For months now, the ACA state exchanges in small states like Rhode Island, Vermont and Hawaii have been struggling mightily with either funding issues (RI) or both funding and technical problems (VT & HI). Most of my own focus has been on the 2 northeastern states.

Today, however (thanks to Sabrina Corlette for the heads' up), the HI Health Connector has apparently skipped ahead a few chapters and concluded that due to their inability to convince the state legislature to pony up more cash (they were originally seeking $10 million but only $2 million was approved), they're gonna have to close up shop:

May 09--The Hawaii Health Connector has prepared a contingency plan to shut down operations by Sept. 30 after lawmakers failed to pass legislation to keep the state's troubled Obamacare insurance exchange afloat.

The looming case of King v. Burwell threatens subsidies that help 7.5 million people* afford health coverage in the roughly three dozen states using the Affordable Care Act’s federally run marketplace.

*(Note: As I've stated repeatedly, the actual number who would lose tax subsidies is "only" about 6.5 million, but the number who would lose their insurance as a result is likely a couple million more, plus another 4-5 million who'd pay through the nose to keep their coverage).

The Associated Press-GfK poll released Monday finds 56 percent wants the justices to rule to continue the subsidies, while 39 percent wants them invalidated for the federally run marketplaces.

There's also some interesting numbers about the politicization of the Supreme Court (y'know, the one which isn't supposed to be politicized):

In the latest update to The Graph, in addition to simply updating both the currently confirmed and estimated exchange-based QHP totals, I've also made one significant addition: The estimated number of HC.gov-based enrollees who are currently receiving federal tax credits from the IRS, and how many of those I expect to lose those credits in the event that the Supreme Court rules for the plaintiffs in the King v. Burwell case.

The total numbers nationally are notable mainly because of the milestones which have now been passed: Over 11.9 million QHP selections have been confirmed as of today, and I estimate that the actual total should have passed the 12.4 million mark by now. I now expect to hit my official "Open Enrollment Period" QHP selection target of 12.5 million in another couple of weeks (hey, look at that!--I was right after all, just early by...um....3 months...ok, never mind...).

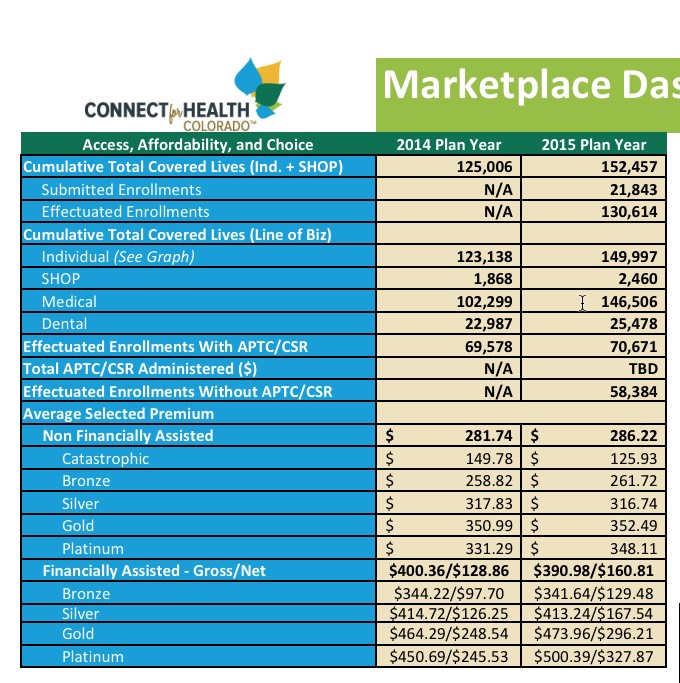

Colorado just released an updated enrollment report bringing things all the way up through April 30th...and as always, CO's report is both extremely comprehensive and extremely confusing at the same time.

A week or so ago, U of Michigan assistant law professor Nicholas Bagley and his associate, Boston U. public health asst. professor David K. Jones) posted a lengthy, comprehensive analysis of potential post-King v. Burwell options for the HHS Dept. and/or the impacted states in the event that the Supreme Court rules in favor of the plaintiffs. As I noted at the time, several of their points were very close to my own last July...except that I was just shooting off at the mouth, whereas they actually know what they're talking about, legally speaking.

What if HHS declared that any state that performs substantial, ongoing, and essential exchange functions has established an exchange, even if the state never formally elected to do so?

Last year, Connecticut was a perfect example of how the initial requested insurance policy rate changes from the companies involved in a given state can end up changing dramatically after the approval process (and in CT's case, change even more when the actual Open Enrollment period actually arrives). The original requested average increas in CT was 12.8%, but the approved changes ended up only being around 4.5%...and in the end they were far lower: Less than a 1% overall weighted average increase!

With that in mind, here's the story on 2016 requested changes in CT:

Four major health care providers that offer plans on Connecticut's health insurance marketplace have filed for rate increases for the upcoming open enrollment period that begins Nov. 1, 2015.

...The following increases have been proposed: 2 percent for ConnectiCare, 6.7 percent for Anthem, 12.4 percent for United Healthcare and 13.96 percent for Healthy CT.

Assuming this ratio hasn't shifted much over the past 6 years, around 28% of the total U.S. population are mothers

Obviously women over 64 (mostly on Medicare) are much more likely than the general population to be mothers...but girls under 18 are far less likely to be (well...under 16, anyway...the birth rate varies from state to state, of course), so I'm assuming that these cancel each other out, resulting in that 28% rate hopefully being roughly accurate.

On the one hand, Washington State, like Oregon, has a nifty, easy-to-use web-based searchable database for their 2016 rate request filings, yay!

On the other hand, when you get into the details, some of it can be pretty confusing stuff. In 2014, there were 8 companies approved for the WA exchange. For 2015, there were 10 companies, plus 2 more which didn't make the cut. For 2016, a total of 17 companies/subsidiaries have requested approval to sell on the individual market. There's no guarantee that all 17 will be approved to sell in the state, but I'm assuming they all will be for the time being.

There's actually 18 listings, however, because Lifewise split their policies into two entries...one of which is "grandfathered" policies only, and is therefore not relevant for the table below...although this does answer the question "how many people are sill enrolled in Grandfathered policies in Washington State?" The answer appears to be just 15,677 people...out of 343,348 total in the individual market, or only 4.5% of the total.

Since I made such a fuss over Colbeck's jaw-dropping laundry list of factual errors and omissions, I figure it behooves me to give the same scrutiny to the follow-up from a "union boss". Let's take a look:

They said it wouldn’t work.

They said no one wanted it.

They said it would destroy the economy.

They said it would create chaos in the healthcare industry and cause masses of people to lose their insurance.

They said no one would sign up for it; especially healthy and young people.

They even said it would lead to “death panels” deciding who will live or die under Obamacare.

From "It'll Destroy America!!" to "It Doesn't Suck But It Will Someday!" in 10 Easy Steps

1. October 2013: "No one can enroll!!"

(ok, this one is a gimme; the technical mess at HC.gov and some of the state exchanges did make it almost impossible for anyone to sign up the first month.)