According to the last official HHS enrollment report from back in May, as of April 19, 2014, Washington State had enrolled 163,207 people in private policies via their ACA exchange. Of those, 8,310 people never actually had their coverage start due to non-payment (WA requires payment of the first month's premium as part of the enrollment process, so I'm not sure what happened in these cases, but presumably there was some sort of credit card account approval glitch, insufficient funds in debit card accounts and/or the like).

In any event, that means the actual paid tally as of 4/19 was 154,897, or 95%, which is pretty darned good.

Well, a couple of days ago the WA exchange issued a press release regarding the renewal process for 2015, and included 2 key data nuggets. First up:

Just received the following email from a Kentucky resident. With his permission, I'm leaving out his name but am presenting it verbatim otherwise, with no further comment:

Thanks for discrediting good ol' Mitch. What a joke. I am a resident of Kentucky and here's how the ACA impacts my family with other opinions included for good measure.

We have read and heard the partisan battle waged for and against the Affordable Care Act (ACA). Much has been written and said, but I live it. I experience it. But to truly evaluate it requires good old-fashioned common sense. For some reason, this has gone the way of bipartisan politics.

Since I am a consultant paid on a per hour basis, I do not receive nor do I expect to receive health benefits through my employer. We purchased our health plan through the Kentucky Health Exchange – KYNECT: a marketplace to purchase health plans created via the ACA. We chose a silver plan.

For starters, returning customers will have to use the old, 78-screen application. New customers can use a simpler, faster, and more streamlined 16-screen version.

Health and Human Services officials said the site will automatically fill in existing consumers' information, such as their address and income, to help speed them through the process even though they have to use a more cumbersome application. That makes sense, as long as consumers take the time to change pre-populated information that has become outdated.

Boy, this syndrome of Republicans seemingly forgetting that repealing Obamacare would mean that hundreds of thousands of the very people they're hoping will vote for them would have their shiny new healthcare coverage torn away from them seems to be spreading fast. I'm calling it "repealnesia".

Yeah, I did a takedown of Mitch McConnell last night which gained some traction. However, that was more of a rant. Today, let's take a look at just how many times he flat-out lied about the Affordable Care Act (aka "Obamacare", aka "kynect"), shall we?

The yellow highlights are lies by McConnell. The orange highlights are either questionable/confusing statements by either him or the moderator, or otherwise just noteworthy:

(Moderator Bill) Goodman: has Obamacare and kynect been a boon or a bane for Kentuckians? Senator?

Mcconnell: Kentucky kynect is a website1. It was paid for by a $200 million and some-odd grant from the federal government. The website can continue. But in my view, the best interest of the country would be achieved by pulling out Obamacare root & branch and let me tell you why.

I'm pleased to announce that as ACASignups.net enters its' second year in operation, I've also started writing occasional pieces for healthinsurance.org:

Since 1994, healthinsurance.org has been a guide for consumers seeking straightforward explanations about the workings of individual health insurance– also known as medical insurance – and help finding affordable coverage.

The topic of insurance can be confusing, but we’re here with more information than ever: educational articles, expert health policy analysis, frequently asked questions about reform, a health insurance glossary, and guides to the health marketplaces and other insurance resources in each state.

I can't think of another publication outside of this one where what I do here is more appropriate. Looking at the list of other contributors, I'm honored to join their company.

My debut contribution to healthinsurance.org is an update regarding the citizenship/immigration data situation for Covered California enrollees...and the implications it may have for the rest of the country. Please take a look!

In addition to running ACASignups.net, I also happen to be a website developer by trade. I founded my website development company 15 years ago, which makes me an old man in the industry.

Given both of these capacities, I think I'm in a pretty good position to judge what's "just a website" and what isn't.

The kynect "just a website" wouldn't exist without Barack "Yeah, He's Black And He's The President Of The United States, It's Been 5 1/2 Years So Get Over It Already" Obama and the Democratic Party.

Those are two of the findings of a survey released today by the Center for Outcomes Research & Education at Providence Health Services. The goals were to understand who enrolled, assess their connection to care before and after enrollment and to understand their health. At the time of the study, 76,569 Oregonians had signed up through open enrollment.

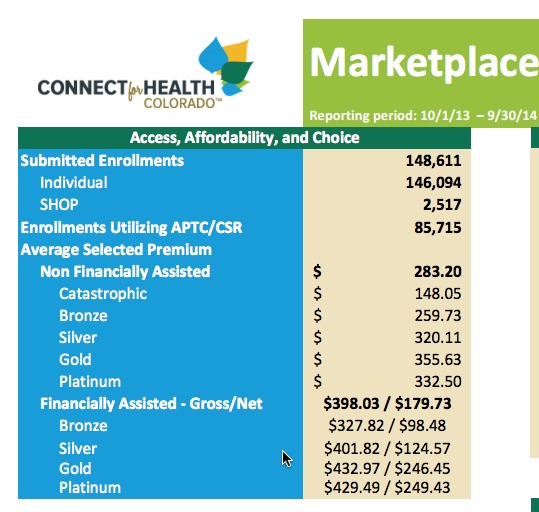

Colorado's official monthly metrics report is out, and shows that while off-season QHP additions have started to drop off as we approach the 2nd Open Enrollment period, they're still within my estimated range of 20-25% of the on-season rate.

Meanwhile, SHOP enrollments have inched above the 2,500 mark to sit at 2,517 covered lives as of the end of September.