Moments ago, Covered California, the nation's largest state-based ACA exchange, released data via a media teleconference regarding the 2020 Open Enrollment Period.

In addition to being the largest ACA exchange after HealthCare.Gov, this info from Covered California is especially significant for the 2020 OEP due to their newly expanded/enhanced premium subsidies.

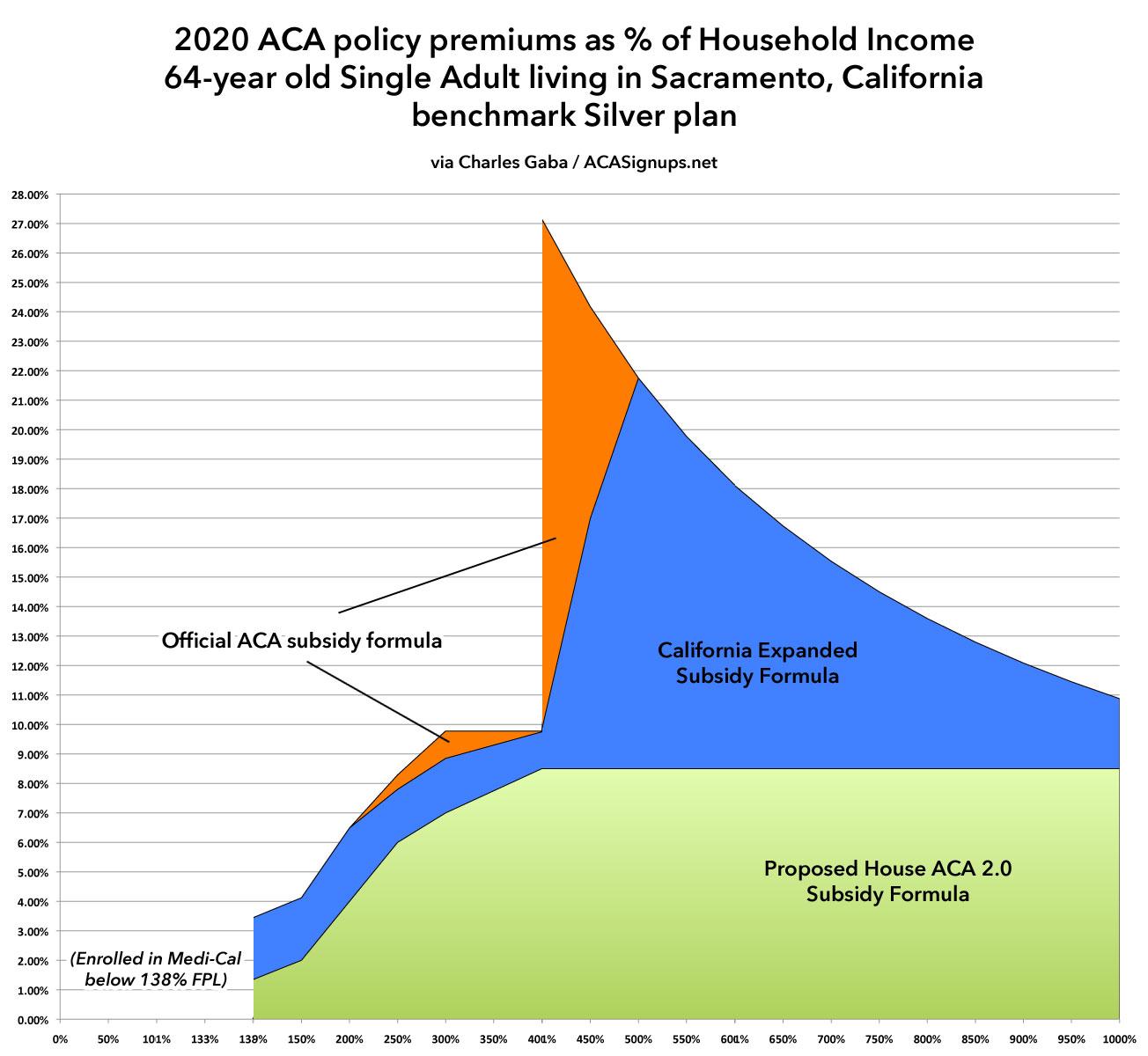

To recap: Under the ACA, financial subsidies are available to exchange enrollees earning between 100-400% of the Federal Poverty Level (FPL). That's between around $12,500 - $50,000/yr if you're a single adult, or between $25,000 - $100,000/yr for a family of four. Under the standard ACA formula, enrollees in that income range have their premiums capped at no more than around 2.0 - 9.8% of their income, on a sliding scale.

Unfortunately, this means that people earning more than 400% FPL are eligible for no financial assistance at all, a sudden drop-off known as the Subsidy Cliff.

Covered California and the Challenged Athletes Foundation Team Up to Promote Open Enrollment and the Dec. 15 Deadline for Coverage During All of 2020

While Covered California’s Open Enrollment period runs through Jan. 31, 2020, consumers must enroll by the end of Dec. 15 to have their coverage begin on Jan. 1.

Covered California is teaming up with the Challenged Athletes Foundation, to host a Holiday Boot Camp to promote the importance of health, fitness and the open enrollment period.

The Boot Camp will be led by Paralympian, 2019 Parapan Gold Medalist and World Record Holder Scout Bassett and Nike Master Trainer Betina Gozo.

Californians who choose to go without coverage could face a penalty when they file their 2020 taxes.

Covered California continued its statewide open enrollment campaign by teaming up with the Challenged Athletes Foundation in San Diego for its Holiday Boot Camp on Tuesday. The event comes as Covered California alerts consumers about a critical upcoming deadline. Consumers must sign up by Dec. 15 if they want their coverage to start on Jan. 1.

A few weeks ago, I did a write-up about a concerning development at HealthCare.Gov: The growing push under the Trump Administration to not only partner with 3rd-party web brokers (which has been done since the first days of the ACA under the Obama Administration), but to actively promote those third-party brokers over HealthCare.Gov itself.

