And there you have it: As I've been expecting all week, not only has the MA Health Connector broken the 100K milestone, they blew past it, with 108,051 private policy selections as of last night (the Medicaid number is still hovering just below 200K, but that doesn't include yesterday; they should have easily tacked on another 5,000 to put MassHealth over the top).

In addition, the overall payment rate continues to climb, reaching 76%...but likely much higher when you consider that about many of the 108,000 total aren't scheduled to have their policies kick in until February anyway. I know that at least 50K of those who paid were for January-start policies, so it could easily be something like: 50K paid / 57K (January) + 32.2K paid / 51K (February), which would mean 88% of the January enrollees are paid up + 63% of the February enrollees so far. The larger point is that we won't know the real payment rate until late March (over a month after the enrollment period itself ends), so there's nothing to worry about for now.

A few days ago I posted an article about how Rhode Island is having trouble scraping together the $19 million or so that they need to operate HealthSource RI, now that the federal funds have pretty much dried up and the exchange has to pull its own weight. Some exchanges were set up with a funding mechanism in place (generally by charging either the insurance companies operating on the exchange, or the enrollees themselves, some sort of tax or fee), but others, like Rhode Island, were funded with federal dollars but never got around to setting up a way to pay for themselves after that funding stopped.

Anyway, a Republican state legislator in RI came up with an ingenious solution: Dump the exchange, even though it's functioning perfectly well. The reasoning is that the federal exchange, Healthcare.Gov, is operating more efficiently, so why not just do what Oregon and Nevada had to do this year (due to technical problems) and add themselves to the pile of 3 dozen states already being run through HC.gov?

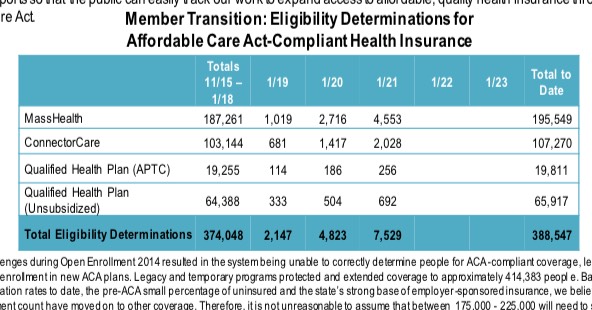

Today's update makes that even more clear: Another 2,976 QHP determinations likely means at least 1,300 more QHP selections, which should bring the total up to around 98,800 through last night. Another 1,200 today should put them over the top...and that's quite likely since the numbers should be ramping up further today (MA's February-start enrollment deadline is tomorrow).

For the record, this also means that Massachusetts has now officially enrolled 3x as many people in private policies as they did all of last year.

The Medicaid (MassHealth) side, meanwhile, isn't an estimate--those 195,549 people are enrolled immediately as I understand it. 4,500 more today and they've hit the 200K milestone.

*Well, ok, not all of them...they aren't breaking out zip codes with 50 or fewer enrollments in the interest of privacy...which is kind of ironic given my earlier entry today, but whatever.

I haven't done anything with this file yet, partly because I'm swamped with work (I do have a day job, remember), but mainly because I don't really get into the sub-state level stuff; I already have my hands full with the state-level data.

Still, there's a ton of interesting ways that you can slice & dice up this data, and huge kudos to HHS/CMS/HC.gov for the impressive leaps in transparancy this fall: First the weekly snapshots; then the state-level weekly snapshots; and now, this QHP-by-zip-code database.

David Ramsey has the full skinny on the unpleasant situation in Arkansas, where their "private option" Medicaid expansion program, which was always weird with a beard to begin with, is very much at risk of collapsing altogether:

Well, here we go again. The legislature is once again ready to debate the private option – the state’s unique version of Medicaid expansion, which uses funds available via the Affordable Care Act to purchase private health insurance for low-income Arkansans. Gov. Asa Hutchinson will take a long-awaited position on the policy in a speech at UAMS tomorrow morning. Then it will be up to the legislature. Health insurance for more than 200,000 Arkansans is at stake. Here are some keys to remember as the debate unfolds tomorrow and in the coming weeks.

The short version: The AR program has to be re-approved by the legislature every year, and requires a 75% majority to do so, so it's a wonder that it's survived this long, frankly.

Obamacare’s individual mandate is beginning to creep into outreach about signing up for health insurance this year.

The message is coming from two directions. Some outreach groups will move in the coming weeks to clearly mention the risk of rising penalties as they urge people to get covered before the enrollment season ends Feb. 15. And people who are getting an early start on their 2014 taxes — tax preparers say they expect the year’s first big surge in early February — will get a reminder of fines they may face for being uninsured last year and how much larger those fines could be one year from now if they say “No thanks” to Obamacare.

...But the mandate fines are going to start hitting home. As people start working on their 2014 tax forms, they will be able to see precisely how much they could pay in penalties for being uninsured last year. And it’s often more than the $95 they heard about.

No, I'm not gonna go into a "Dental Gate"-style rant against the HHS Dept. about this. Without knowing more details about the information in question or how it's being used, this may be another "nontroversy". Even so, it strikes me as being a bit of an unforced error on the part of the administration:

The government's health insurance website is quietly sending consumers' personal data to private companies that specialize in advertising and analyzing Internet data for performance and marketing,The Associated Press has learned.

The scope of what is disclosed or how it might be used was not immediately clear, but it can include age, income, ZIP code, whether a person smokes, and if a person is pregnant. It can include a computer's Internet address, which can identify a person's name or address when combined with other information collected by sophisticated online marketing or advertising firms.

Hot off the presses... HealthSource RI has posted their latest enrollment report; the new numbers are modest, but the payment data is rapidly improving; they're up to an 84% payment rate and the other 16% still have 6 days (from the 17th) to pay up.

DEMOGRAPHIC, AND VOLUME DATA THROUGH JANUARY 17, 2015

RENEWAL UPDATE As of January 17, 2015, 81% of Year One customers have renewed (selected a plan) for 2015 (72% of renewing customers paid the first month’s premium).

Total New Customers: 7,660 (5,646 paid)

Total Renewed Customers: 21,129 (18,460 paid) Total HealthSource RI enrollments for 2015 coverage: 28,789 (24,106 paid)

...Renewed Customers

2015 vs. 2014 Selection by Plan, by Metal Level and by Insurer

With the release of the latest data from HC.gov less than an hour ago, here's where things stand:

At least 33 states have now reached the "official" 2015 QHP enrollment target laid out for them by either the HHS Dept (10.4 million nationally) or, in some cases, individual state governments/exchanges. Again, this means roughly 30% more enrollees than the April 19, 2014 total, but in some cases it's higher or lower (for instance, Florida only targeted enrolling about 9% more people this year than last, while New York is hoping to nearly double their 2014 total...and Massachusetts is a whole different game).

Another 6 states (Connecticut, New Hampshire, Ohio, Tennesse, Texas and Wisconsin) are all within striking distance (90%+) of HHS's target; all should easily break through over the next 3 1/2 weeks.

The states which are lagging include Colorado, Minnesota, Rhode Island, Vermont and Washington State, which are all below 75% of the HHS/official goal as of their most recent update. Bear in mind, however, that some of these states are missing more data than the other states, so they may have made up some ground since the number shown.