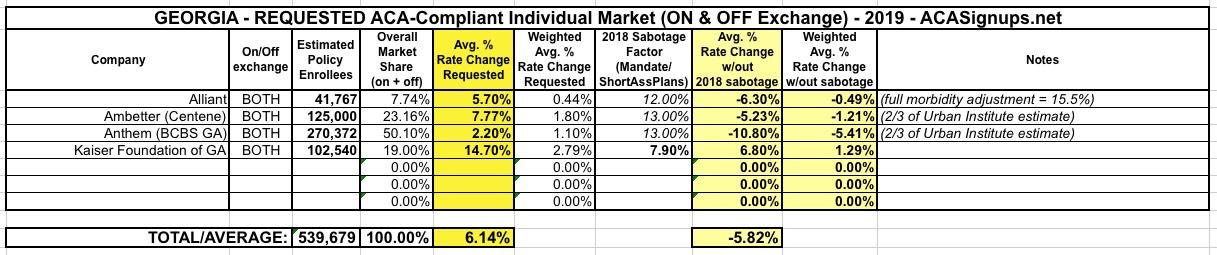

Whew! Georgia only has 4 carriers participating in the individual market, but tracking down some of the data was a royal pain in the butt, especially Ambetter/Centene, which not only buried the numbers I needed inside a whopping 1,900-page PDF file, but the actual average requested rate increase wasn't even included; for that I had to check a different file. Yeesh.

The good news is that carriers in Georgia are only requesting around a 6.1% average rate increase for ACA-compliant individual market policies next year.

The bad news is that if it weren't for the ACA's individual mandate being repealed and the Trump Administration's expansion of #ShortAssPlans, 2019 premiums would likely be dropping by around 5.8% instead.

For nearly a year, healthcare wonks like myself, David Anderson, Andrew Sprung and Louise Norris have been heavily getting the word out to promote not just the "Silver Loading" CSR-load workaround, but an even more clever variant which I've coined "the Silver Switcharoo" which takes the concept of Silver Loading and goes one step further.

*(OK, these are technically only "semi-approved" rates...there could still be some additional tweaks later on after public comment, etc.)

Oregon was the fourth state which I ran a preliminary 2019 rate increase analysis on back in May. At the time, I concluded that insurance carriers were requesting a weighted average increase of 10.5% for ACA-compliant individual market policies next year. I knew that Oregon's state-based Reinsurance program was helping keep that average down to some degree, but I didn't know exactly how much of a factor it was.

I also knew that efforts to sabotage the ACA by Donald Trump and Congressional Republicans would play a major role in increasing 2019 rates: Repeal of the individual mandate is a big factor, along with the unnecessary 1-point increase in the state exchange fee being imposed on Oregon and the other four states which run their own exchange but "piggyback" on HealthCare.Gov's technology platform.

This article from KTVQ is excellent for my purposes. It clearly and cleanly plugs in just about all of the hard numbers I need to run my rate hike analysis: Which carriers are participating in the 2019 ACA individual market; how many current enrollees each carrier has (both on and off the exchange); and the exact average increase each one is requesting for next year!

Health insurers selling individual policies on the “Obamacare” marketplace in Montana are proposing only modest increases for 2019, on average – or, no increase at all.

State Insurance Commissioner Matt Rosendale released the proposed rates Thursday, with Blue Cross and Blue Shield of Montana proposing an average increase of zero – and a 4.9 percent decline for small-group policies.

The other two companies selling policies on the online marketplace, PacificSource and the Montana Health Co-op, proposed average increases of 6.2 percent and 10.6 percent for individual policies, respectively, and lesser increases for small-group policies.

For weeks now, I've been painstakingly analyzing and plugging in the preliminary 2019 rate change data for ACA-compliant individual market as each state submits their filings. As of today, I've compiled data for 18 states (+DC), comprising perhaps 40% of the total ACA individual market, give or take. The table below shows where things stand at the moment.

Those yellow and manilla cells at the bottom are not a typo: To the best of my estimates so far, the insurance carriers across these 19 markets are asking for average 2019 unsubsidized premium rate increases of around 10-11%...however, as far as I can tell, they would be keeping rates FLAT year over year (on average), for the first time since the ACA launched, if not for three sabotage efforts by Donald Trump and Congressional Republicans: Repeal of the ACA's individual mandate, and Trump's removal of restrictions on non-ACA compliant "Short-Term, Limited Duration" and "Association" plans, which I've shorthanded as simply #ShortAssPlans....and in fact would actually be dropping in quite a few states (or, in the case of Minnesota, dropping more than they already are set to with those factors):

Florida is the 3rd largest state in the country, but has nearly the same number of ACA-compliant individual health insurance policy enrollees as California (around 2.0 million people if you subtract out grandfathered and transitional enrollees, vs. California's 2.1 million) even though Florida's total population is only 53% of California's (about 20.9 million vs. 39.5 million). Put another way, nearly 13% of Florida's non-elderly population is enrolled in the individual market, which is about twice as high as the natoinal average.

Add to this the fact that Florida is also the largest swing state politically, and people will be watching Florida's ACA exchange/premium situation very closely this fall.

Kentucky's 2019 preliminary Rate Filings have been posted, and they're pretty straightforward: Like this year, there will only be two carriers offering policies on the KY individual market in 2019: Anthem and CareSource, with roughly a 46/54 market share split.

The overall average requested rate increase is around 12.2% between the two. Neither carrier states just how much of their requested increase is due to mandate repeal or #ShortAssPlans (CareSource did list it...but then redacted it from public view). The Urban Institute projected around an 18.7 percentage point impact; 2/3 of that is around 12.5 points, so that's what I'm assuming until further notice.

Assuming that's accurate, that means that if not for the mandate/shortassplan sabotage factors, Kentucky carriers would be keeping unsubsidized 2019 premiums flat year over year (or even dropping them a smidge).

The Affordable Care Act (ACA) requires that every state have an exchange where consumers can buy individual health insurance policies. In Ohio, the federal government runs the health insurance exchange. Ohioans who do not have health insurance through their employer, Medicare or Medicaid may be eligible to purchase coverage through the exchange. Open enrollment for coverage next year (2019) begins November 1, 2018. Below is preliminary data based on the filings submissions of insurers in Ohio. Once filings are approved in late summer/early fall, final information will be posted.

Ohio’s Health Insurance Market (2018–2019)

In 2018, 8 companies sold health insurance products on the exchange in Ohio and 42 counties had just one insurer with an additional 20 counties having only two.