In and of itself, this wouldn't be too problematic as long as people are still ultimately enrolling in fully ACA-compliant policies and receiving ACA subsidies if they're eligible for them. Hell, one of these 3rd-party authorized web brokers even has a banner ad at the top of my website...which I only allow because this particular one only sells on-exchange ACA-compliant policies.

I have a different California-specific post coming later this afternoon, but I stumbled across a mildly interesting bit of data and figured this would be a good time to share it while I wait to be able to post that one.

As you may recall, while the ACA required that most individual market major medical healthcare policies sold have to comply with full ACA regulations, there were some exceptions to this. The biggest exception made was for major medical plans which had been continuously enrolled in since before the ACA was signed into law in March 2010.

These plans were grandfathered in, and so are appropriately called "Grandfathered Plans", and applied to perhaps 5 million people or so back in 2014, when ACA-compliance became mandatory for newly-sold policies.

IMPORTANT: As I've noted before, Covered California has arranged to expand and enhance their ACA premium subsidies beyond the official ACA formula starting with the 2020 Open Enrollment Period. Back in October, I posted a detailed analysis, complete with tables and graphs to explain just how much hundreds of thousands of Californians could save under the new, beefed-up subsidy structure.

However, Anthony Wright of Health Access California just called my attention to the fact that I made a major mistake in my analysis which impacted every one of the examples: I was basing them on the draft enhanced subsidy formula from back in May instead of the final version, which is considerably more generous at the upper end of the sliding scale than the draft version was!

In short:

The ACA formula caps premiums (for the benchmark Silver plan) at between 2 - 9.8% of household income but only if you earn between 100 - 400% of the Federal Poverty Level.

The draft California formula is a bit more generous from 100 - 400% FPL and also caps premiums between 9.9 - 25% of income between 400 - 600% FPL.

