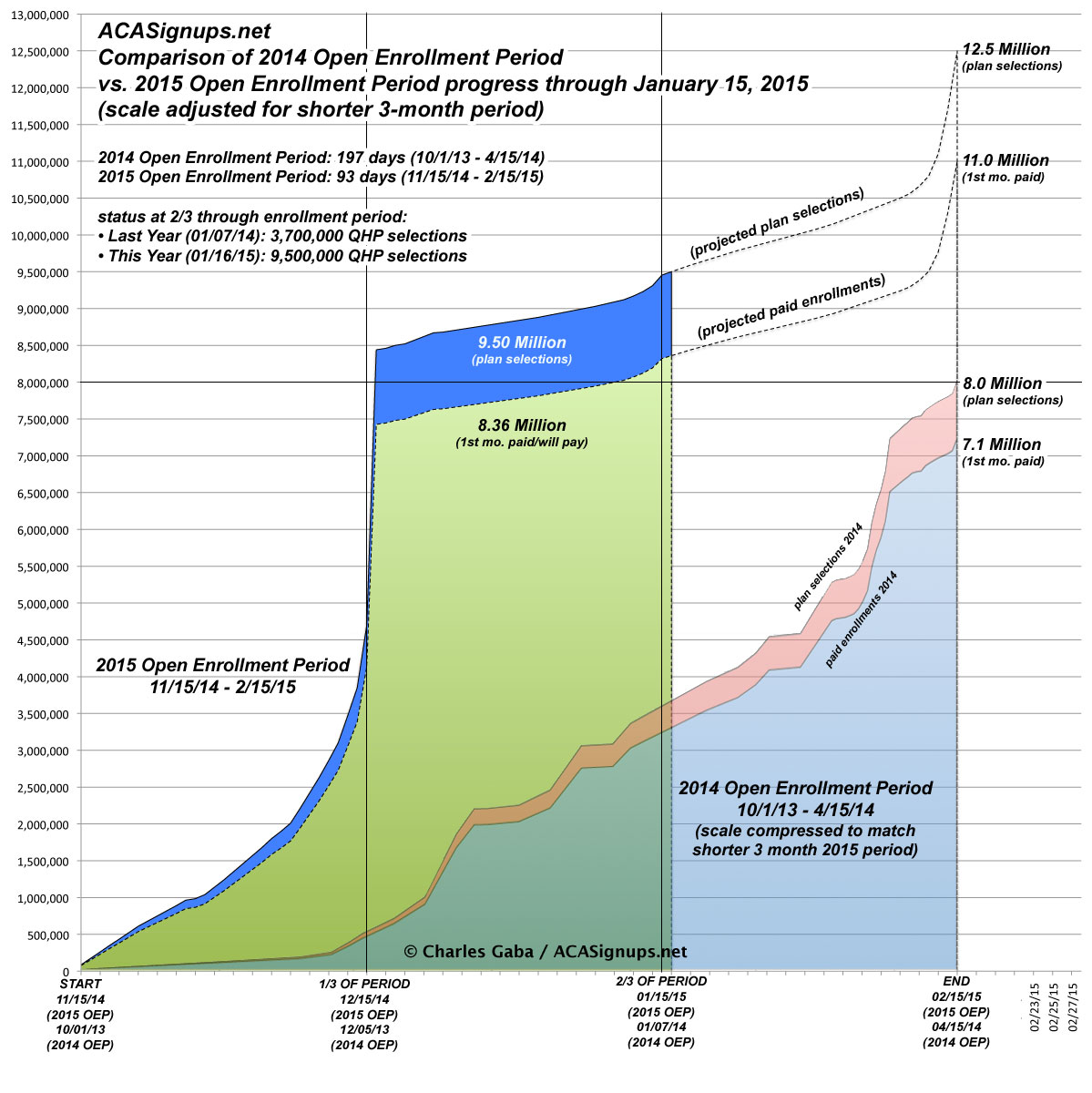

I put together a year-over-year overlay 1/3 of the way through open enrollment (right after the 12/15 deadline) and again at around the halfway point, both of which were pretty well-received, so now that we've crossed the 2/3 mark I've done an updated version.

I was going to use 1/15 as the cut-off date, but since the HHS "weekly snapshots" run through Fridays, I wanted to avoid the confusion of 2 different projection numbers, so I included the extra day to line this up with my 1/16 projection of 9.5 million QHPs even.

At the 2/3 point last year (around January 9th), total QHP selections were at around 3.7 million, versus the 9.5 million who should have enrolled for 2015 as of Friday night, or almost 2.6x as many. This gap will obviously close quickly once we move into the home stretch, but this period should still end with roughly a 50-60% increase over last year.