The final California formula is more generous yet: It's pretty much the same up to 400% FPL, but caps premiums between 9.8 - 18% of income between 400 - 600% FPL.

I've therefore gone back and re-calculated and re-written the entire blog post below with the updated, corrected subsidy formula. My apologies for the error!

----------

There's two important points for CA residents to keep in mind starting this Open Enrollment Period:

First: The individual mandate penalty has been reinstated for CA residents. If you don't have qualifying coverage or receive an exemption, you'll have to pay a financial penalty when you file your taxes in 2021, and...

Second: California has expanded and enhanced financial subsidies for ACA exchange enrollees:

Until now, only CoveredCA enrollees earning 138-400% of the Federal Poverty Line were eligible for ACA financial assistance. Starting in 2020, however, enrollees earning 400-600% FPL may be eligible as well (around $50K - $75K/year if you're single, or $100K - $150K for a family of four). In addition, those earning 200-400% FPL will see their ACA subsidies enhanced a bit.

I've made quite a bit of fuss about California expanding availability of ACA financial subsidies to those earning 400 - 600% of the Federal Poverty Line ($75K for a single person, $154K for a family of four). The subsidies aren't massive for most people, but for hundreds of thousands of Californians--especially older folks earning between 400 - 450% FPL--this is a huge savings. In addition, they're sweetening the subsidies somewhat for those already receiving ACA tax credits.

The only real concern I had about this is whether enough people in California know about it. Just like with reinstating the mandate penalty (which California has also done this year), expanding & enhancing ACA subsidies isn't gonna cause a spike in enrollment if no one knows they're available. A lot of people who might have checked into it in prior years isn't likely to bother taking another look if they don't know that the income cut-off threshold has gone up, and many others have never bothered trying in the first place because they "heard somewhere" that they won't qualify.

This press release came out last week but I covered all the other state-based exchange Open Enrollment press releases so I figured I should include this one as well:

Covered California for Small Business Announces Expanded Choices and an Average Rate Change of 4.1 Percent for 2020

I'm not sure how this slipped by me, but in addition to Covered California already having launched their 2020 Open Enrollment Period yesterday, five other state-based ACA exchanges are already partly open as well. That is, you can shop around, compare prices on next year's health insurance policies and check and see what sort of financial assistance you may be eligible for:

I'm not sure when the other 7 state-based exchanges will launch their 2020 window shopping tools, nor do I know when HealthCare.Gov's window shopping will be open for the other 38 states, although I believe they usually do so about a week ahead of the official November 1st Open Enrollment Period launch date.

I also noted that there's two important points for CA residents to keep in mind starting this Open Enrollment Period:

First: The individual mandate penalty has been reinstated for CA residents. If you don't have qualifying coverage or receive an exemption, you'll have to pay a financial penalty when you file your taxes in 2021, and...

Second: California has expanded and enhanced financial subsidies for ACA exchange enrollees:

Until now, only CoveredCA enrollees earning 138-400% of the Federal Poverty Line were eligible for ACA financial assistance. Starting in 2020, however, enrollees earning 400-600% FPL may be eligible as well (around $50K - $75K/year if you're single, or $100K - $150K for a family of four). In addition, those earning 200-400% FPL will see their ACA subsidies enhanced a bit.

While the 2020 Open Enrollment Period doesn't officially start until November 1st across the rest of the country, in California it begins two weeks earlier, for whatever reason:

In most states, open enrollment for 2020 coverage will run from November 1, 2019 to December 15, 2019. But California enacted legislation (A.B.156) in late 2017 that codifies a three-month open enrollment period going forward — California will not be switching to the November 1 – December 15 open enrollment window that other states are using.

Instead, California’s open enrollment period (both on- and off-exchange) will begin each year on October 15, and will continue until January 15. Under the terms of the legislation, coverage purchased between October 15 and December 15 will be effective January 1 of the coming year, while coverage purchased between December 16 and January 15 will be effective February 1.

{kind=link}