The following are, again, ACA/healthcare stories which I simply never had time to do write-ups on. Some of these are several weeks old, so please forgive any outdated-ness:

The Supreme Court on Monday rejected a 2-year-old legal challenge to a central provision of ObamaCare from a conservative doctors group.

The case, which was led by the Association of American Physicians and Surgeons, sought to strike down the law’s individual mandate, which fines individuals who fail to purchase health insurance.

The plaintiffs’ argument had been rejected twice before: first by a district court judge in 2012 and then by the D.C. Circuit Court of Appeals in March 2014.

As I reported Wednesday, brokers and small businesses using the D.C. Health Link exchange say the website is plagued with technical problems that have led to ongoing delays and frustrations. Among the problems: frozen screens, lost enrollment information, repeat error messages and other glitches. They also described ongoing delayed responses when they've reached out to the help resources for D.C. Health Link.

California's Obamacare exchange rejected a bid from the nation's largest health insurer to start selling coverage statewide next year.

The Covered California board adopted new rules Thursday that sharply limit where industry giant UnitedHealth Group Inc. could offer policies to individuals.

I haven't checked in on the Medicaid/CHIP enrollment situation in awhile, but with last week's revelation that California's Medicaid enrollment is a whopping 500,000 higher than previously thought, I probably should have done so earlier.

Well this one was unexpected: It's not a formal press release, but this story from the Hawaii Reporter--which actually has a pretty negative slant to it--is chock full of actual, current enrollment data points for Hawaii...and they're pretty good, relatively speaking.

None of the numbers are precise--they're all rounded off...but it's still a breath of fresh air from the Aloha state, and brings the number of states which haven't provided renewal data down from 3 to two (of course, the other two are California and New York, but still...)

...The Connector had about 1,000 people enrolled at this time last year. As of Thursday, that number had grown to 16,000.

...More than 365 small businesses, with 2,400 enrollees, have joined the Connector through the Small Business Health Options Program, or SHOP, in part because of tax deductions available to them, Kissel said.

So, that brings their total up to 91,430 as of...um...well, "the last week alone" suggests 7 days, which would mean either 1/07 - 1/13 or 1/09 - 1/15 (which would leave a 2-day gap). Fortunately, they then followed up with this:

Two months of open enrollment down & more than 125,000 Kentuckians have newly enrolled 4 health coverage or renewed their plans thru #kynect

Over the past month or so, the "Healthy Michigan" program (our name for ACA Medicaid expansion) has been bouncing around between 490K - 505K...a bit higher one week, a bit lower the next as people move on and off of it.

However, given that the estimated maximum number of Michiganders eligible for the program is somewhere between 477K - 500K depending on your source, it's unlikely to go much higher than that. I'll keep a close eye on it for the next few weeks, but assuming it continues to jostle above/below the 500K mark, I'll consider Michigan to be effectively "tapped out" and will likely stop reporting it every week.

Last week, with autorenewals added into the mix, MNsure was sitting at 41,704 QHPs as of January 5th. They just posted another update running through last night (the date of the numbers is actually as of the night before, as made clear from the corresponding press releases):

Latest Enrollment Numbers: January 16, 2015

MNsure will release 2015 enrollment metrics weekly, and will present a more robust metrics summary to the MNsure Board of Directors at each regularly-scheduled board meeting. During weeks that MNsure is closed on Friday, the enrollment metrics update will be released earlier in the week.

Health Coverage Type Cumulative Enrollments Medical Assistance 38,405

MinnesotaCare 16,056

Qualified Health Plan (QHP) 43,461

TOTAL 97,922

I was burned a couple of weeks in a row by overestimating the actual private policy (QHP) selections to date in Massachusetts by around 5% or so. Last week I downshifted a bit (from 50% of eligibility determinations to 45%), resulting in an estimate of around 90,700 QHPs as of Tuesday.

Today the MA exchange released their weekly dashboard, with official QHP selections, and sure enough, I'm back on target: 93,262 QHP selections as of Wednesday the 14th, in addition to 178,912 Medicaid (MassHealth) enrollees.

As for the payment rate, on the surface it appears to be just 72% (67,265 out of 93,262). However, remember that the 93K figure includes 19,000 people who are enrolling for coverage starting in February. We know this because of this update from December 30th:

Of the 74,203 people who selected plans by the Tuesday deadline, 51,888 paid their first month’s premium by Friday.

I've updated The Graph again, bringing things up to the end of the day today (Friday, January 16). After a 3-week "quiet period" (made even quieter due to both Christmas and New Year's), things should have heated up again this past week as yesterday's February coverage deadline approached.

The first week after the January deadline, HC.gov saw a mere 96K QHP selections due to Christmas Eve/Day, and the following week wasn't much better at 103K. As expected, they picked up somewhat last week with 163K QHPs.